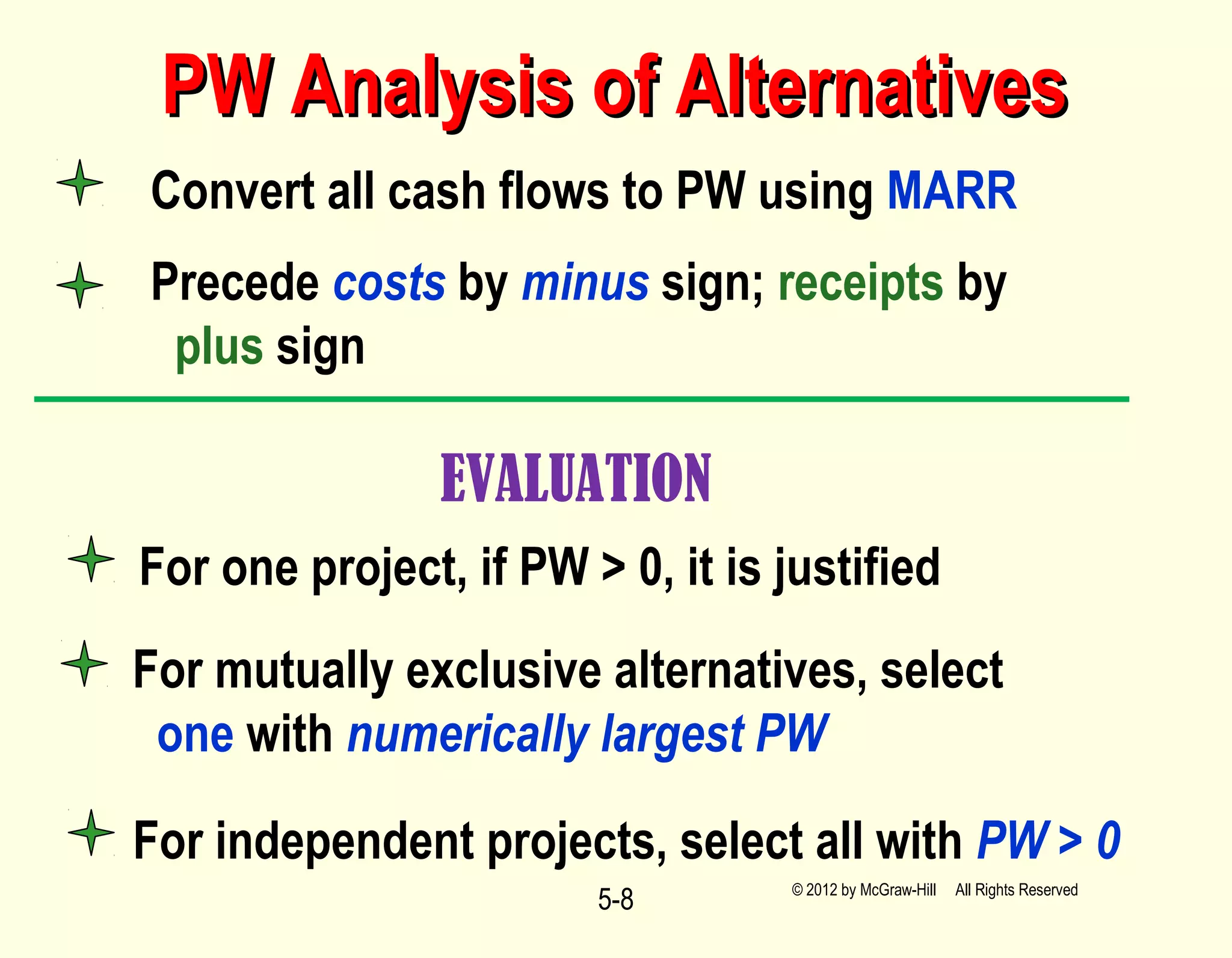

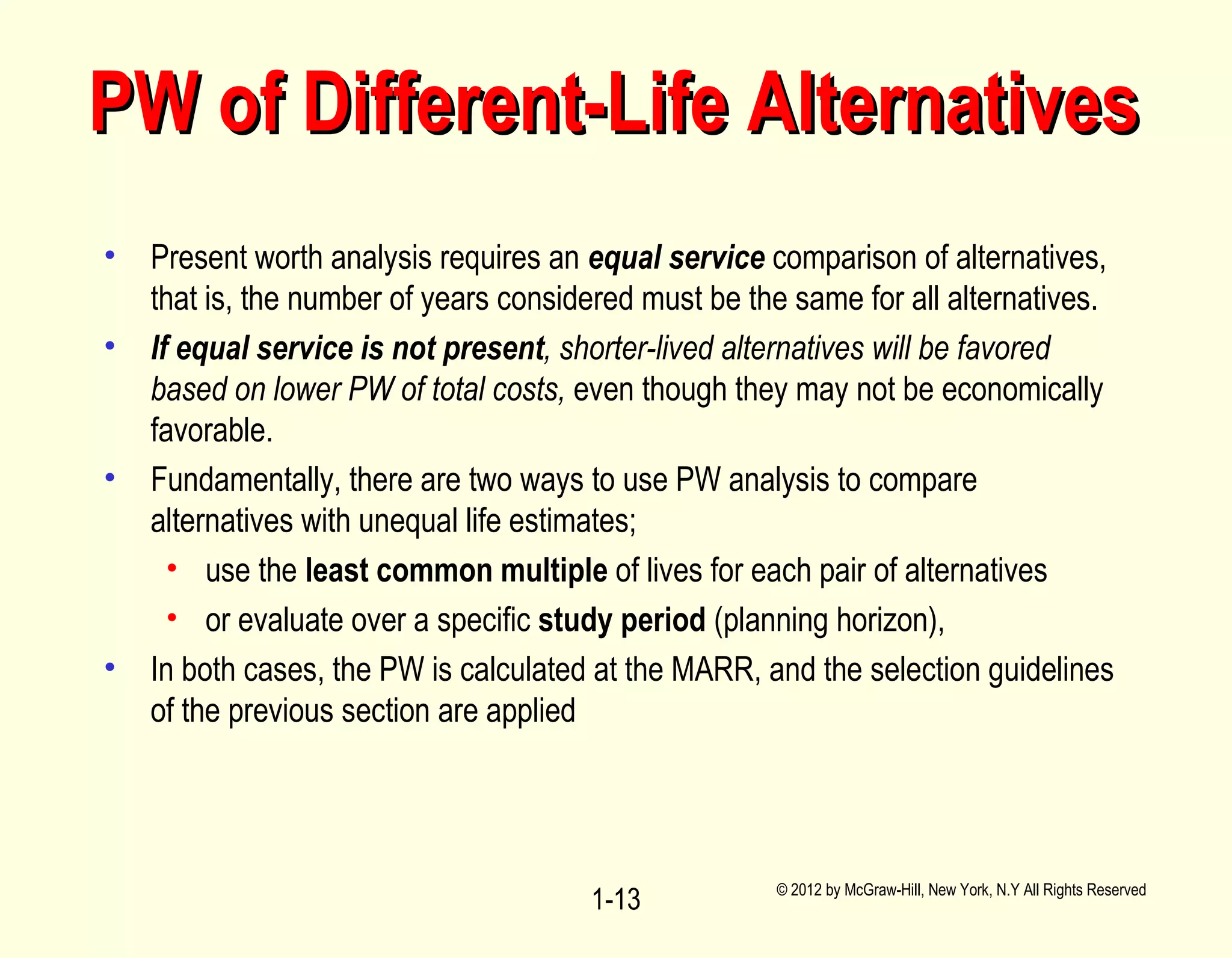

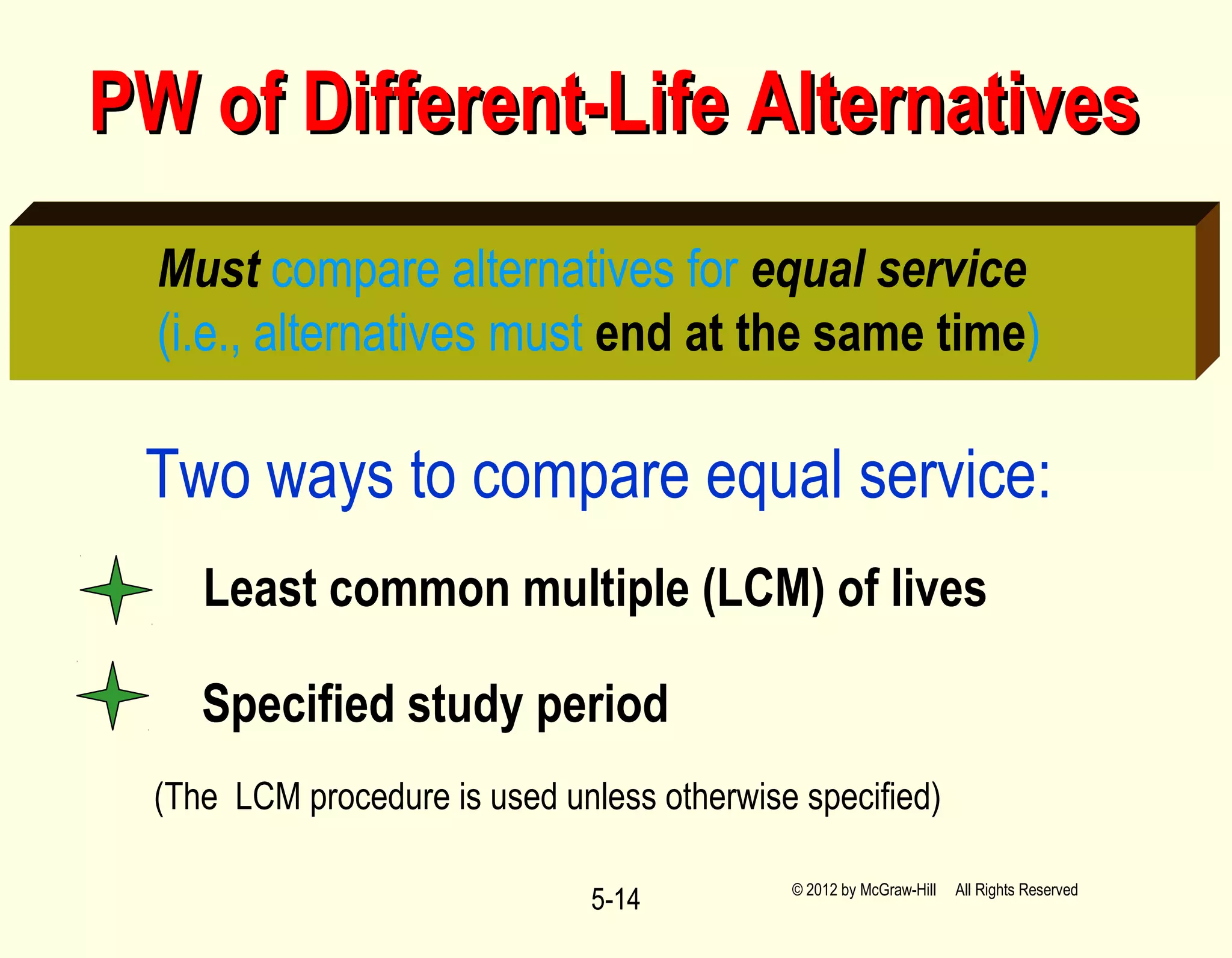

