Download as PDF, PPTX

![Geometric Gradient Series

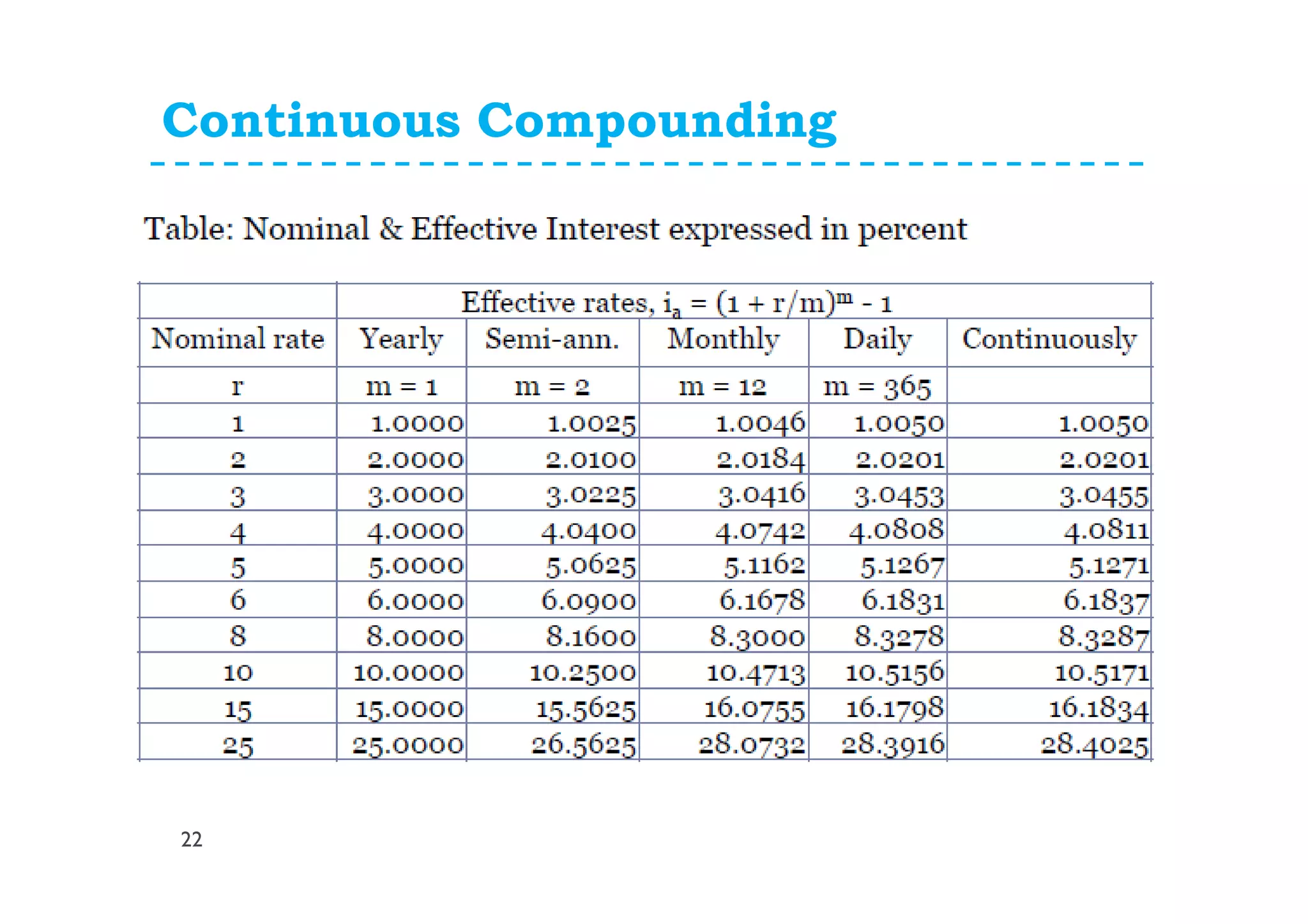

7

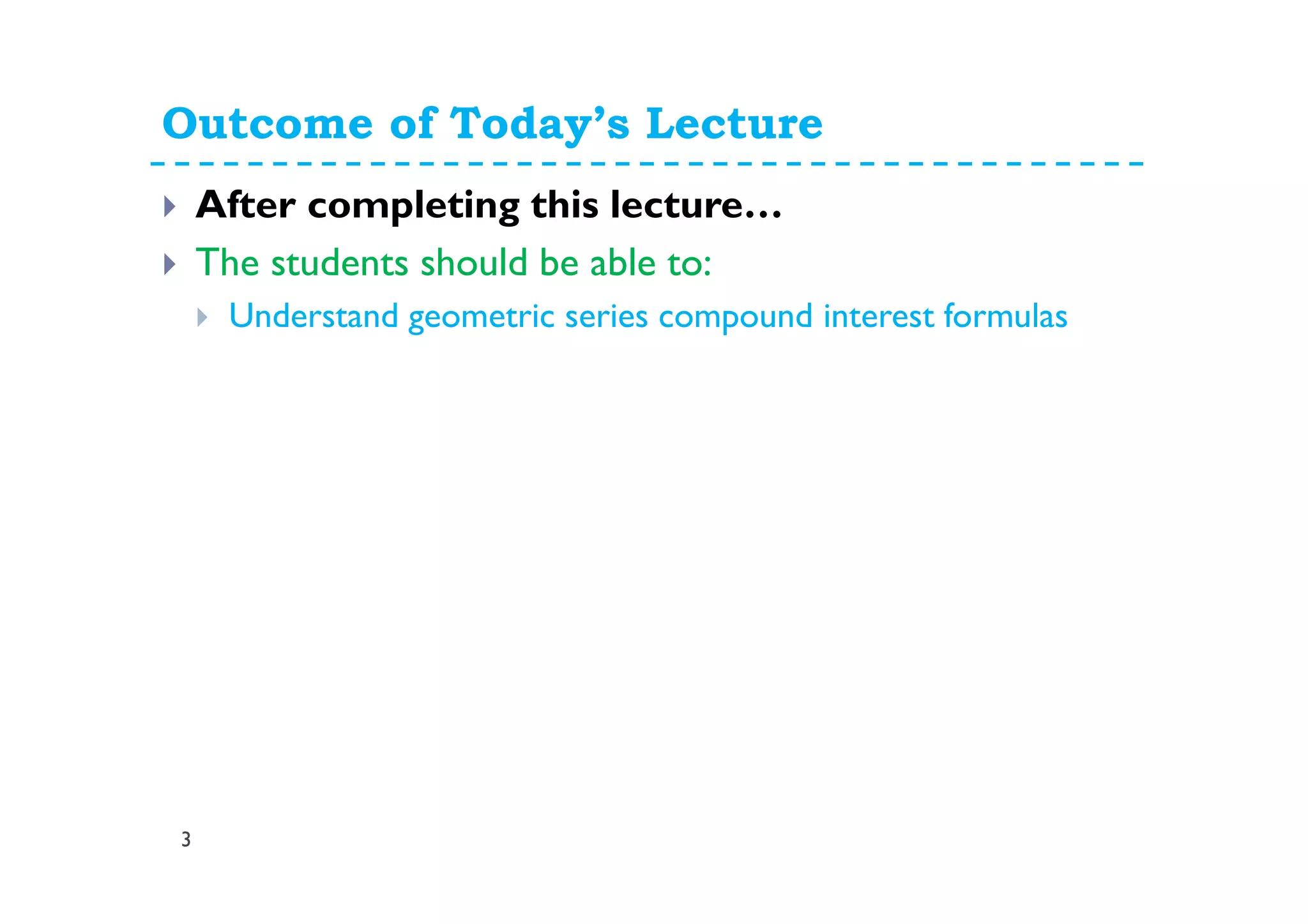

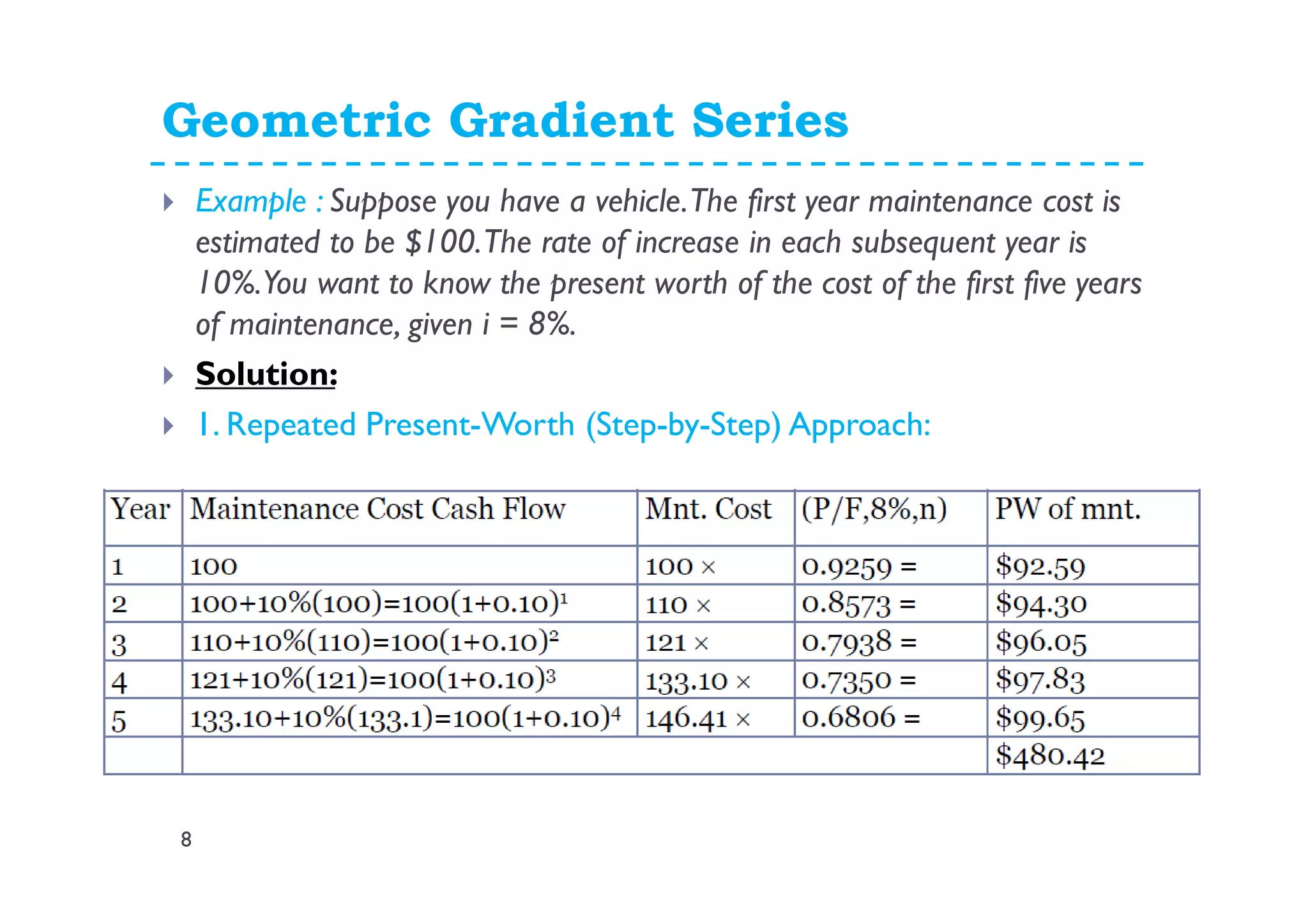

Subtract Equation (2) from Equation (1) to yield

( ) ( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

( ) ( ) ( )[ ]

( ) ( )

( )

−−+

++−

=

++−=−−+

++−=+−+

++−+=++−

−

−

−

−−−−

gi

ig

AP

igAgiP

igAAgPiP

igAiAigPP

nn

nn

nn

nn

11

111

11111

1111

11111

1

1

11

1

1

1

1

1

11

-

Eq. (3)

Eq. (4)Where gi ≠

Where is called geometric series

present worth factor and has notation

( ) ( )

( )

−−+

++−

−

gi

ig

nn

11

111

( )nigAP ,,,/

( ) ( ) ( ) ( ) ( )

( ) ( ) ( ) ( ) nnnn

igAigA

igAigAiAP

−−+−−

−−−

++++++

++++++++=

1111

...11111

1

1

12

1

32

1

21

1

1

1

( ) ( ) ( ) ( ) ( ) ( ) ( ) ( )

( ) ( ) ( ) ( ) 1

1

1

1

43

1

32

1

21

1

11

1111

...11111111

−−−−

−−−−

++++++

+++++++++=++

nnnn

igAigA

igAigAigAigP](https://image.slidesharecdn.com/5-150316005456-conversion-gate01/75/5-more-interest-formula-part-ii-7-2048.jpg)

