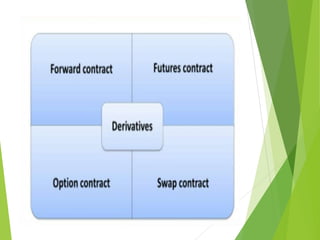

This document provides an overview of swaps, including: - A history of swaps beginning with the first interest rate swap in 1981 and growth to $250 trillion by 2006. - Definitions and key characteristics of swaps, which involve the exchange of cash flows between two counterparties according to a pre-arranged formula. - The main types of swaps are interest rate swaps, currency swaps, equity swaps, credit default swaps, and commodity swaps. Interest rate swaps and currency swaps make up the largest portion of the swap market.