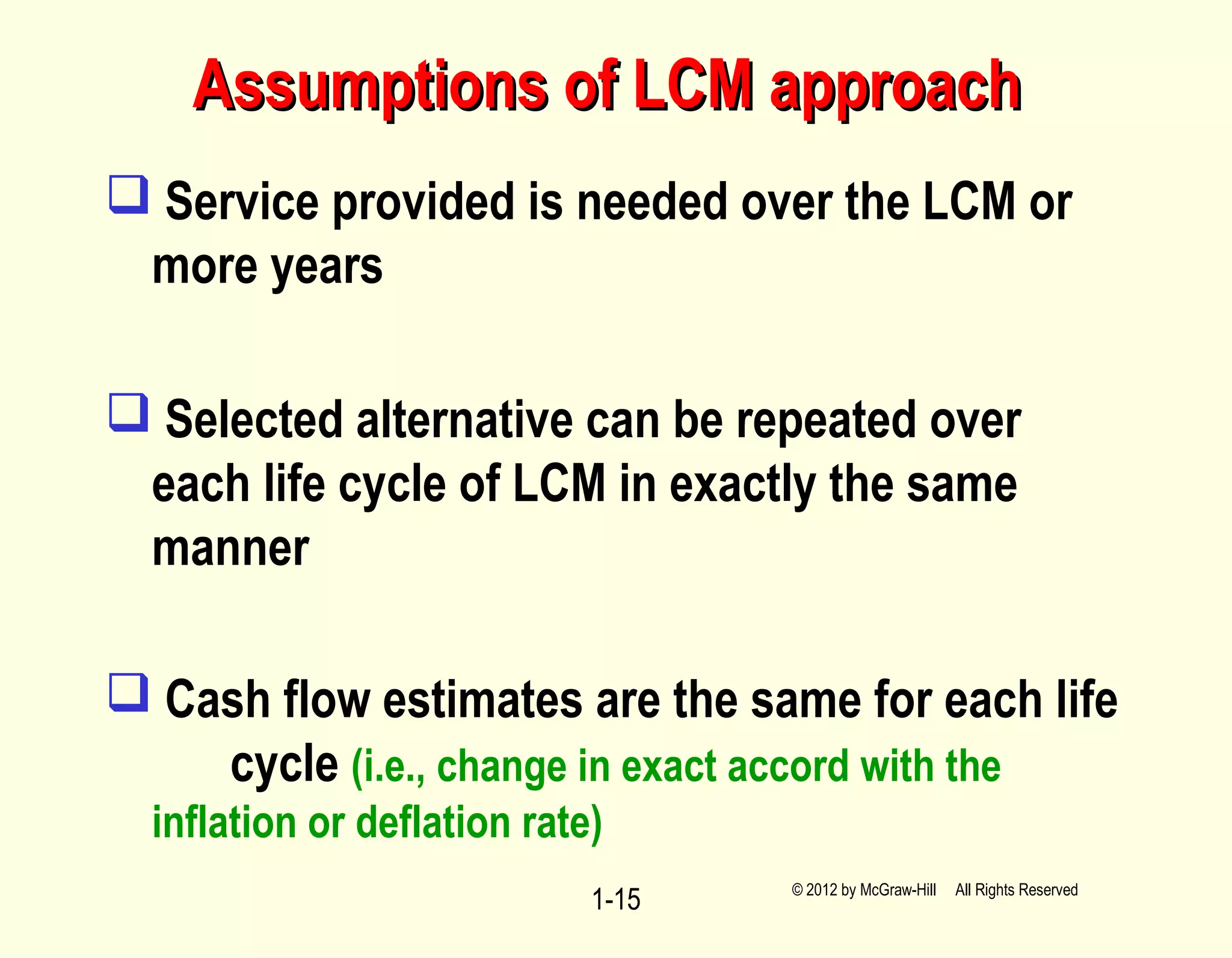

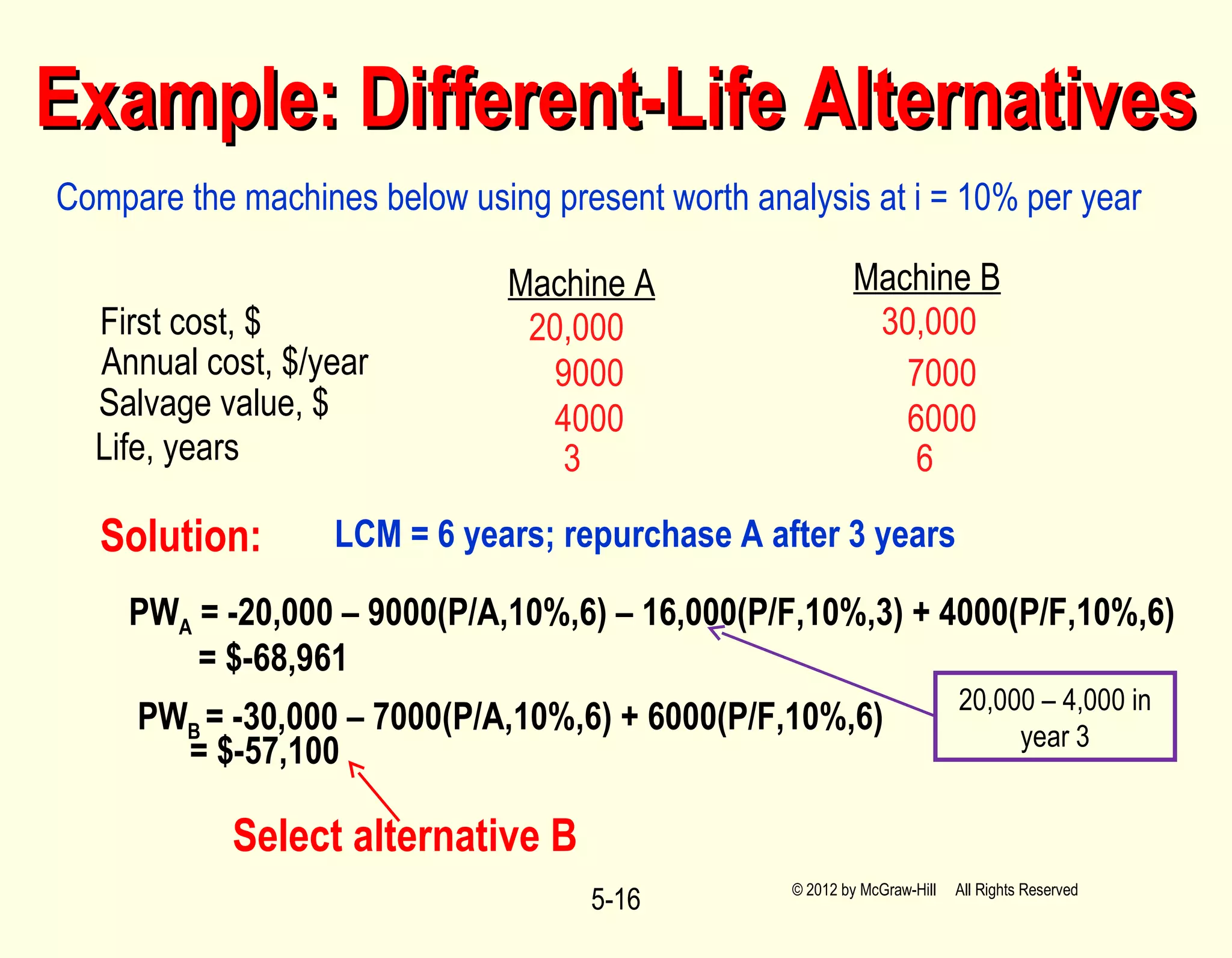

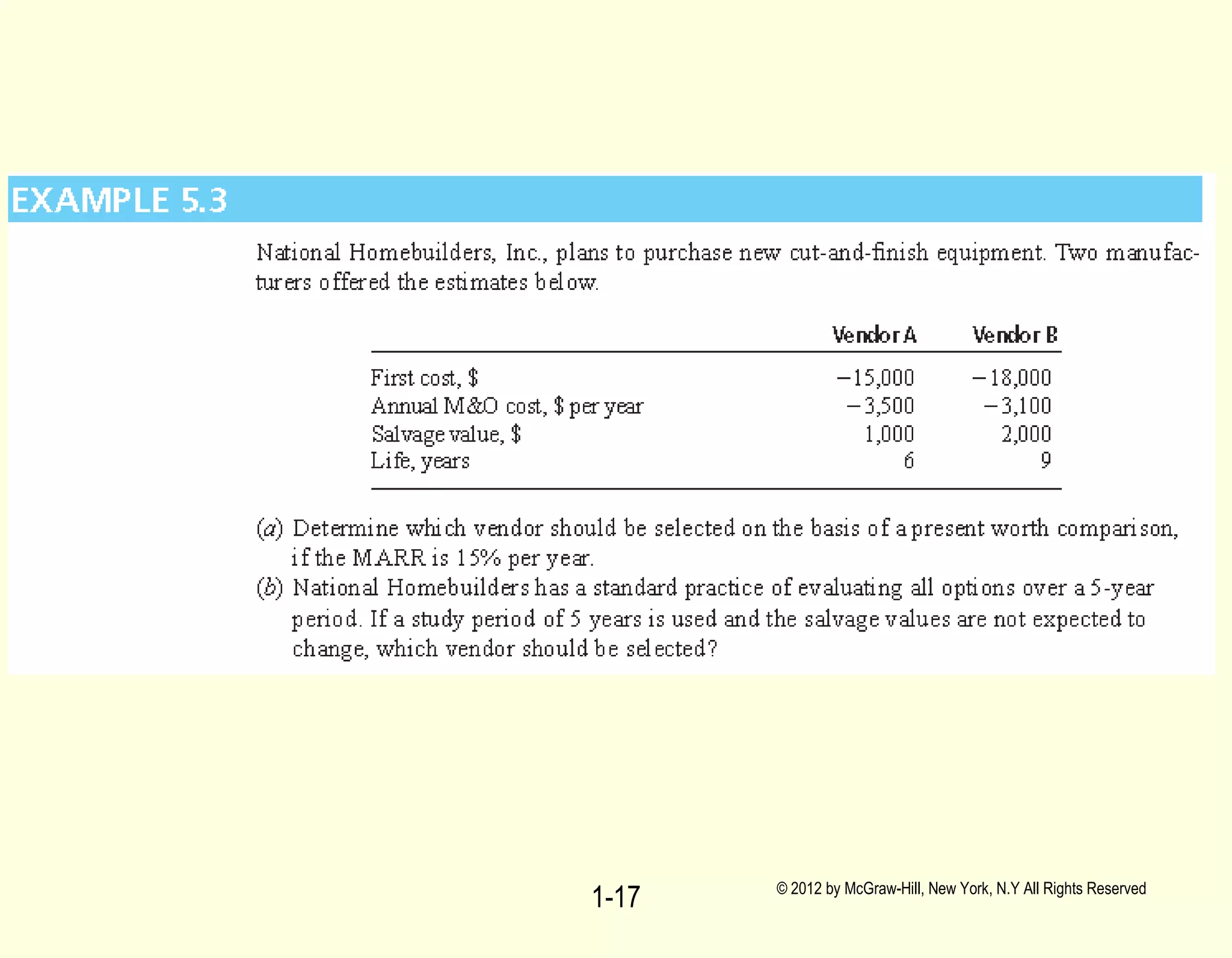

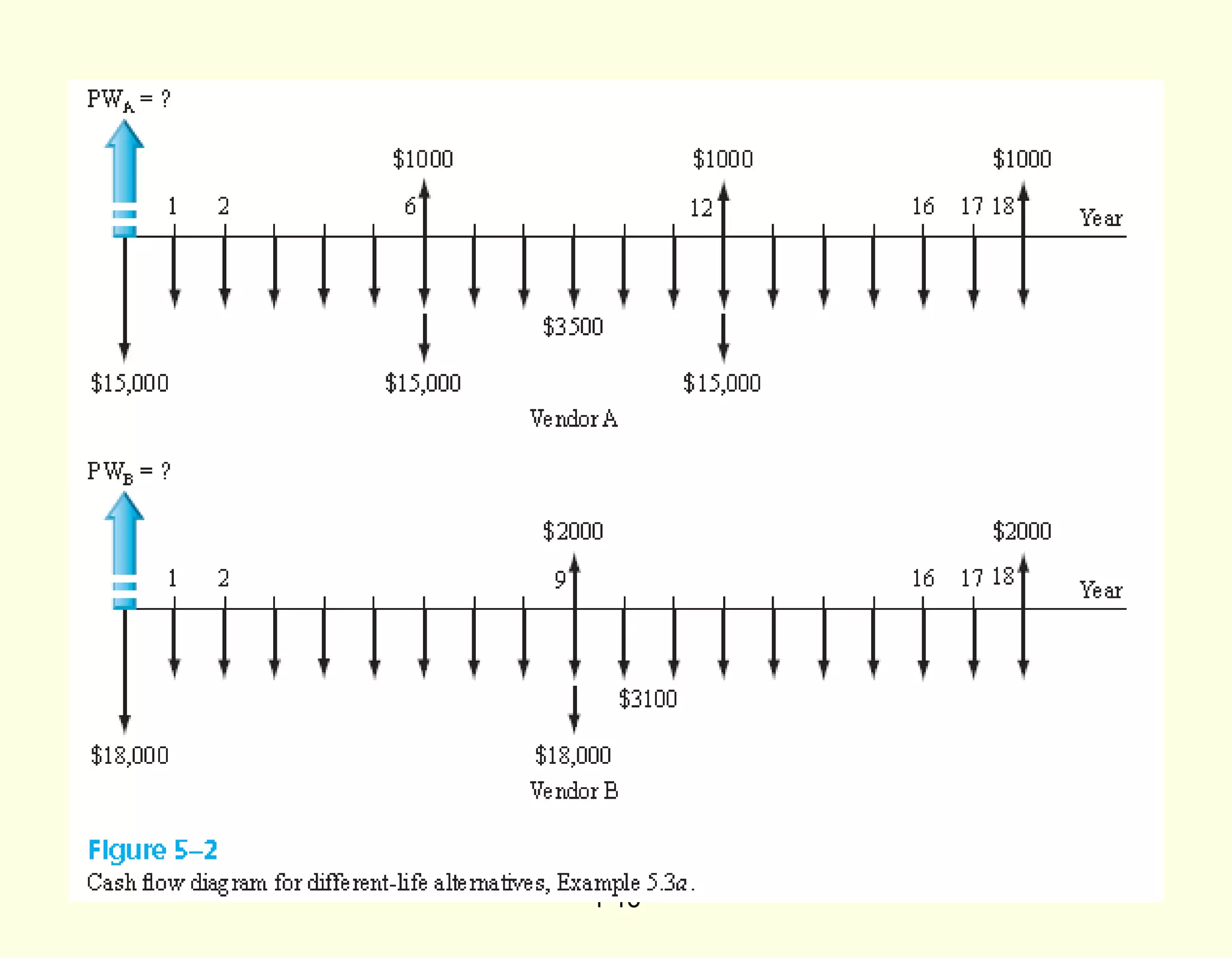

