Famous Kala Jadu, Black magic expert in Faisalabad and Kala ilam specialist i...

JP Associates

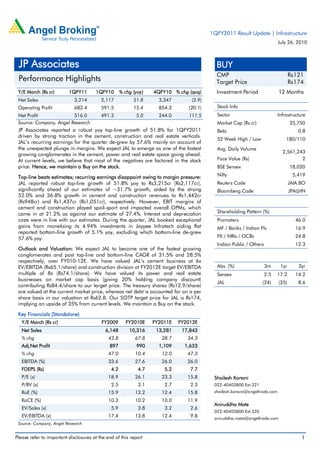

1. 1QFY2011 Result Update | Infrastructure

July 26, 2010

JP Associates BUY

CMP Rs121

Performance Highlights Target Price Rs174

Y/E March (Rs cr) 1QFY11 1QFY10 % chg (yoy) 4QFY10 % chg (qoq) Investment Period 12 Months

Net Sales 3,214 2,117 51.8 3,347 (3.9)

Operating Profit 682.4 591.5 15.4 854.3 (20.1) Stock Info

Net Profit 516.0 491.3 5.0 244.0 111.5 Sector Infrastructure

Source: Company, Angel Research Market Cap (Rs cr) 25,750

JP Associates reported a robust yoy top-line growth of 51.8% for 1QFY2011 Beta 0.8

driven by strong traction in the cement, construction and real estate verticals.

52 Week High / Low 180/110

JAL’s recurring earnings for the quarter de-grew by 57.6% mainly on account of

the unexpected plunge in margins. We expect JAL to emerge as one of the fastest Avg. Daily Volume

2,561,243

growing conglomerates in the cement, power and real estate space going ahead.

At current levels, we believe that most of the negatives are factored in the stock Face Value (Rs) 2

price. Hence, we maintain a Buy on the stock. BSE Sensex 18,020

Top-line beats estimates; recurring earnings disappoint owing to margin pressure: Nifty 5,419

JAL reported robust top-line growth of 51.8% yoy to Rs3,215cr (Rs2,117cr), Reuters Code JAIA.BO

significantly ahead of our estimates of ~31.7% growth, aided by the strong Bloomberg Code JPA@IN

52.0% and 36.8% growth in cement and construction revenues to Rs1,442cr

(Rs948cr) and Rs1,437cr (Rs1,051cr), respectively. However, EBIT margins of

cement and construction played spoil-sport and impacted overall OPMs, which

came in at 21.2% as against our estimate of 27.4%. Interest and depreciation Shareholding Pattern (%)

costs were in line with our estimates. During the quarter, JAL booked exceptional Promoters 46.0

gains from monetising its 4.94% investments in Jaypee Infratech aiding flat MF / Banks / Indian Fls 16.9

reported bottom-line growth of 5.1% yoy, excluding which bottom-line de-grew

57.6% yoy. FII / NRIs / OCBs 24.8

Indian Public / Others 12.3

Outlook and Valuation: We expect JAL to become one of the fastest growing

conglomerates and post top-line and bottom-line CAGR of 31.5% and 28.5%

respectively, over FY010-12E. We have valued JAL’s cement business at 6x

EV/EBITDA (Rs65.1/share) and construction division at FY2012E target EV/EBITDA Abs. (%) 3m 1yr 3yr

multiple of 8x (Rs74.1/share). We have valued its power and real estate Sensex 2.5 17.2 14.2

businesses on market cap basis (giving 20% holding company discount)

JAL (24) (25) 8.6

contributing Rs84.4/share to our target price. The treasury shares (Rs12.9/share)

are valued at the current market price, whereas net debt is accounted for on a per

share basis in our valuation at Rs62.8. Our SOTP target price for JAL is Rs174,

implying an upside of 35% from current levels. We maintain a Buy on the stock.

Key Financials (Standalone)

Y/E March (Rs cr) FY2009 FY2010E FY2011E FY2012E

Net Sales 6,148 10,316 13,281 17,843

% chg 43.8 67.8 28.7 34.3

Adj.Net Profit 897 990 1,109 1,633

% chg 47.0 10.4 12.0 47.3

EBITDA (%) 33.6 27.6 26.0 26.0

FDEPS (Rs) 4.2 4.7 5.2 7.7

P/E (x) 18.9 26.1 23.3 15.8 Shailesh Kanani

P/BV (x) 2.5 3.1 2.7 2.3 022-40403800 Ext:321

RoE (%) 15.9 13.2 12.4 15.8 shailesh.kanani@angeltrade.com

RoCE (%) 10.3 10.2 10.0 11.9

Aniruddha Mate

EV/Sales (x) 5.9 3.8 3.2 2.6

022-40403800 Ext:335

EV/EBITDA (x) 17.4 13.8 12.4 9.8 aniruddha.mate@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