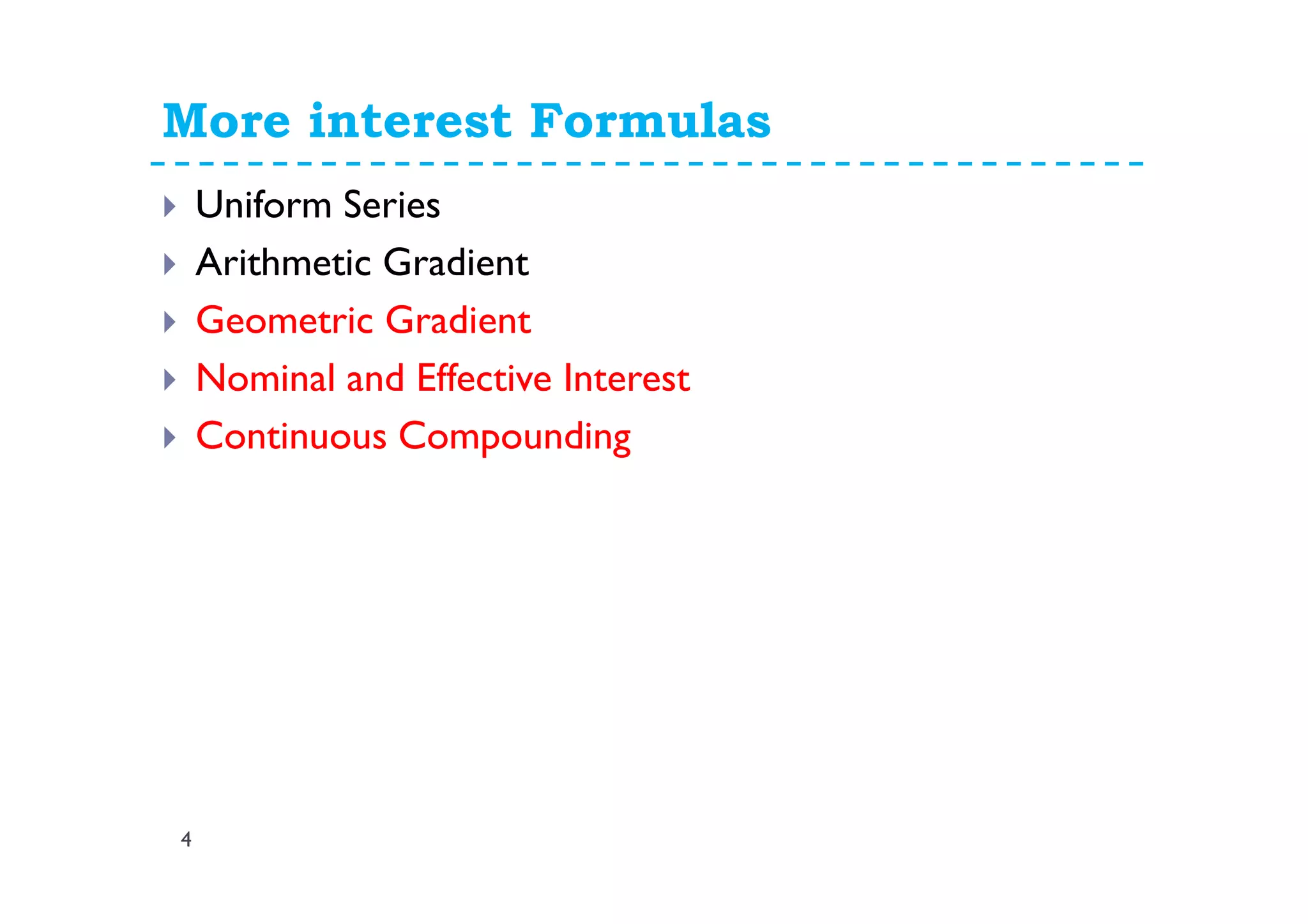

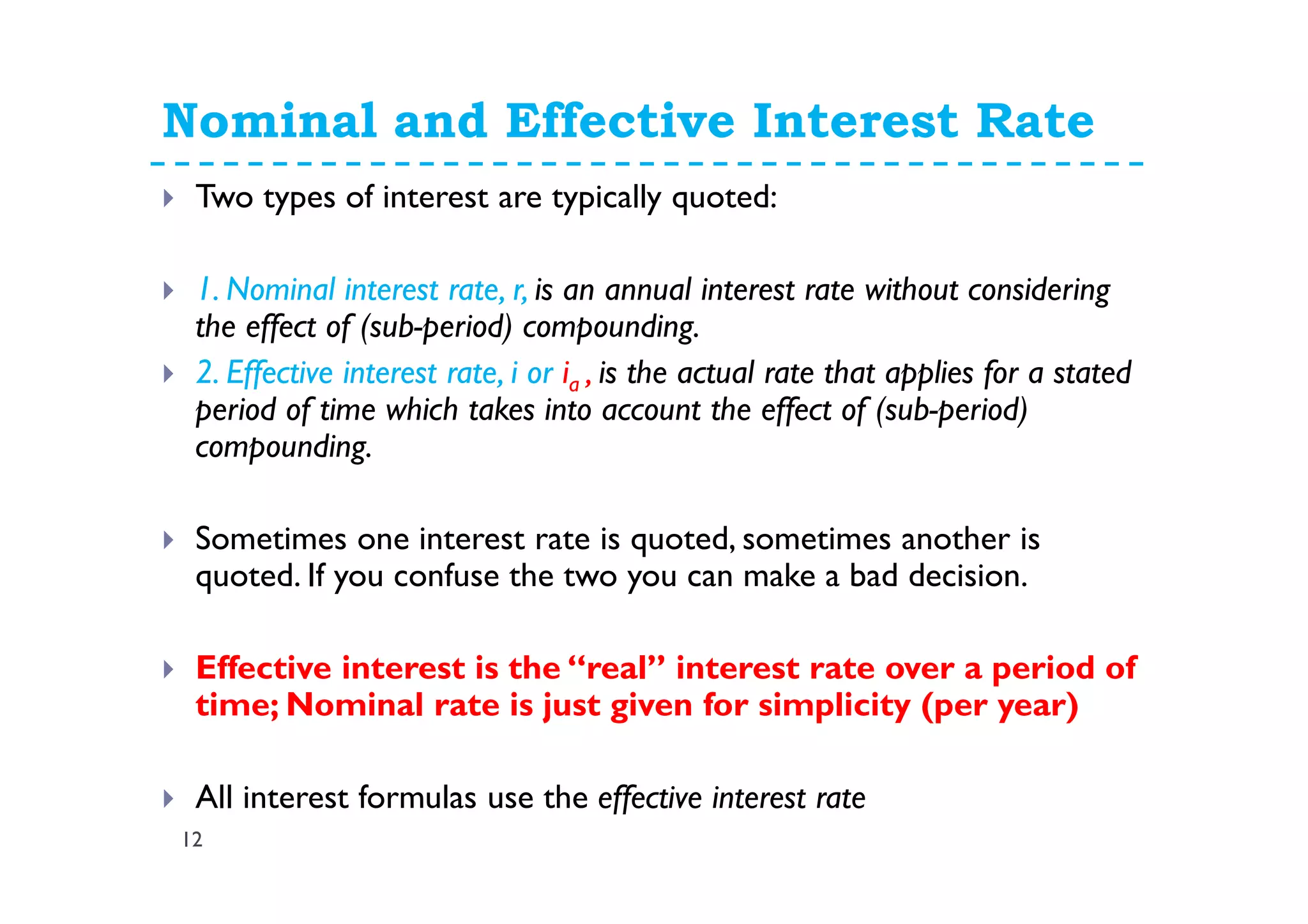

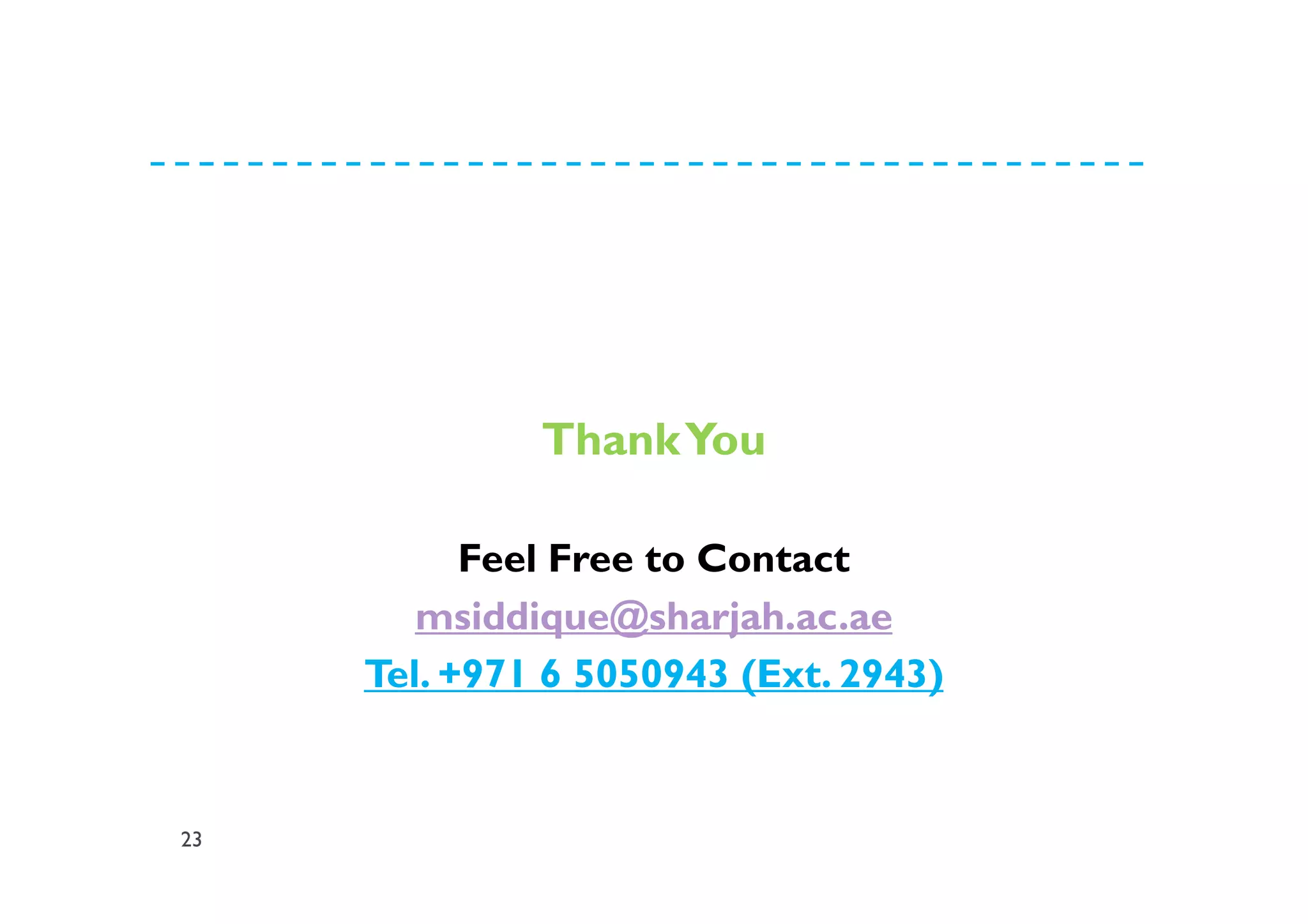

![Nominal and Effective Interest Rate

14

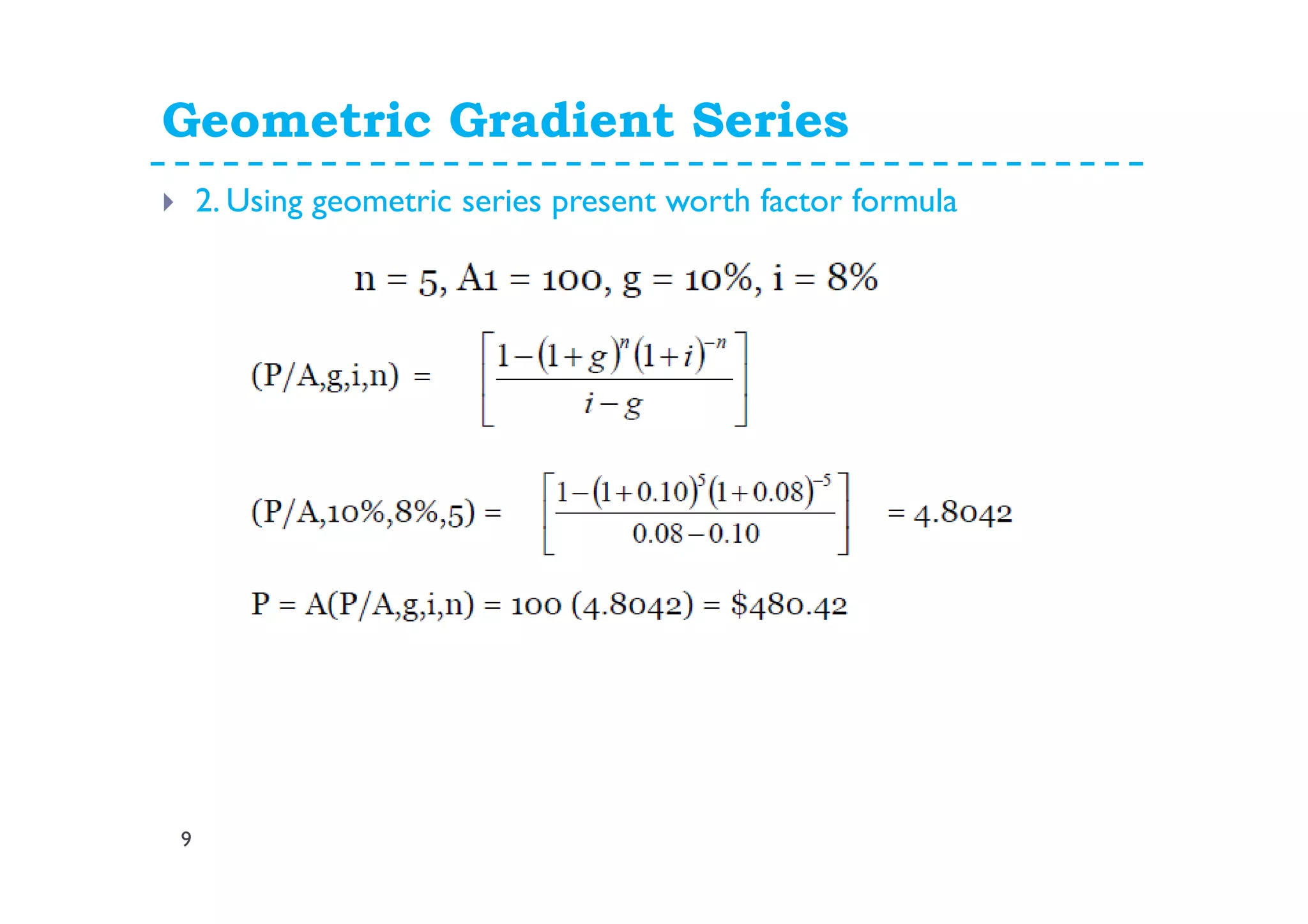

Example:

Given an interest rate of 12% per year, compounded quarterly:

Nominal rate=r = 12%

Compounding frequency=m=4

Effective (Actual) rate =r/m= 12%/4 = 3% per quarter

Effective rate per year = [1+(0.12/4)]4-1= 0.1255=12.55%

Investing $1 at 3% per quarter is equivalent to investing $1 at 12.55%

annually](https://image.slidesharecdn.com/5-150316005456-conversion-gate01/75/5-more-interest-formula-part-ii-14-2048.jpg)

