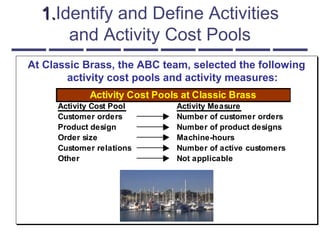

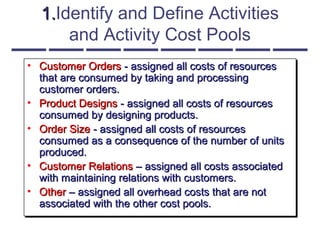

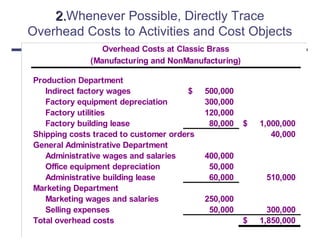

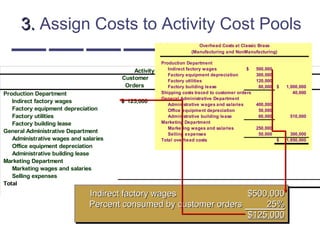

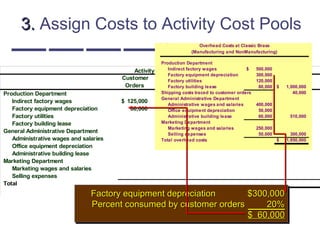

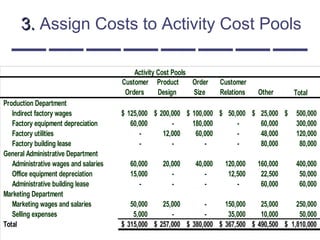

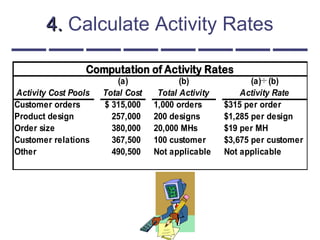

1. Classic Brass identified five activity cost pools: customer orders, product design, order size, customer relations, and other overhead. They traced costs to these pools based on consumption. 2. Costs were assigned to the pools. For example, 25% of indirect factory wages were assigned to customer orders. 3. Activity rates were calculated by dividing the total cost in each pool by the total activity for that pool. For customer orders, with $315,000 of costs and 1,000 orders, the rate was $315 per order.