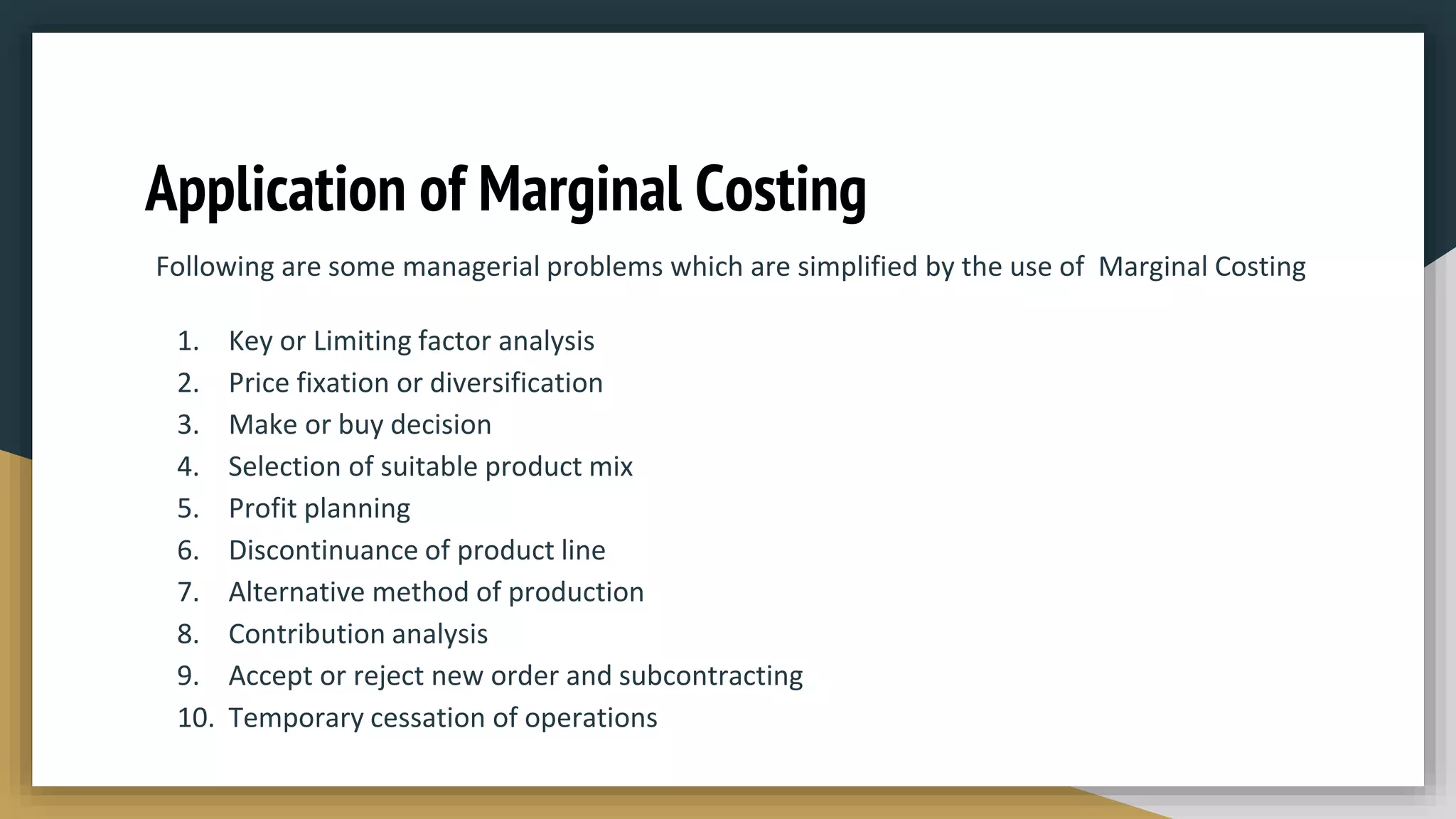

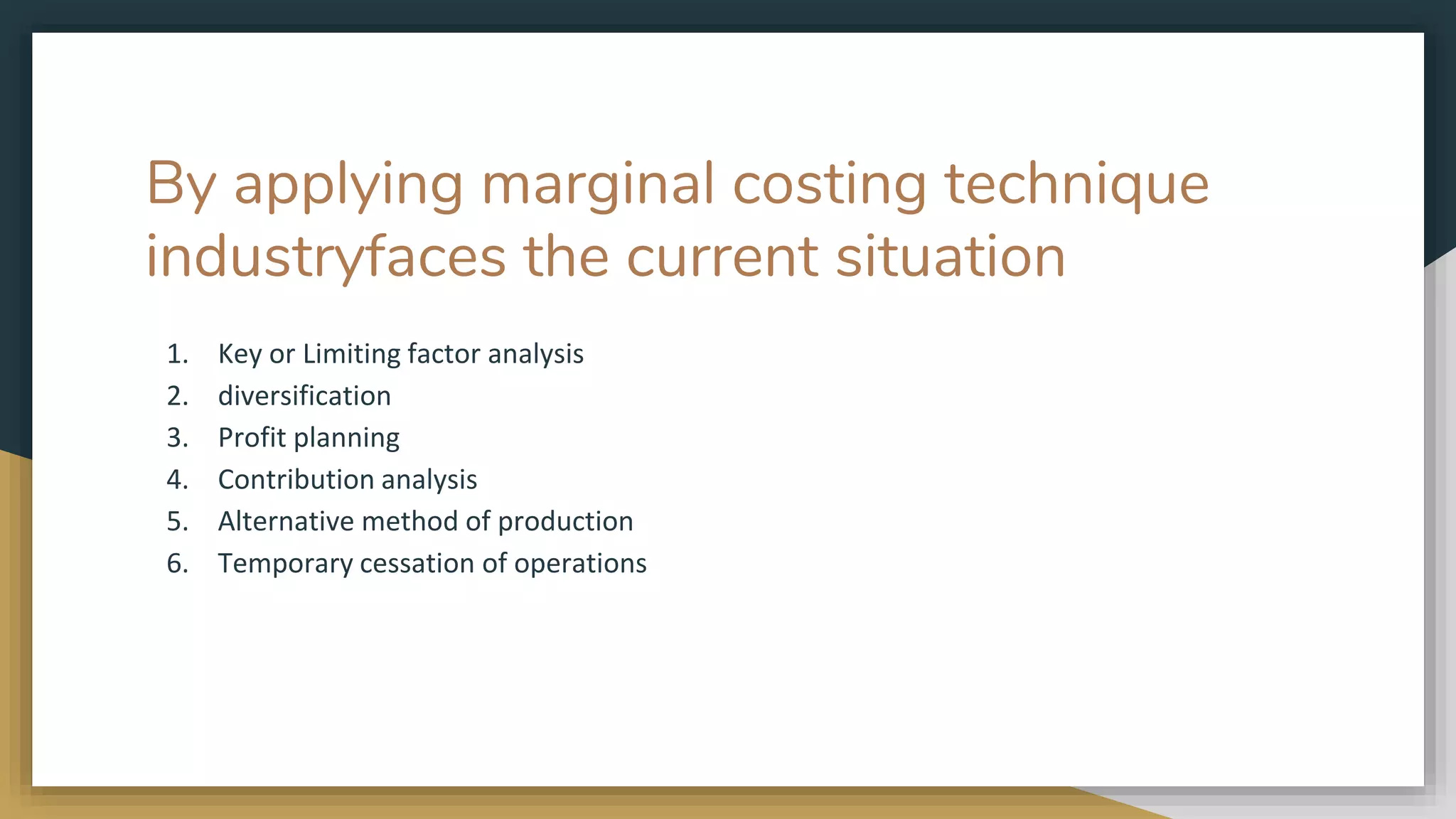

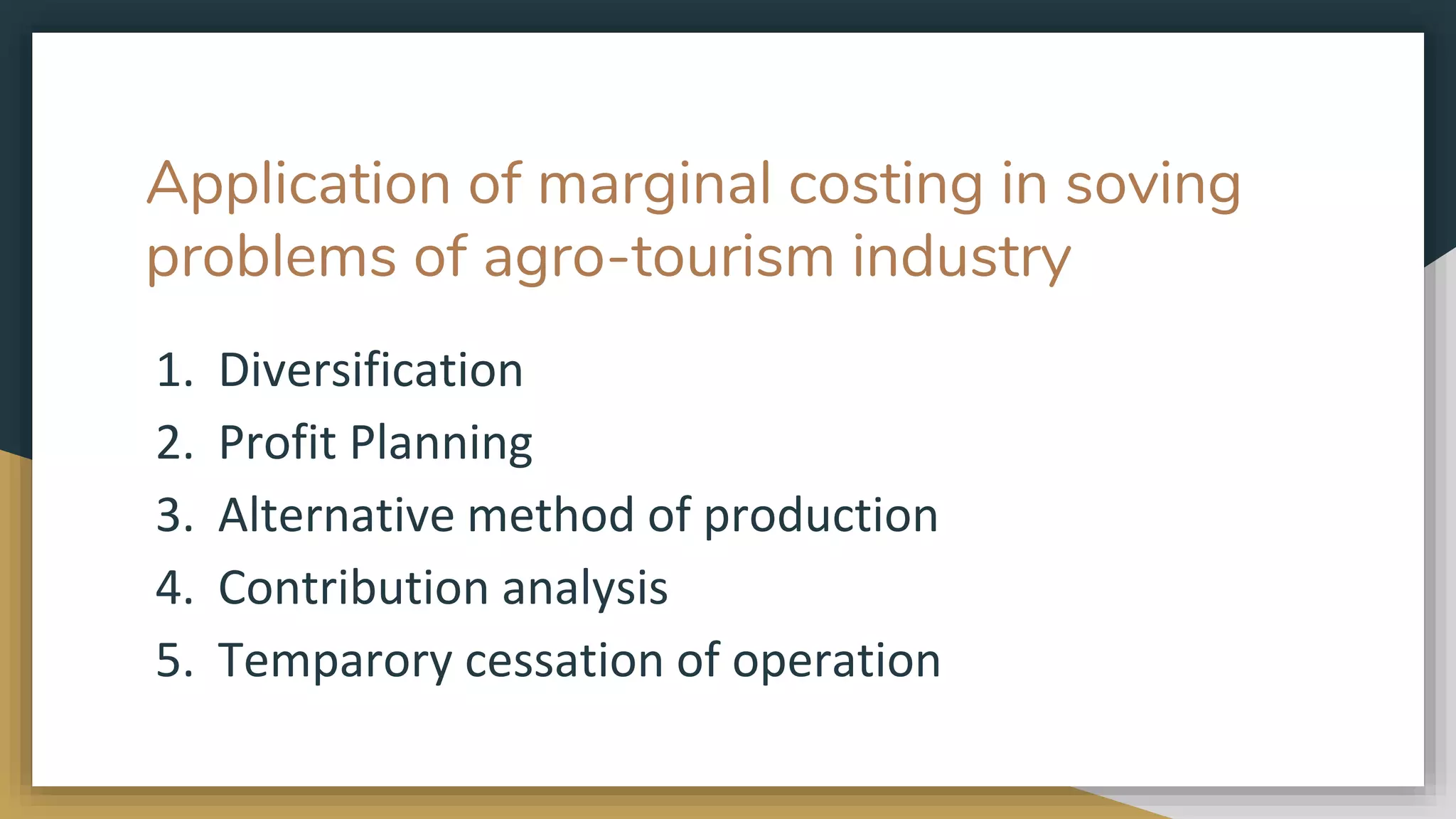

This presentation discusses the application of marginal costing techniques in decision making. It begins by defining marginal costing as the ascertainment of marginal costs and the effect on profit of changes in output volumes or types by differentiating between fixed and variable costs. Only variable costs are assigned to products, while fixed costs are written off against profits. The presentation then provides examples of how marginal costing can be applied to problems like key factor analysis, price fixation, make-or-buy decisions, product mix selection, and more. It also discusses a case study on applying marginal costing to analyze an agro-tourism business model and the impacts of COVID-19 on the tourism industry.