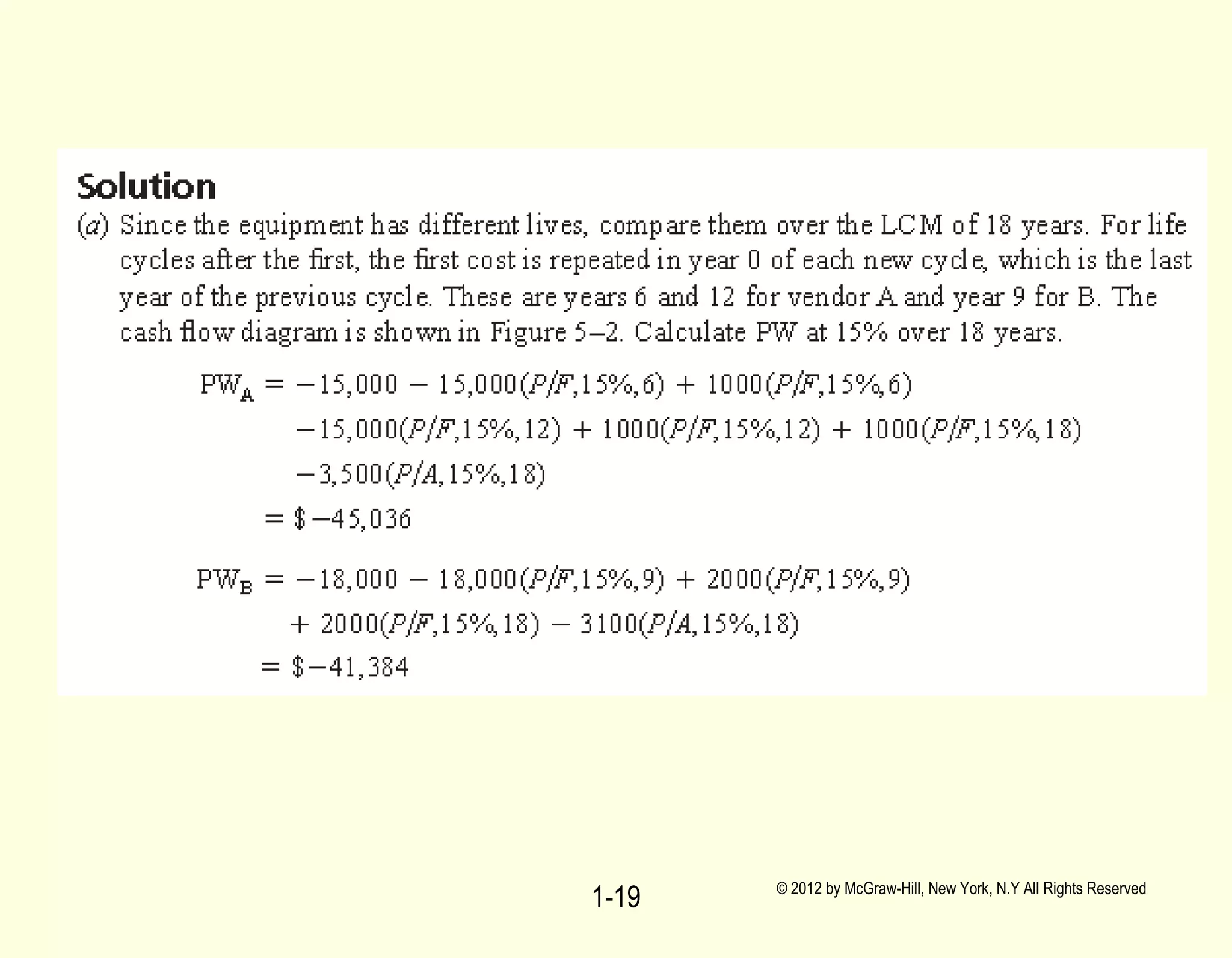

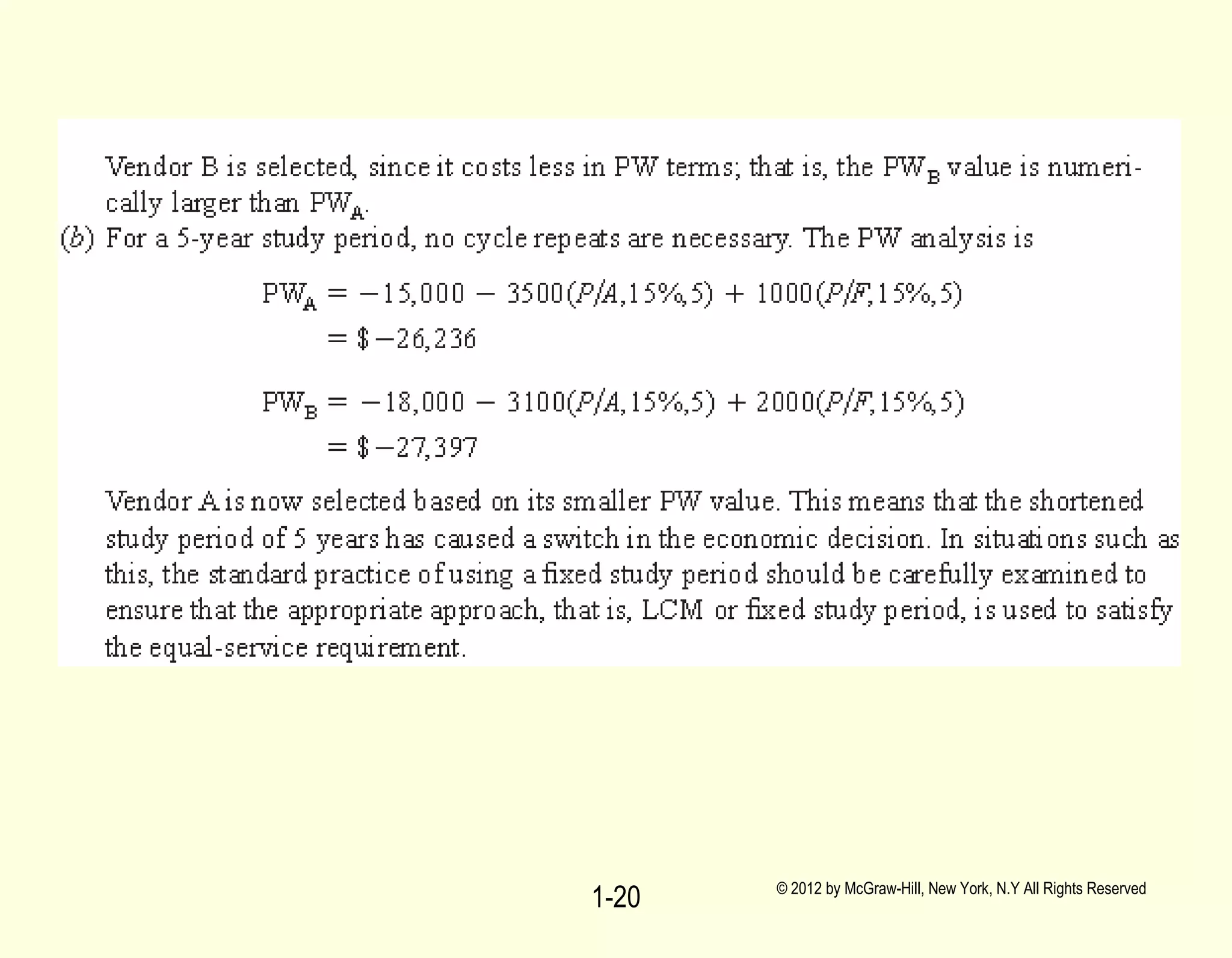

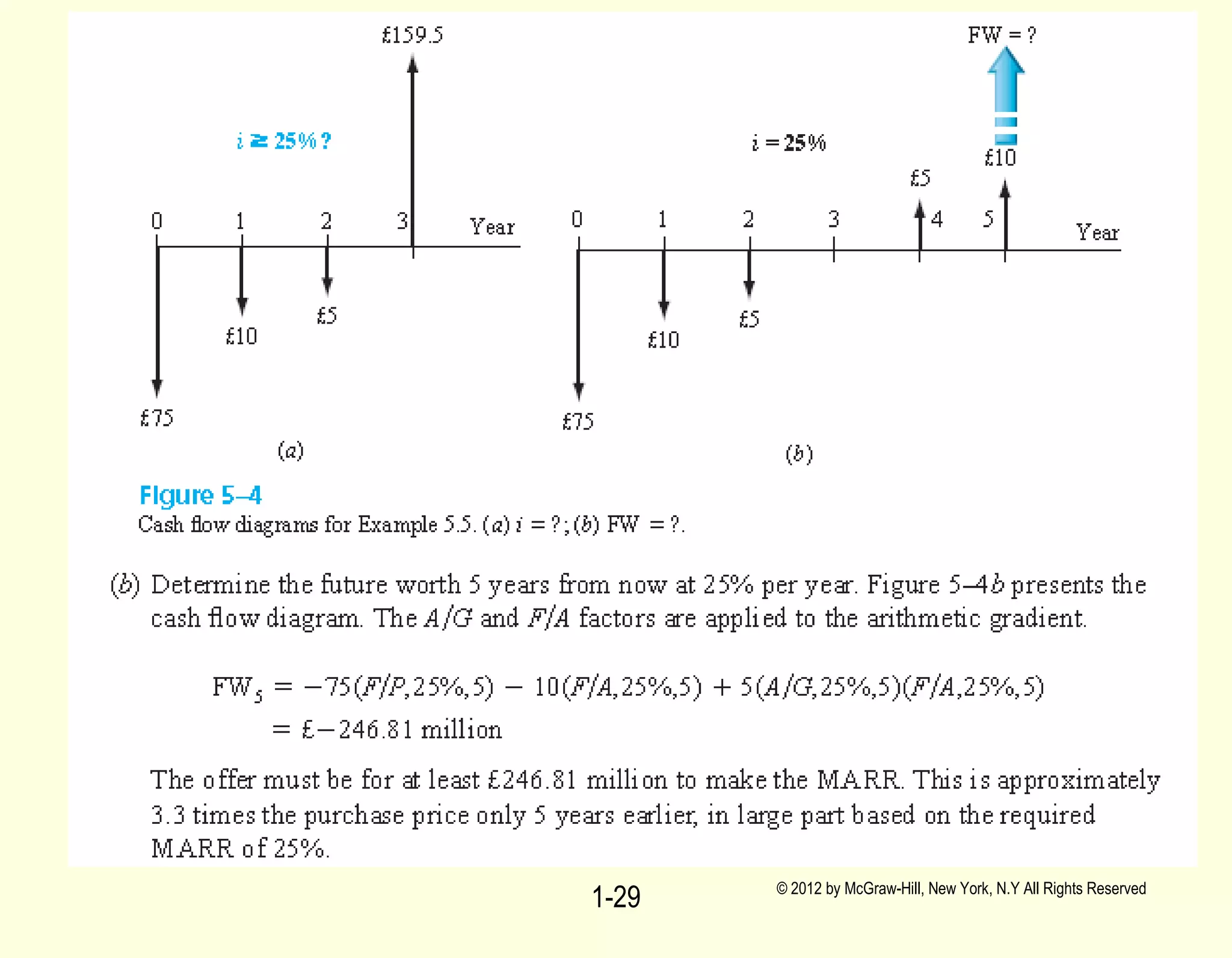

