Download to read offline

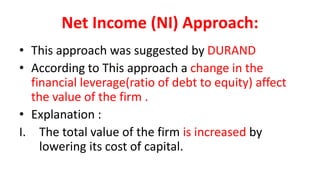

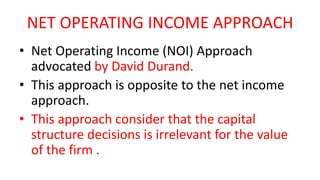

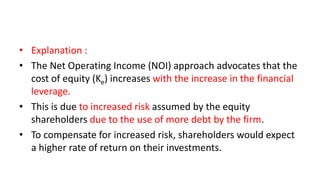

The document discusses different theories of capital structure: 1. The Net Income Approach suggests that firm value increases by lowering cost of capital through increasing debt. The optimum structure is when cost and firm value are maximum. 2. The Net Operating Income Approach argues that equity cost rises with debt, offsetting lower debt costs. Firm value is unaffected by capital structure. 3. The Traditional Approach finds a balance, where judicious debt use initially lowers overall costs and raises firm value, but beyond a point costs rise and value falls. 4. The Modigliani-Miller Approach similarly finds no relationship between capital structure and firm value/costs when ignoring taxes, but recognizes taxes lower effective debt costs

![[wacc] weighted average cost of capital](https://cdn.slidesharecdn.com/ss_thumbnails/anuragmathur-210703072911-thumbnail.jpg?width=640&height=640&fit=bounds)