3. JP Associates |1QFY2011 Result Update

Exhibit 3: 1QFY2011 Segmental standalone performance

Y/E March (Rs cr) 1QFY2011 1QFY2010 % chg

Segment Revenue

Cement & Cement Products 1,441 948 52.0

Construction 1,437 1,051 36.8

Power 11 11 (1.4)

Hotel/Hospitality and Golf Course 37 34 9.6

Real Estate 366 95 284.6

Investment 3 - -

Others 4 5 (18.5)

Unallocated 30 18 63.7

Less: Inter-Segmental Performance 112 45 149.9

Total Sales Income 3,218 2,117 52.0

Segment Results

Cement & Cement Products 286.3 301.6 (5.1)

Construction 104.8 183.3 (42.9)

Power 7.0 7.1 (2.1)

Hotel/Hospitality and Golf Course (1.3) 2.2 -

Real Estate 155.8 44.7 248.8

Investment 3.3 - -

Others 0.7 (1.5) -

Exceptional item : Profit on Sale of Shares 513.2 374.6

Total PBIT 1,070 912.1 17.3

Less: Interest Expense 327.9 221.9 47.8

Less: Exceptional Item - 101.6 0.0

Less: Unallocable Expense 21.9 47.6 (53.9)

PBT 719.9 541.0 33.1

PBIT Margin (%) bp chg

Cement & Cement Products 19.9 31.8 (1,194)

Construction 7.3 17.5 (1,016)

Power 63.1 63.6 (44)

Hotel/Hospitality and Golf Course (3.4) 6.6 -

Real Estate 42.6 46.9 (437.0)

Investment 100.0 - -

Others 19.2 (31.5) -

Capital Employed in Segment

Cement & Cement Products 12,990 9,954 30.5

Construction 2,900 1,833 58.2

Power 596 255 133.9

Hotel/Hospitality and Golf Course 481 621 (22.6)

Real Estate 2,154 612 251.8

Investment 5,727 4,504 27.1

Others 262 139 89.0

Unallocated 3,173 4,077 (22.2)

Total 28,282 21,995 28.6

Source: Company, Angel Research

July 26, 2010 3

4. JP Associates |1QFY2011 Result Update

Segment-wise performance

Cement division

JAL’s cement division reported revenue growth of 52.0% yoy to Rs1,441cr

(Rs948.2cr), 7.8% above our estimate of Rs1,337cr. The divisional EBIT margin

came in at 19.9% (31.8%). JAL currently has an installed cement capacity of ~24

MTPA and 1QFY2011 dispatch volumes of ~3.8MTPA. We expect the company to

achieve dispatch volumes of 14.6mtpa and top-line of Rs4,636cr for FY2011E.

Construction division

The construction division reported revenue growth of 36.8% yoy to Rs1,437cr

(Rs1,050cr) as against our expectation of Rs1,171cr. The divisional EBIT margin

came in at 7.3% (17.5%). The in-house construction segment faced margin

pressure due to stoppage of work at Baglihar II and Srisailam canal projects.

Real estate division

The real estate division reported 284.6% yoy revenue growth to Rs366cr (Rs95.2cr)

as against our expectation of Rs183cr. The divisional EBIT margin came in at

42.6% (46.9%).

Exhibit 4: Quarterly revenue trend Exhibit 5: Quarterly EBITDA trend

4,000 113.8 120.0 900

37.0

40.0

3,500 60.5 800 34.0 35.0

82.6 51.8 100.0

3,000 700 28.5 25.5 30.0

62.9 80.0

2,500 600 23.1

21.2 25.0

48.3 53.0 25.8 23.6

2,000 60.0 500

20.0

1,500 38.3 400

40.0 15.0

1,000 300

20.0 10.0

500 200

0 - 100 5.0

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

0 -

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Sales (Rs cr, LHS) Growth (yoy %, RHS) EBITDA (Rs cr, LHS) EBITDAM (%, RHS)

Source: Company, Angel Research Source: Company, Angel Research

Exhibit 6: Quarterly net profit trend

1,000 60.0

900

800 47.7 50.0

700 40.0

600

500 30.0

400 23.2

300 18.5 20.0

17.1 16.1

200 12.6 10.0

100 7.3

3.6

0 -

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

PAT (Rs cr, LHS) PATM (%, RHS)

