Downloaded 44 times

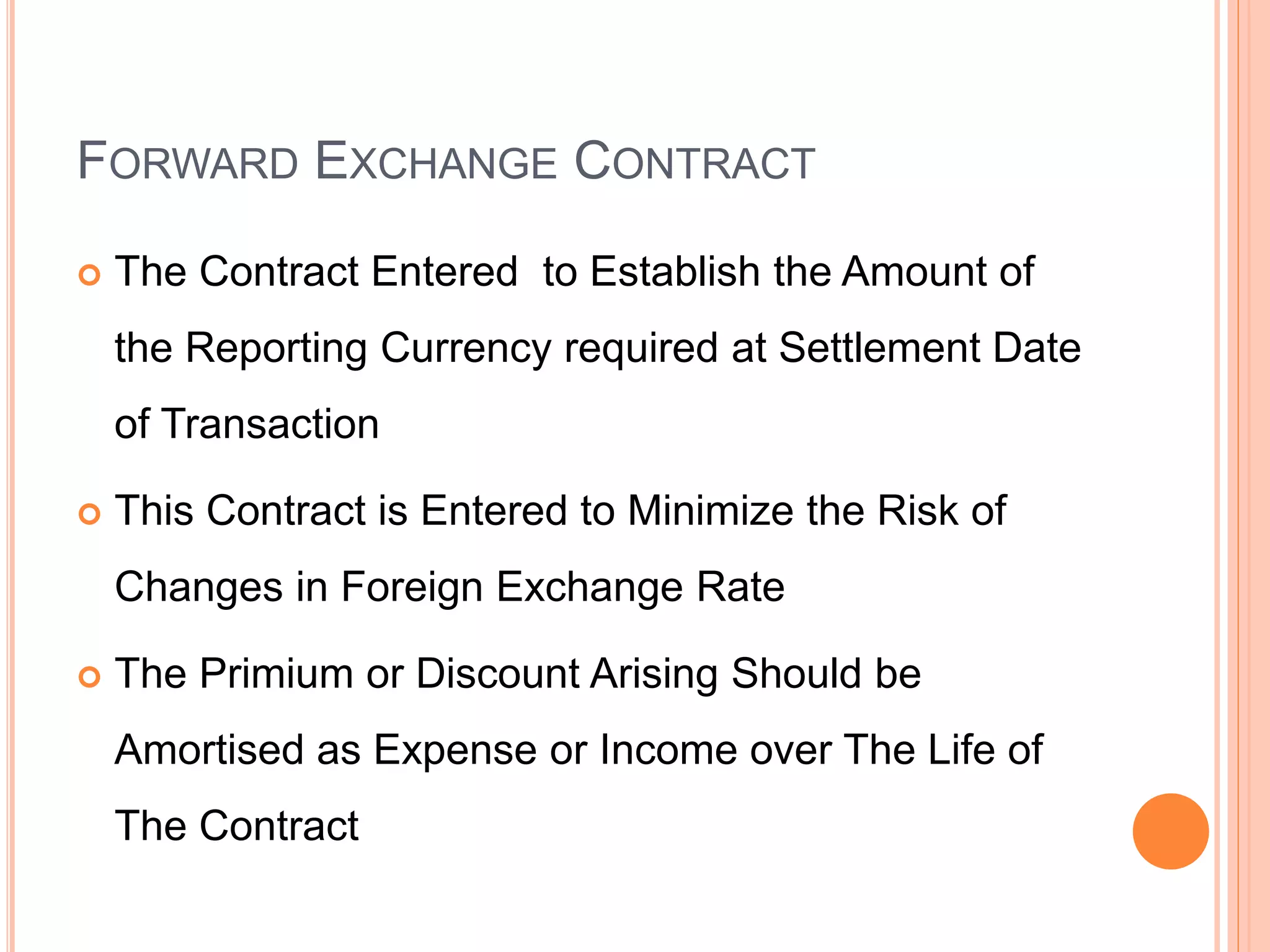

This document summarizes Accounting Standard 11 and 16 issued by the Institute of Chartered Accountants of India. Accounting Standard 11 provides guidelines for accounting of foreign exchange transactions and foreign operations. It defines key terms and outlines how foreign currency transactions should be initially recognized and reported. It also addresses recognition of exchange differences, disclosure requirements, and accounting for forward exchange contracts. Accounting Standard 16 provides the accounting treatment for borrowing costs and specifies that borrowing costs directly attributable to qualifying assets should be capitalized. It defines qualifying assets and distinguishes between specific and general borrowings.