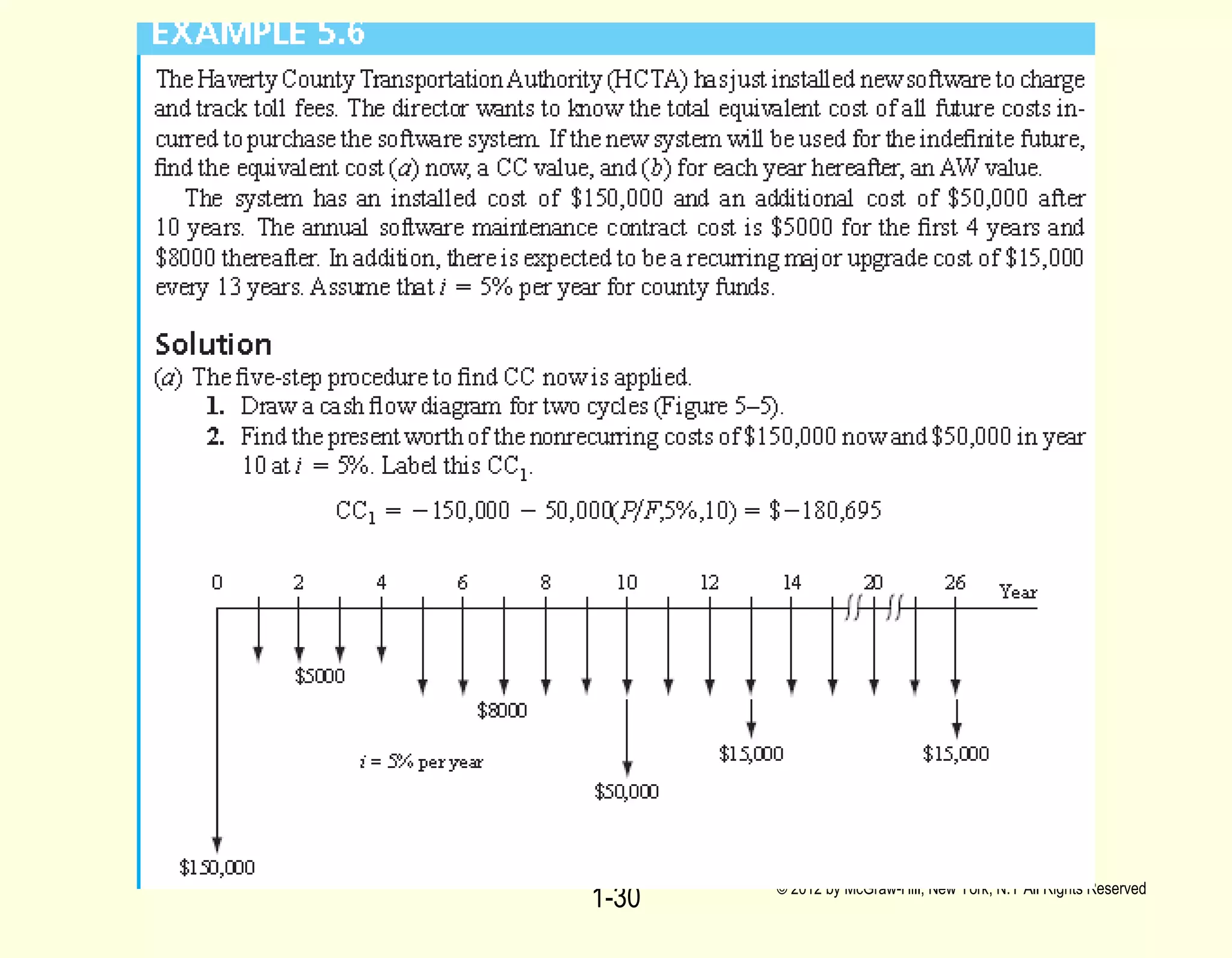

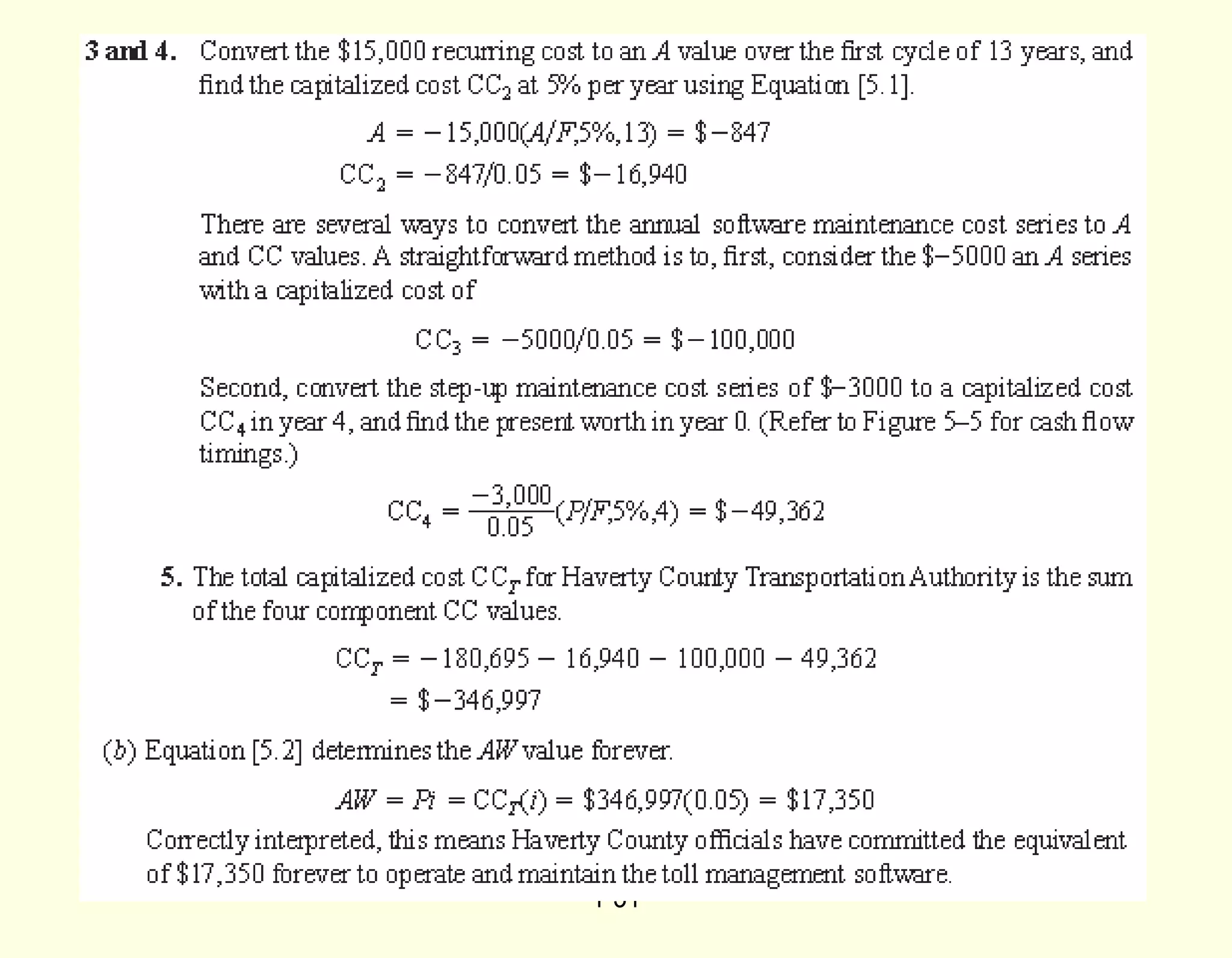

1. The document discusses various methods for analyzing engineering project alternatives using present worth analysis, including analyzing alternatives with equal lives, different lives, and infinite lives.

