Downloaded 232 times

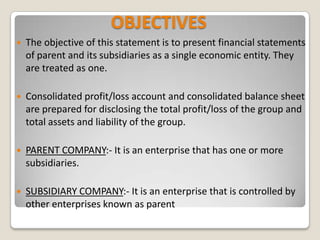

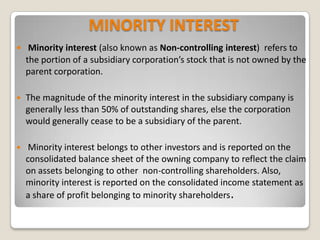

This document summarizes Accounting Standard 21 regarding the consolidation of financial statements for parent and subsidiary companies. The key points are: 1) The objective is to present consolidated financial statements that treat the parent and subsidiaries as a single economic entity. 2) Consolidated statements are prepared to disclose the total profit/loss and assets/liabilities of the entire group. 3) Minority interest represents the portion of a subsidiary's stock not owned by the parent, which is reported separately on the consolidated balance sheet and income statement. 4) The consolidation procedure involves eliminating intra-group balances and combining financial statement line items after eliminating the parent's investment in subsidiaries.

![Indian Accounting Standard [AS] -22 Tax on Income](https://cdn.slidesharecdn.com/ss_thumbnails/as22-150525045409-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)