Downloaded 34 times

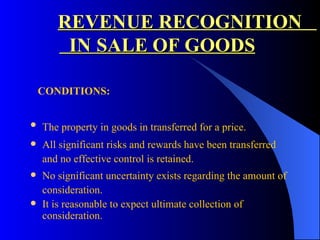

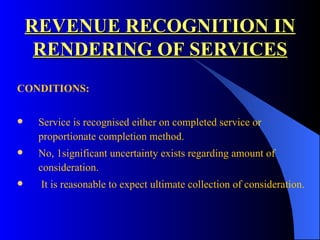

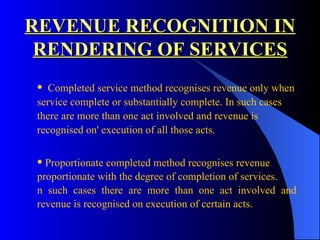

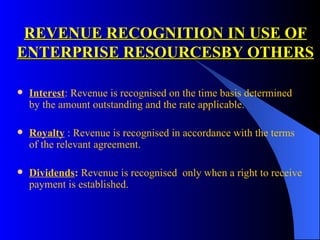

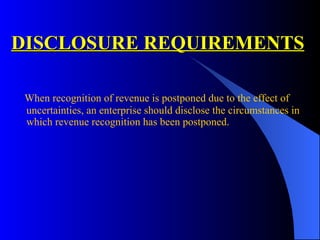

Accounting Standard-9 provides guidance on revenue recognition. It covers revenue from sale of goods, rendering of services, and use of enterprise resources. Revenue is recognized when risks and rewards are transferred for sale of goods or when services are completed or proportionately. Disclosure is required when revenue recognition is postponed due to uncertainties.