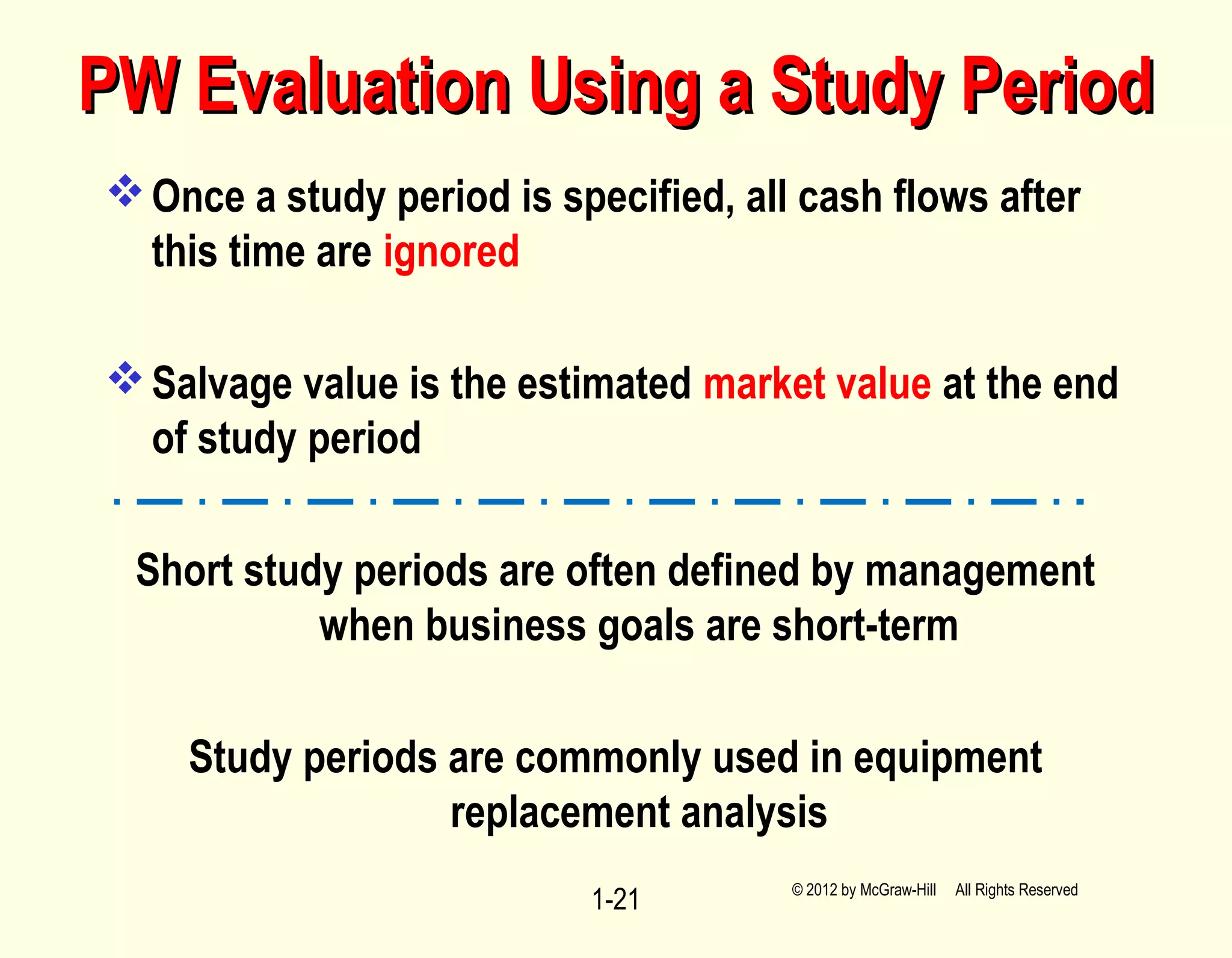

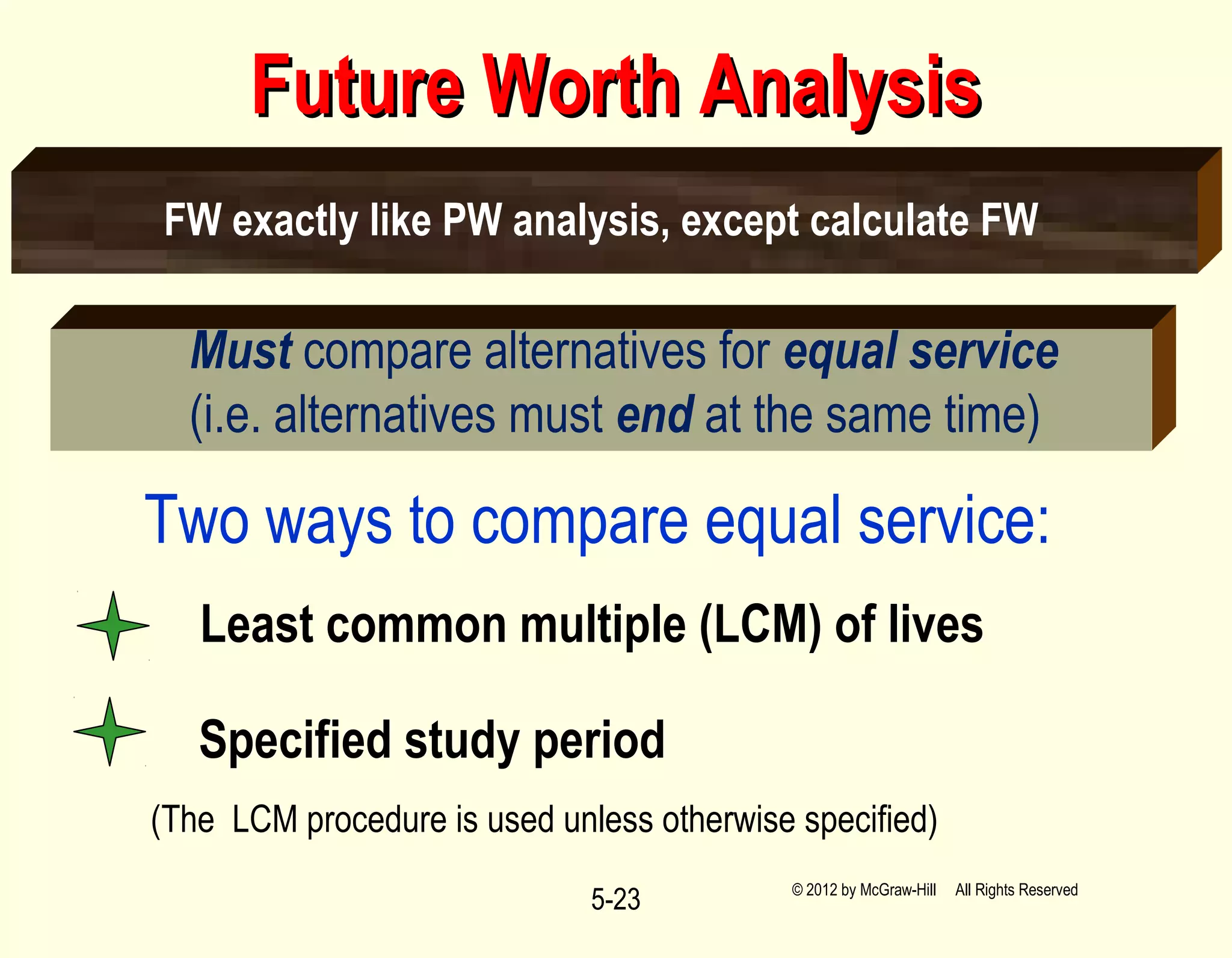

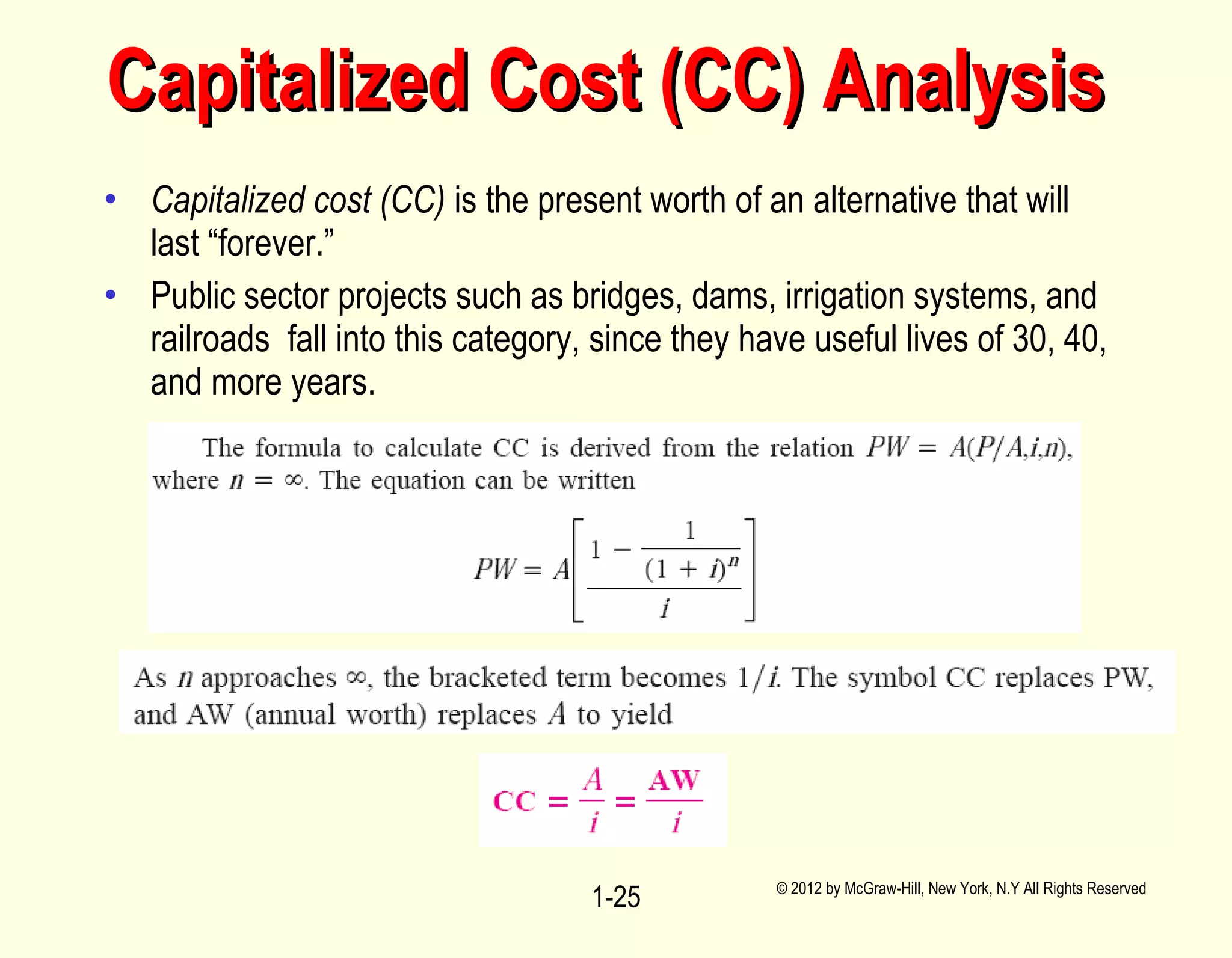

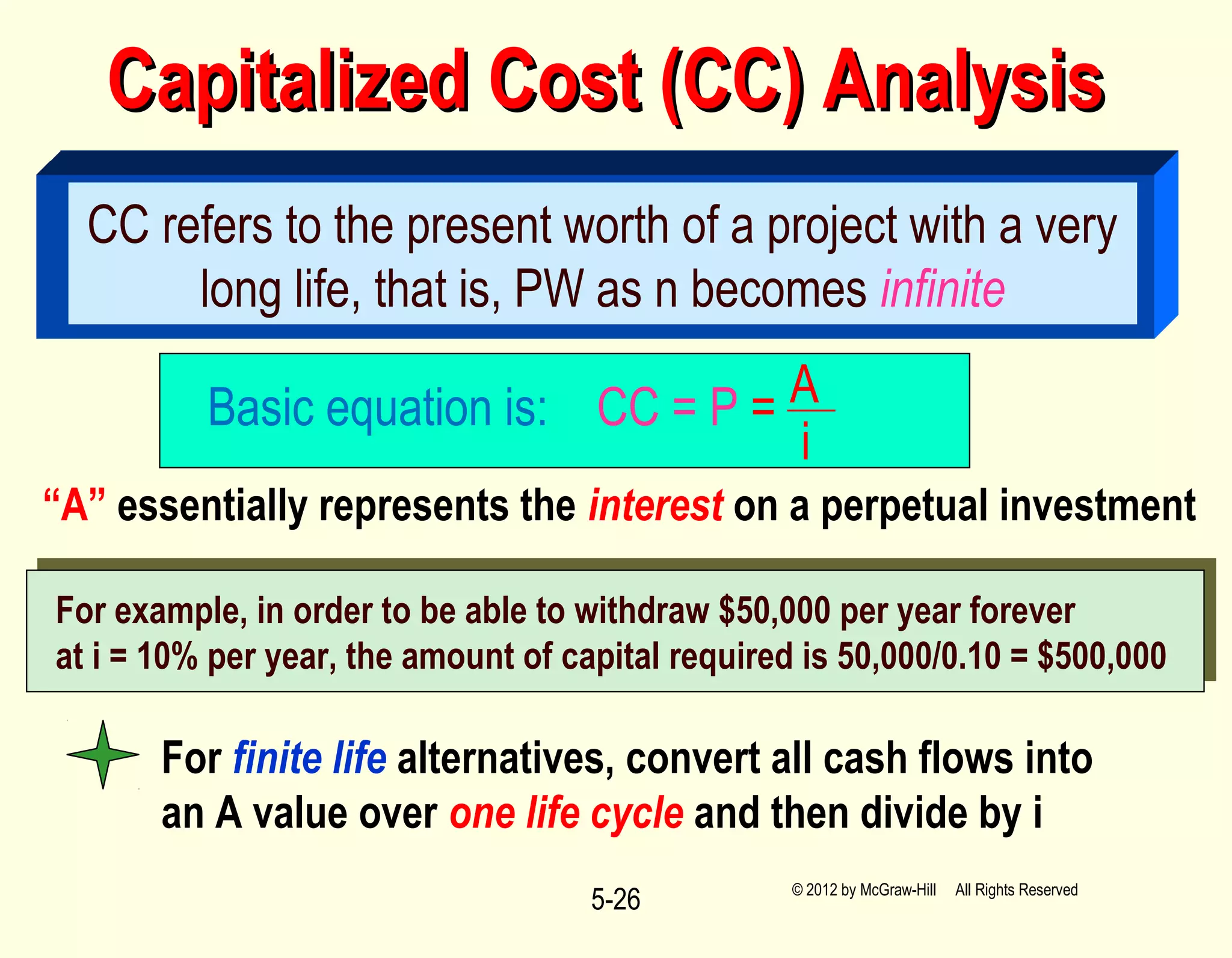