Source: Company, Angel Research

July 26, 2010 4

5. JP Associates |1QFY2011 Result Update

Investment Arguments

On schedule cement capacity expansion instills confidence: JAL is on its way to

become one of the leading players in the cement space following capacity

expansion from 9.0mtpa in FY2008 to 37.6mtpa in FY2012E. The capacity

expansion is on track and in line with management guidance. Cement contributed

44%, 35% and 38% to standalone top-line in FY2008, FY2009 and FY2010

respectively, and is expected to contribute 35% and 38% in FY2011E and

FY2012E, respectively. We believe that the cement capacity size that JAL proposes

to set up would enable it to have substantial bargaining power, result in operating

leverage benefits and catapult JAL into the league of cement majors.

Exhibit 7: JAL's cement capacity vis-a-vis peers

60.0 48.9

50.0 37.6

40.0 27 30.4

30.0

15.8 14.0

20.0

10.0 5.4

-

ACC

Ambuja

Madras Cem

India Cements

JP Associates

JK Lakshmi

Grasim (Incl.

Ultratech)

Cem

FY09 FY10E FY11E FY12E

Source: Company, Angel Research

Construction arm to log 26.4% CAGR over FY2010-12E: JAL is developing the

160km, 6-lane (extendable to 8 lanes) access controlled Yamuna expressway

between Noida and Agra. The Yamuna expressway (YE) project also involves real

estate development to the tune of 530mn.sq.ft. The cost of YE is Rs9,739cr and

has a concession period of 36 years. Financial closure of the YE is done with 69%

of the TPC already put in (equity component of Rs1,250cr, IPO proceeds of

Rs1,500cr and debt of Rs4,477cr). Moreover, Jaypee Infratech is in possession of

96.5% of the land required for construction of the highway, and work is on

schedule. Thus, JAL’s strong execution track record backed by in-place funding

and acquired land renders strong visibility to its construction arm.

Diversified play: JAL is a unique play on the ongoing infrastructure theme with a

bouquet of offerings in construction, cement, power and real-estate. Moreover, not

only does the company have a diversified set of offerings, but also enjoys scale

benefits in each of them. We believe that the company stands to benefit as the

infrastructure theme pans out going ahead.

Outlook and Valuation: We expect JAL to be one of the fastest growing

conglomerates and post top-line and bottom-line CAGR of 31.5% and 28.5%

respectively, over FY010-12E. We have valued JAL’s cement business at 6x

EV/EBITDA (Rs65.1/share) and construction division at FY2012E target EV/EBITDA

multiple of 8x (Rs74.1/share). We have valued its power and real estate businesses

on market cap basis (giving 20% holding company discount) contributing

Rs84.4/share to our target price. The treasury shares (Rs12.9/share) are valued at

the current market price, whereas net debt is accounted for on a per share basis in

our valuation at Rs62.8. Our SOTP target price for JAL is Rs174, implying an

upside of 35% from current levels. We maintain a Buy on the stock.

July 26, 2010 5

6. JP Associates |1QFY2011 Result Update

Exhibit 8: SOTP Valuation Summary

Business Segment Methodology Rs cr Rs/share % to Target Price

Cement EV/EBIDTA (x) 6x EV/EBITDA 13,848 65.1 37.4

Construction EV/EBIDTA (x) 8x EV/EBITDA 15,760 74.1 42.5

Power Mcap of JPVL @20% holding co discount 9,190 43.2 24.8

Real Estate NAV , Mcap Jaypee InfraTech + Jaypee Greens 8,651 40.7 23.4

Hotels - 8x FY2012E Net Profit 148 0.7 0.4

Treasury Stock At CMP 2,758 13.0 7.4

Net Debt - Net Debt for Cement, Construction and Real Estate Business (13,311) (62.6) (35.9)

Total 37,044 174.1 100.0

Source: Company, Angel Research

Exhibit 9: Key Assumptions

Particulars FY2009 FY2010 FY2011E FY2012E

Cement Capacity (MT) 14.7 20.6 26.4 30.8

Cement Production (MT) 7.6 11.2 15.5 22.0

Cement Sales (MT) 7.0 10.6 14.6 20.8

Realisations /Ton 3,594 3,754 3,491 3,631

Source: Company, Angel Research

Exhibit 10: Angel EPS forecast v/s consensus

(Rs) Angel Forecast Bloomberg Consensus Variation

FY2011E 5.2 5.9 13.2

FY2012E 7.7 6.9 (10.4)

Source: Company, Angel Research

July 26, 2010 6

12. JP Associates |1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement (Company name) JP Associates

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

July 26, 2010 12