Downloaded 63 times

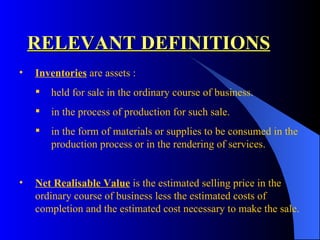

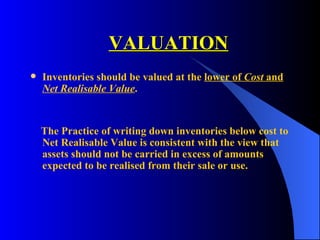

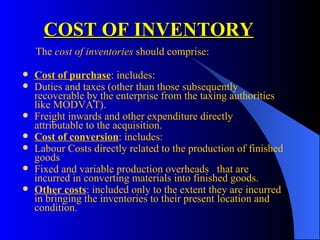

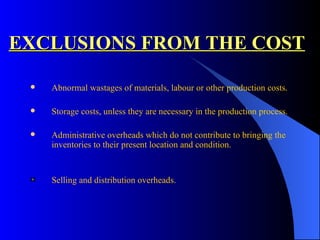

This document summarizes the key principles for valuing inventory according to Accounting Standard 2. Inventories should be valued at the lower of cost and net realizable value. Cost includes costs of purchase, conversion, and other costs to bring inventory to its present location and condition, but excludes abnormal wastage, storage costs unless necessary for production, and administrative and selling overheads. Net realizable value is estimated selling price less costs to complete and sell. Certain inventories like work in progress for construction contracts are excluded from this standard.