Downloaded 31 times

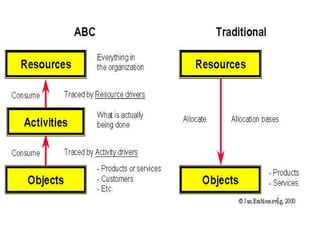

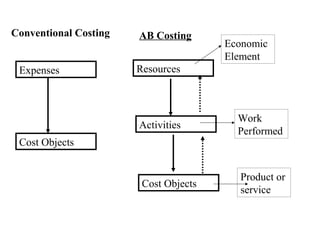

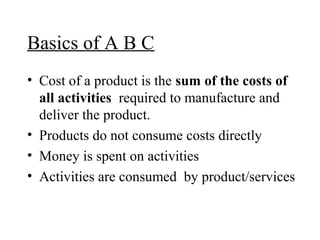

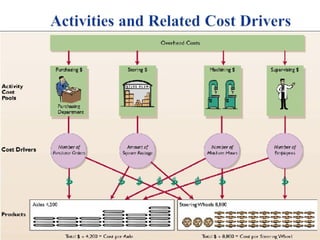

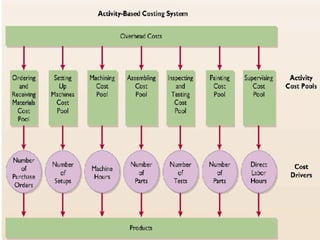

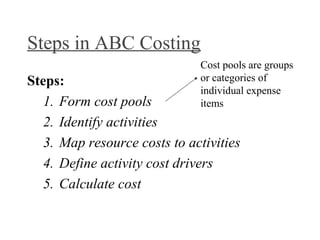

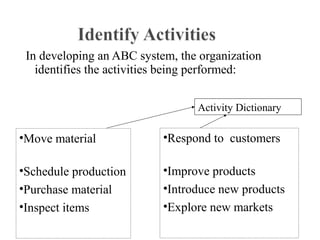

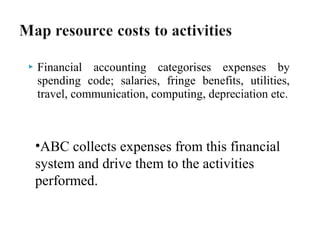

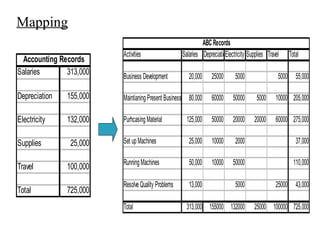

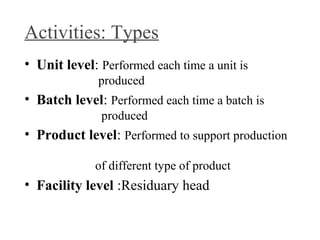

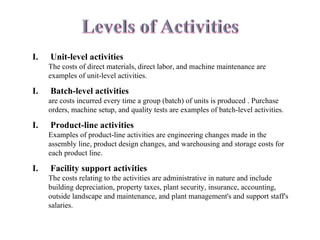

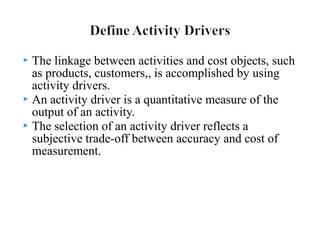

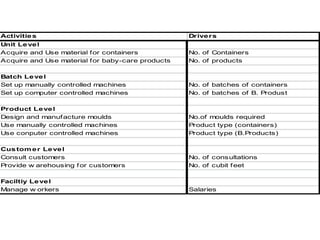

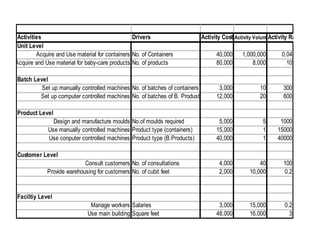

The document discusses Activity Based Costing (ABC), an approach for assigning overhead costs to products and services. It notes that traditional costing methods can misallocate overhead, affecting management decisions. ABC addresses this by tracing overhead costs to the activities that cause those costs, and then assigning the costs of each activity to products based on their use of that activity. This provides a more accurate picture of product costs. The document outlines the basic concepts and steps of implementing ABC, including identifying activities, assigning resource costs to activities, defining activity cost drivers, and calculating activity costs to allocate to cost objects like products.