Downloaded 80 times

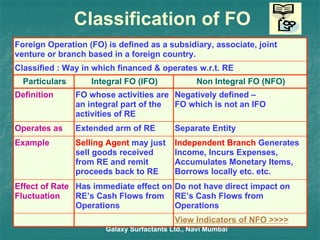

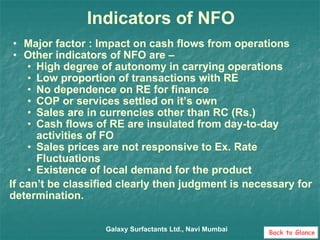

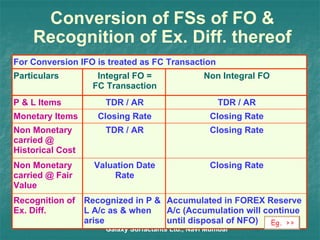

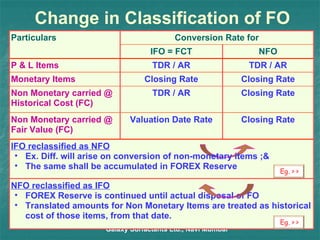

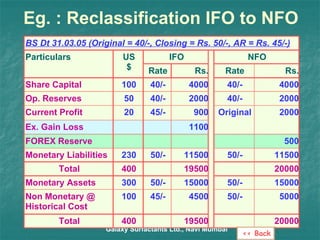

The document summarizes Accounting Standard 11 which provides guidance on accounting for changes in foreign exchange rates. Some key points covered include: - Foreign currency transactions and foreign operations are classified as integral or non-integral. Exchange differences for non-integral operations are accumulated in a foreign currency translation reserve. - Monetary items denominated in foreign currency are translated at closing rates. Non-monetary items are recorded based on historical rates. - Forward exchange contracts are marked to market on the balance sheet date and exchange gains or losses are recognized in profit and loss. - Disclosure requirements include exchange differences, foreign currency translation reserve, and changes in classifications of foreign operations.

![WHOMOVEDMYCHEESE___[1]](https://cdn.slidesharecdn.com/ss_thumbnails/3973179-thumbnail.jpg?width=640&height=640&fit=bounds)