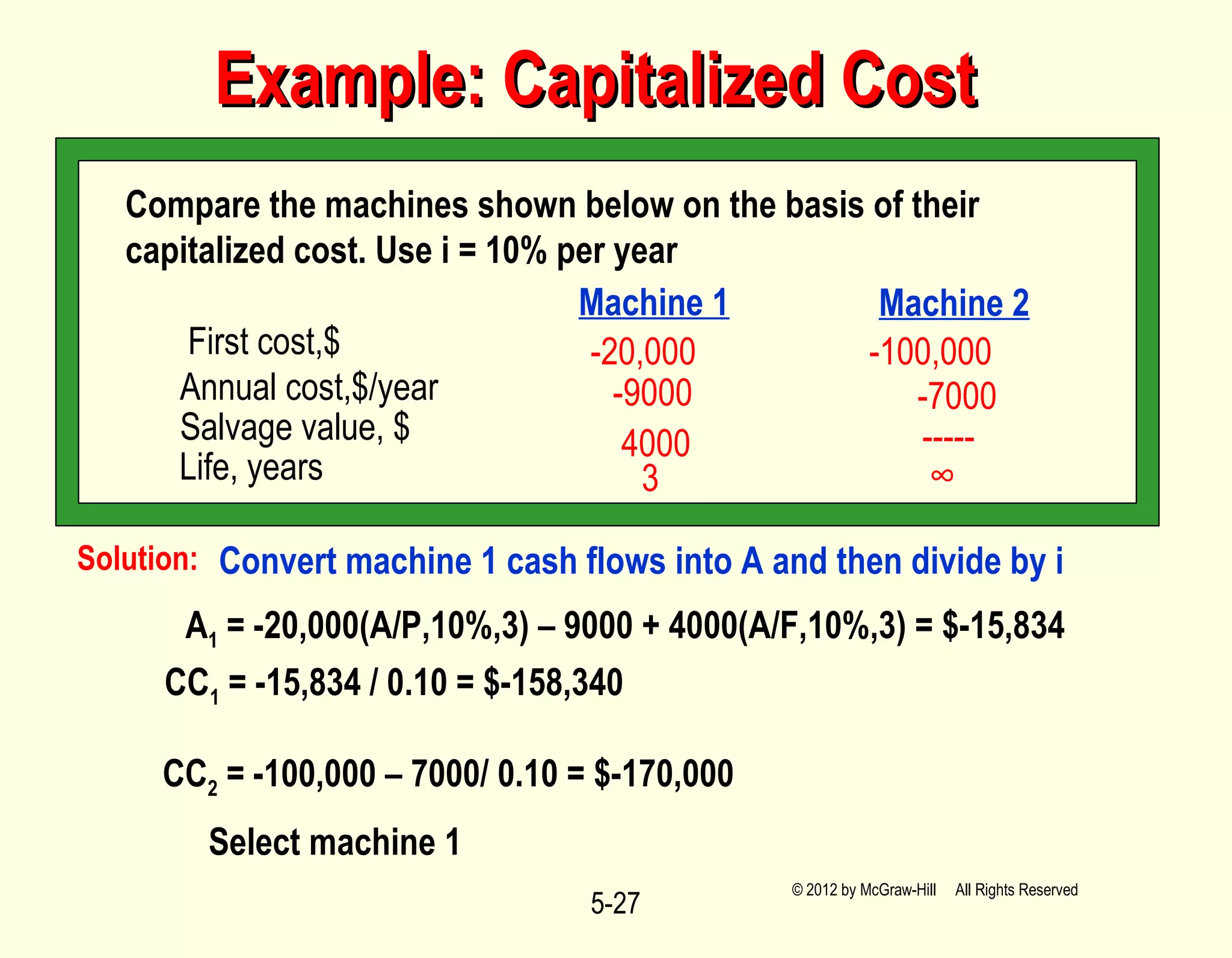

2. Key methods include using the least common multiple of lives or a specified study period to convert alternatives to equal service for