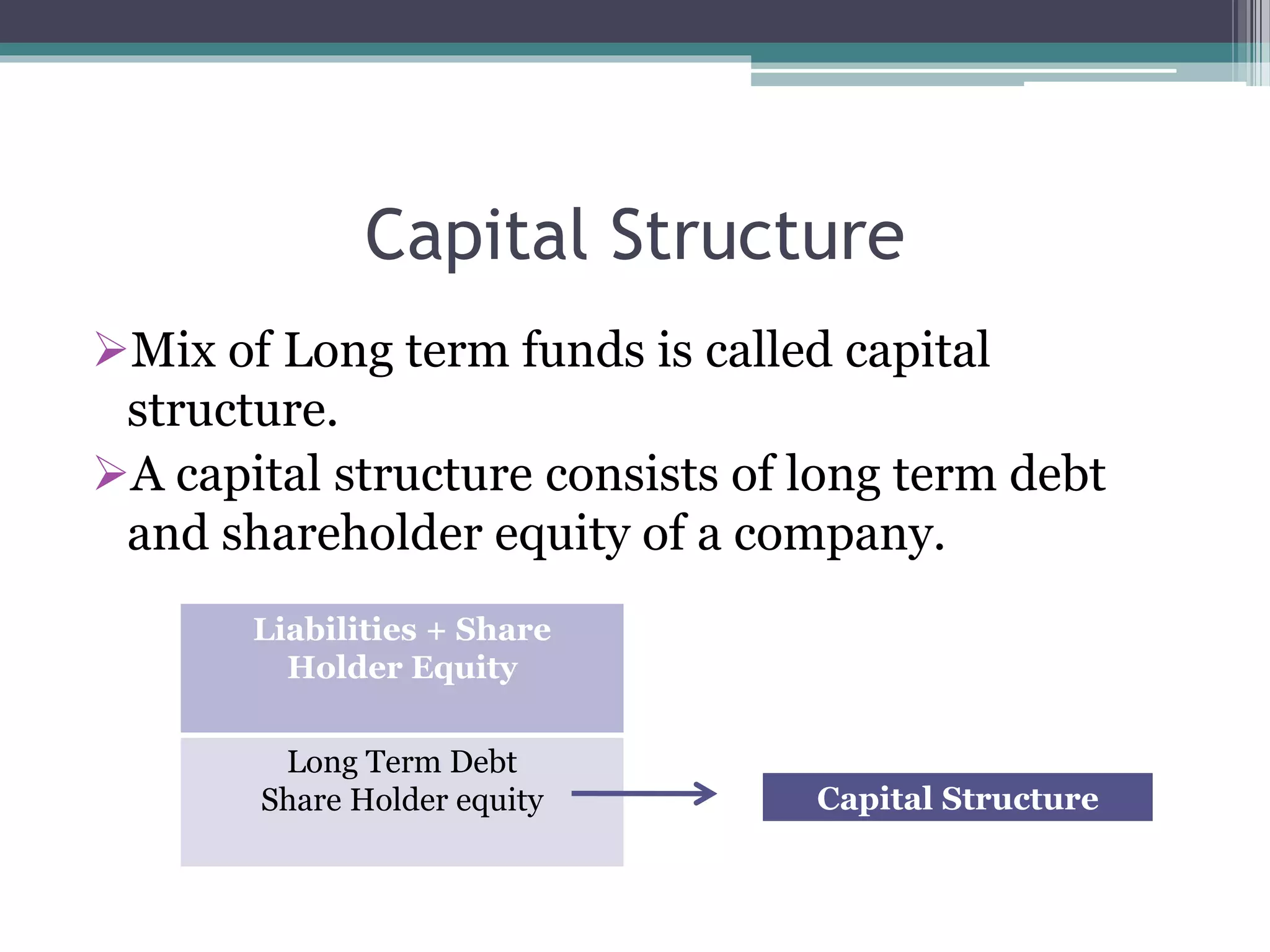

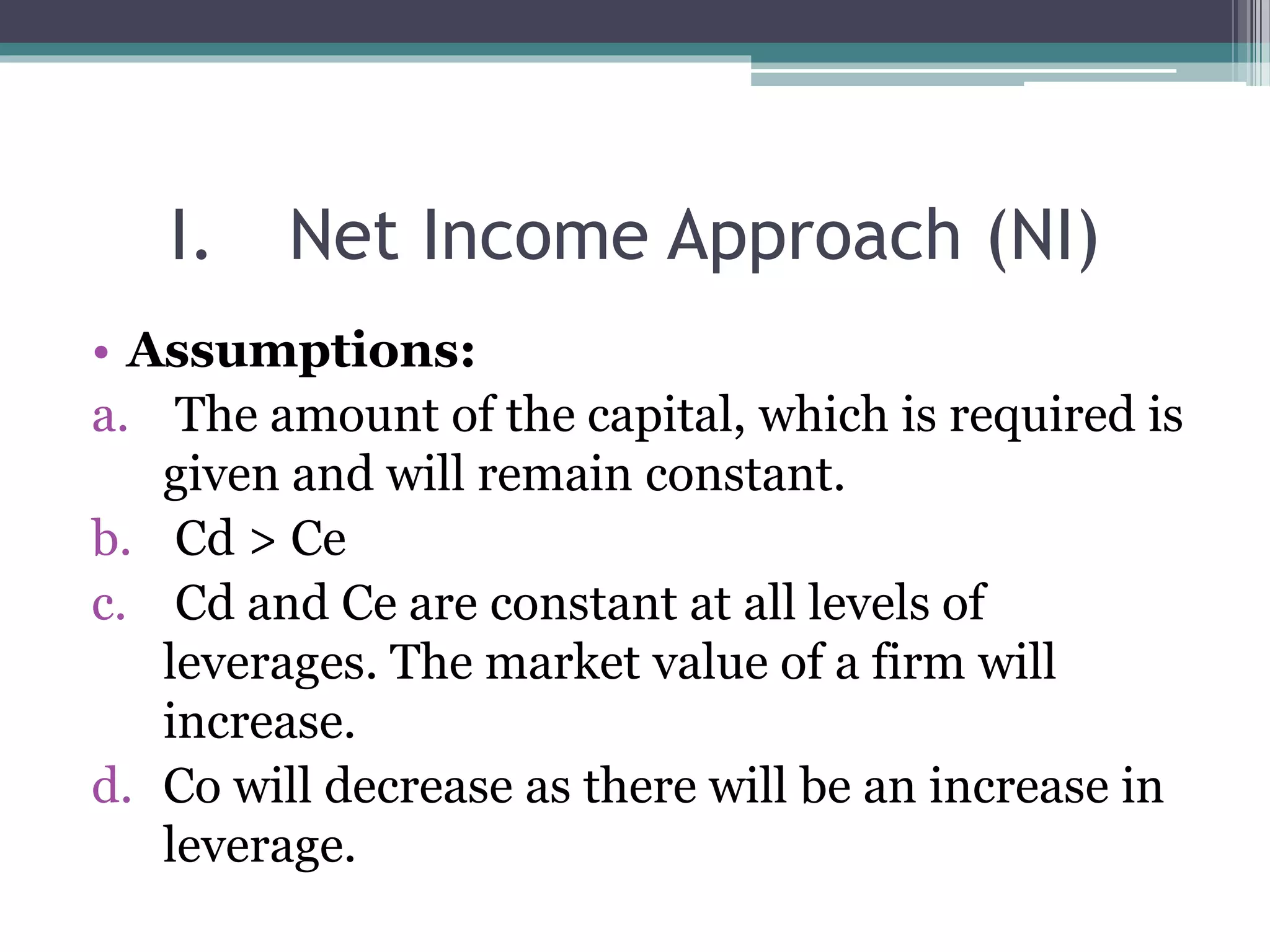

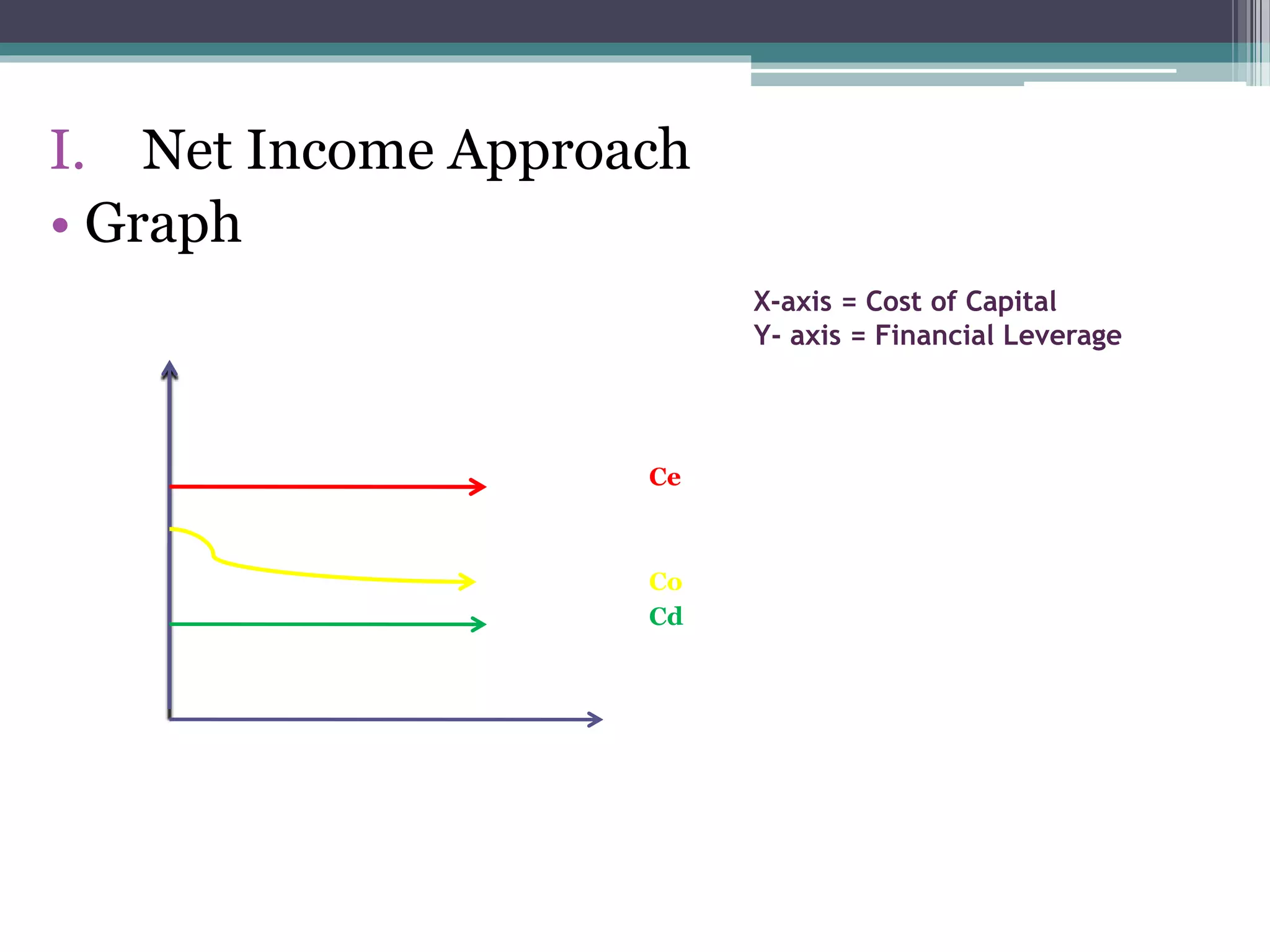

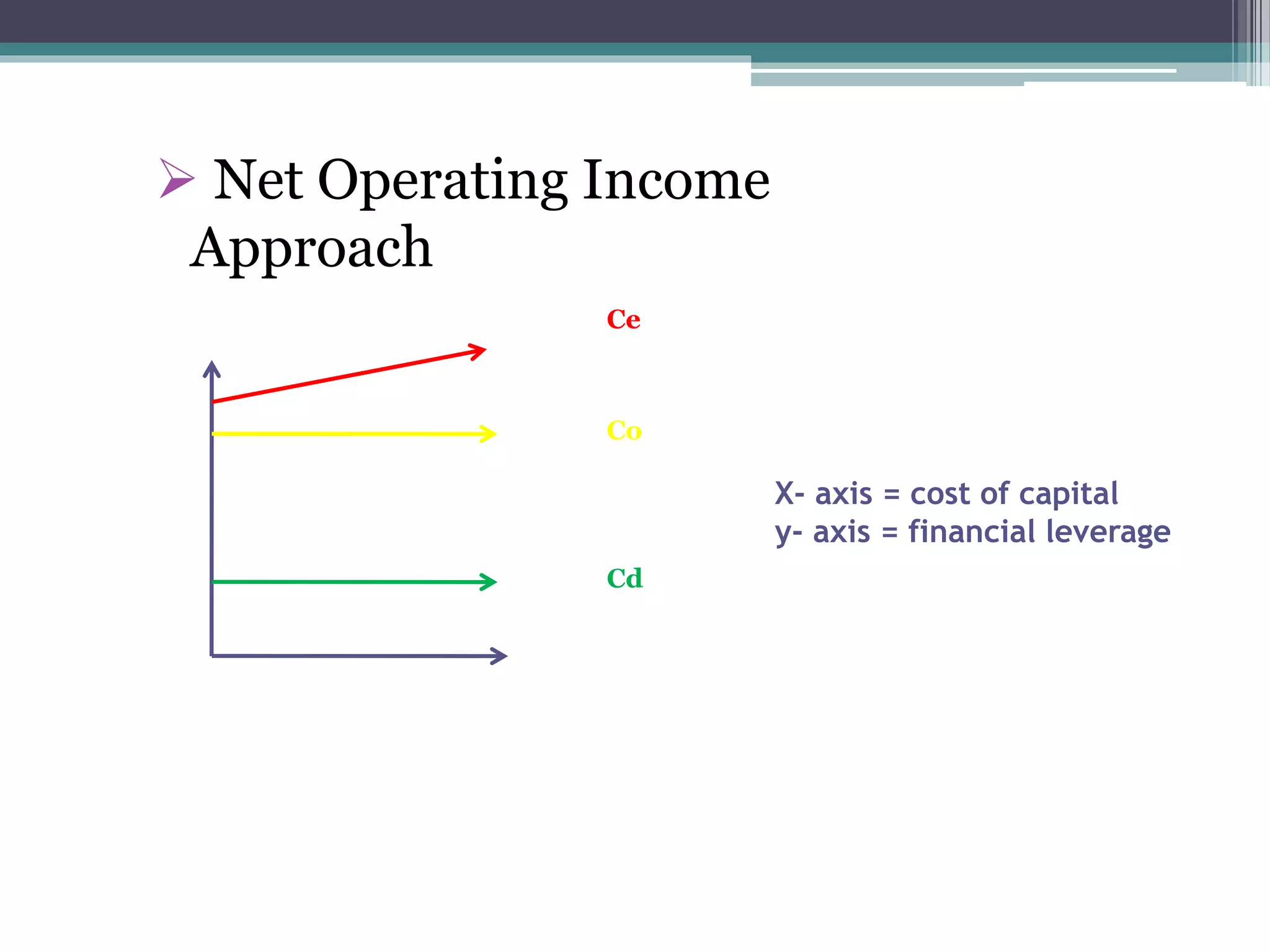

