Downloaded 118 times

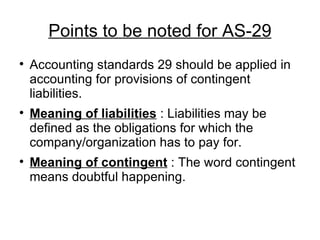

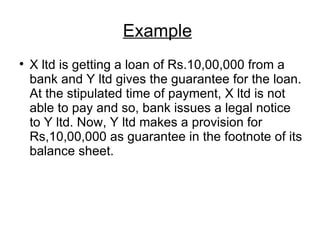

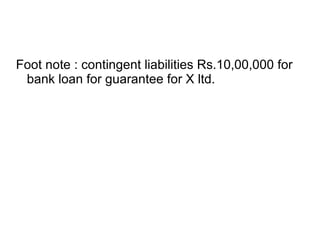

The document discusses Accounting Standard 29 (AS-29) regarding provisions for contingent liabilities. It defines contingent liabilities as possible obligations arising from past events that will only be confirmed by uncertain future events outside the company's control. Provisions should be made for obligations from past events when a reliable estimate can be made and the obligation is likely to affect the company's finances. AS-29 requires contingent liabilities and provisions to be disclosed in footnotes, including estimates of financial effects and uncertainties for contingent liabilities, and details of movements in provisions. An example is given of a company providing a provision for a guarantee it gave on another company's loan.