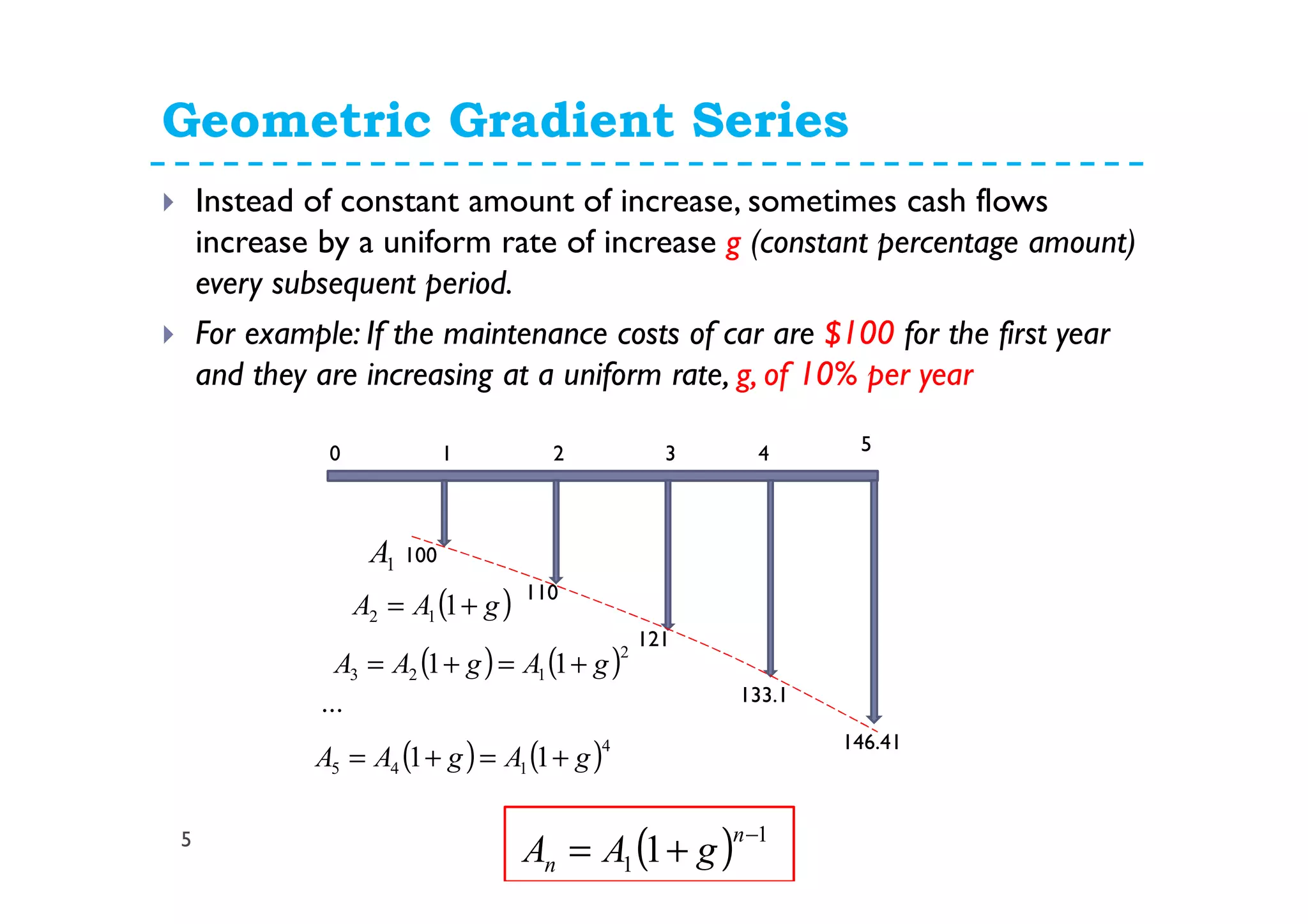

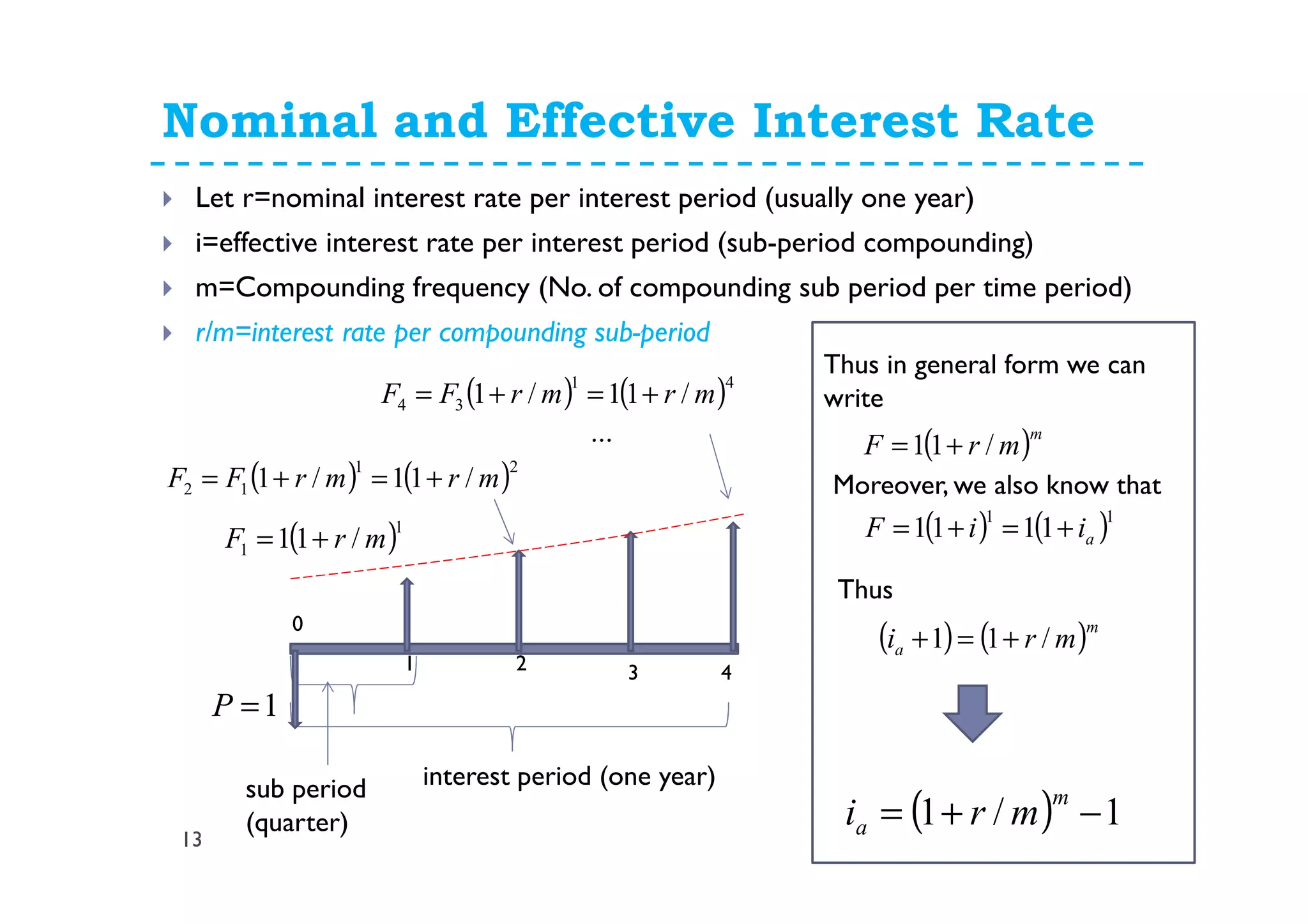

![Nominal and Effective Interest Rate

17

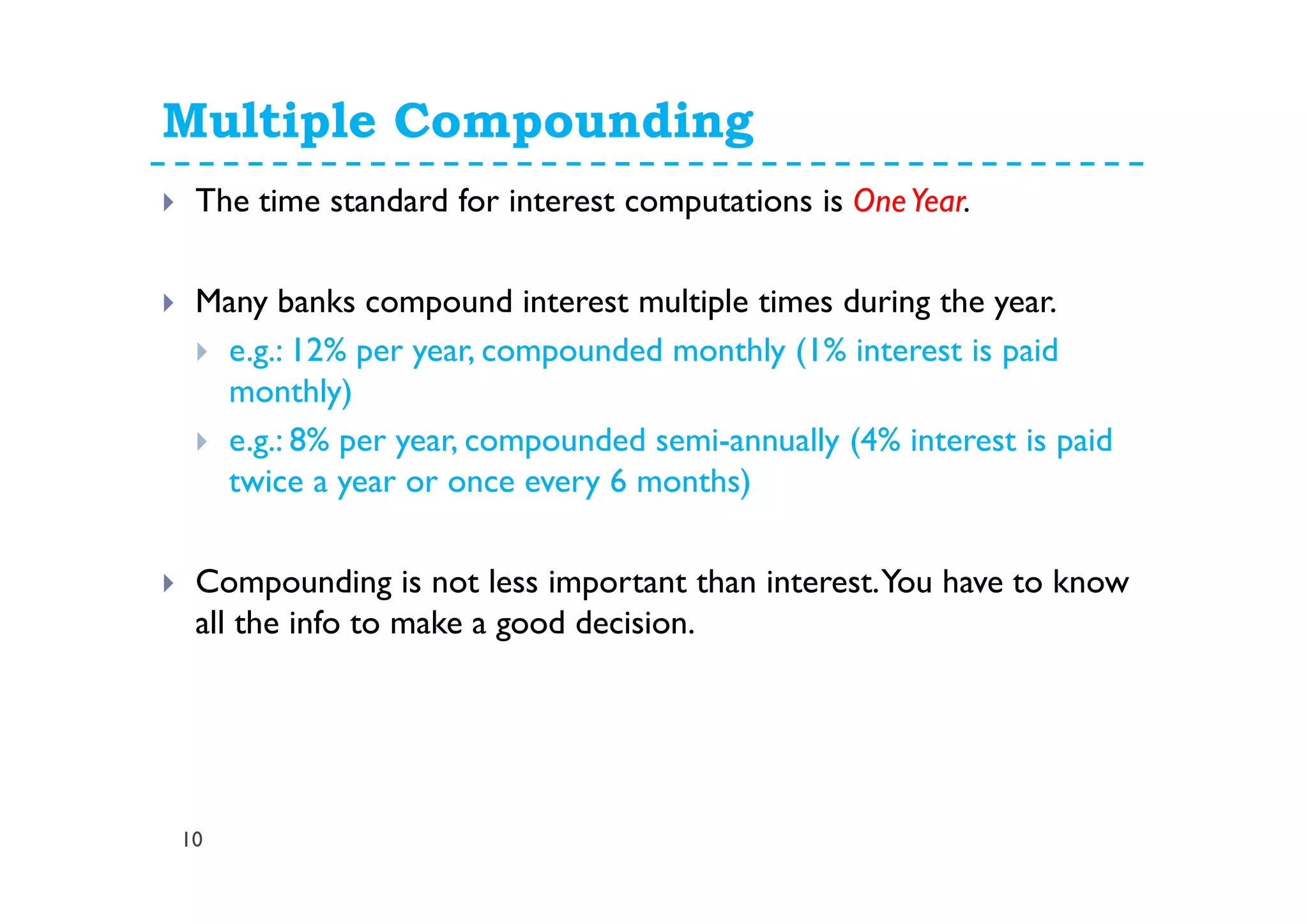

Example 4-15: A loan shark lends money on the following terms.“If I

give you $50 on Monday, then you give back $60 the following Monday.”

Solution

1.What is the nominal rate, r ?

The loan shark charges i= 20% a week:

60 = 50 (1+i) [Note we have solved 60 = 50(F/P,i,1) for i]

i= 0.2

We know m = 52, so r = 52 x i= 10.4, or 1,040% a year

2.What is the effective rate, ia?

ia= (1 + r/m)m–1 = (1+10.4/52)52–1 =13,104

This means about 1,310,400 % a year !!!!](https://image.slidesharecdn.com/5-150316005456-conversion-gate01/75/5-more-interest-formula-part-ii-17-2048.jpg)

This document contains lecture notes on interest formulas including geometric series, uniform series, arithmetic gradient, geometric gradient, nominal and effective interest rates, and continuous compounding. It provides examples and explanations of formulas for present worth, future worth, and compound interest calculations for situations involving constant and increasing cash flows over time with single-rate and multiple compounding periods.

![Engineering Economics: Solved exam problems [ch1-ch4]](https://cdn.slidesharecdn.com/ss_thumbnails/solvedexamproblemsch1-ch4-200220070043-thumbnail.jpg?width=640&height=640&fit=bounds)