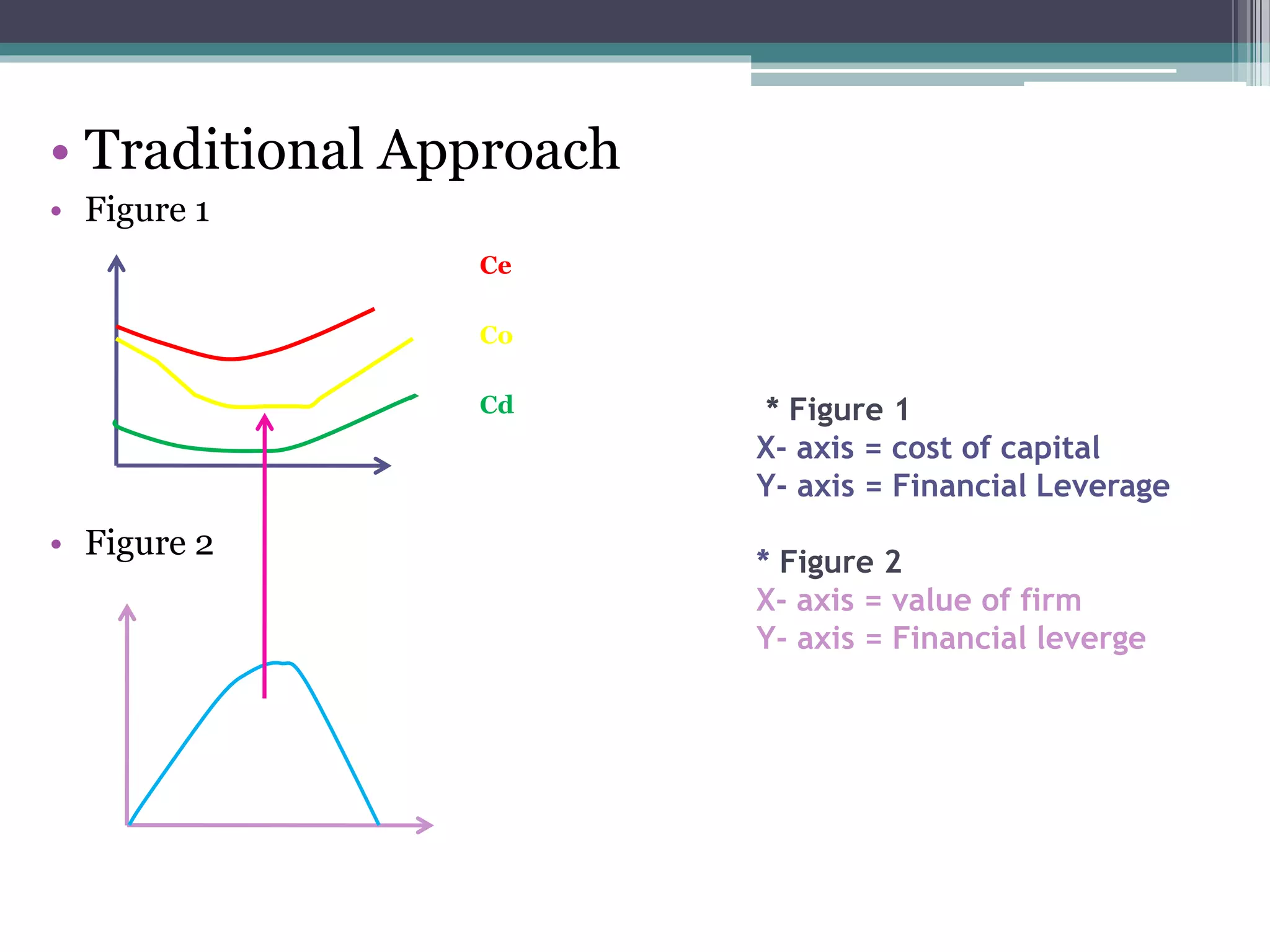

This document discusses various theories of capital structure. It begins by defining capital structure as the mix of long-term funds used by a company, including long-term debt and shareholder equity. It then outlines four main approaches to capital structure: 1) The Net Income Approach suggests capital structure impacts a firm's market value through its effect on net income. 2) The Net Operating Income Approach argues capital structure does not impact firm value. 3) The Traditional Approach finds an optimal capital structure that balances increasing and decreasing returns. 4) The Miller-Modigliani Approach similarly argues capital structure does not matter under certain assumptions but allows for tax benefits of debt.