comparison, and calculating the capitalized cost for alternatives with infinite lives.

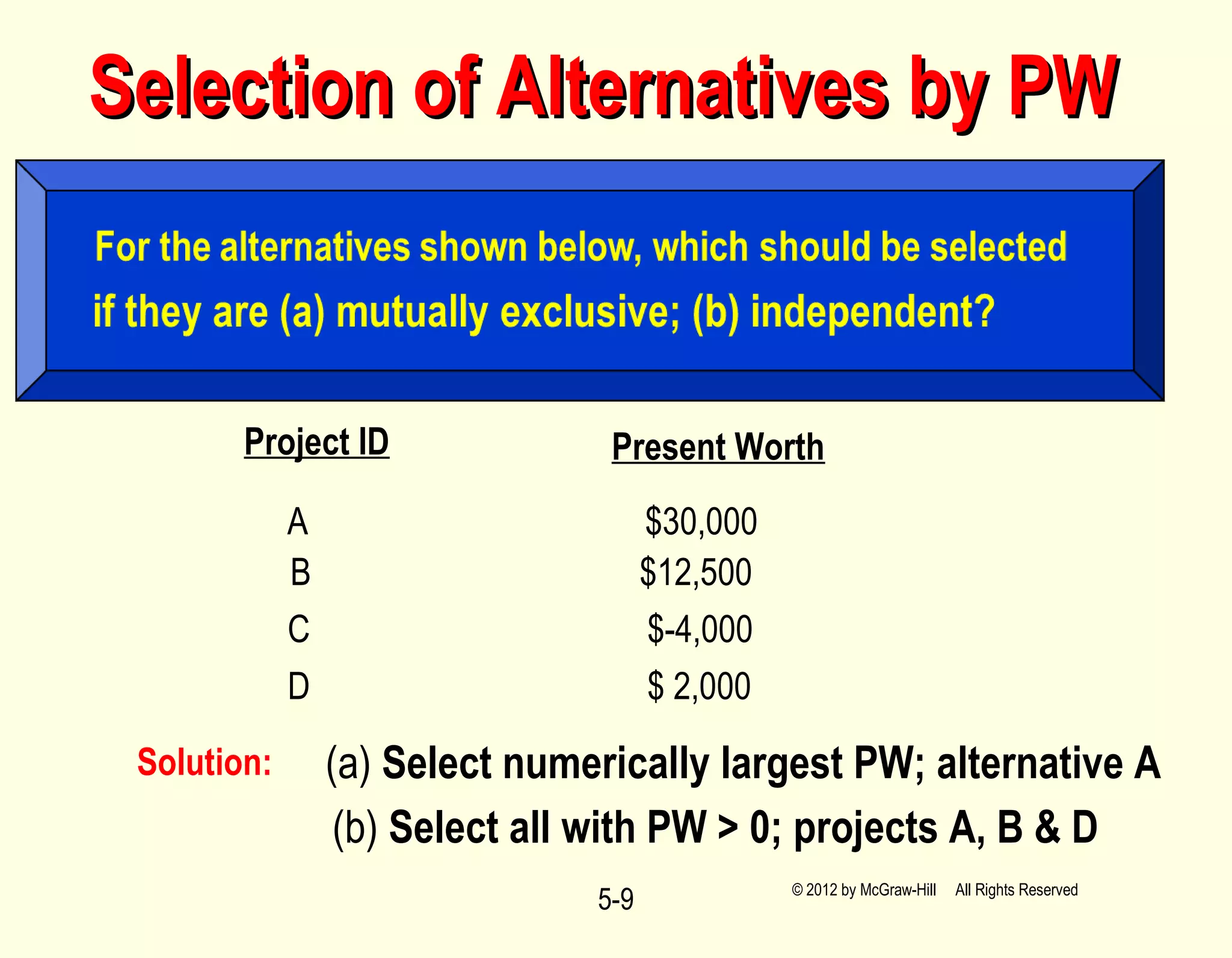

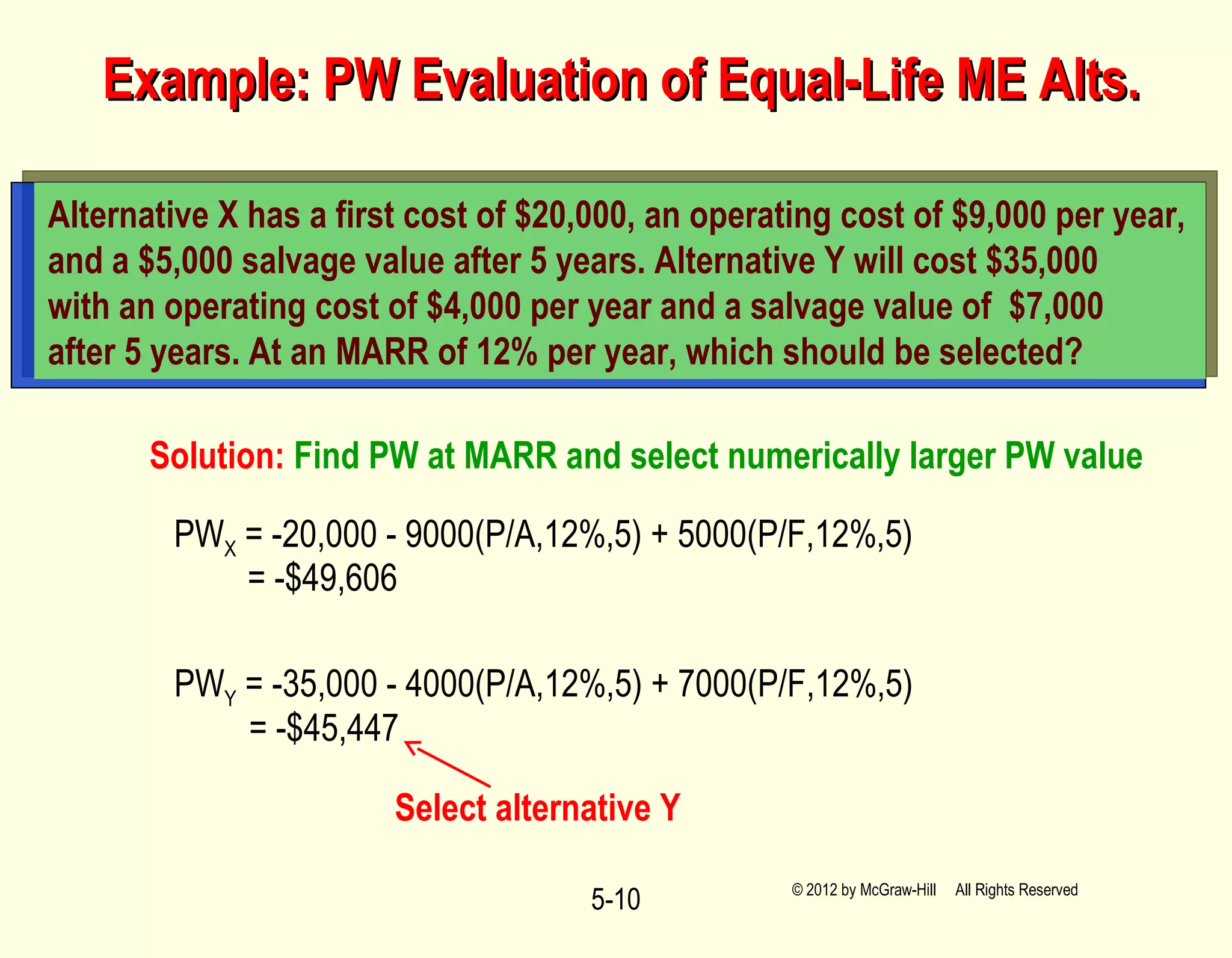

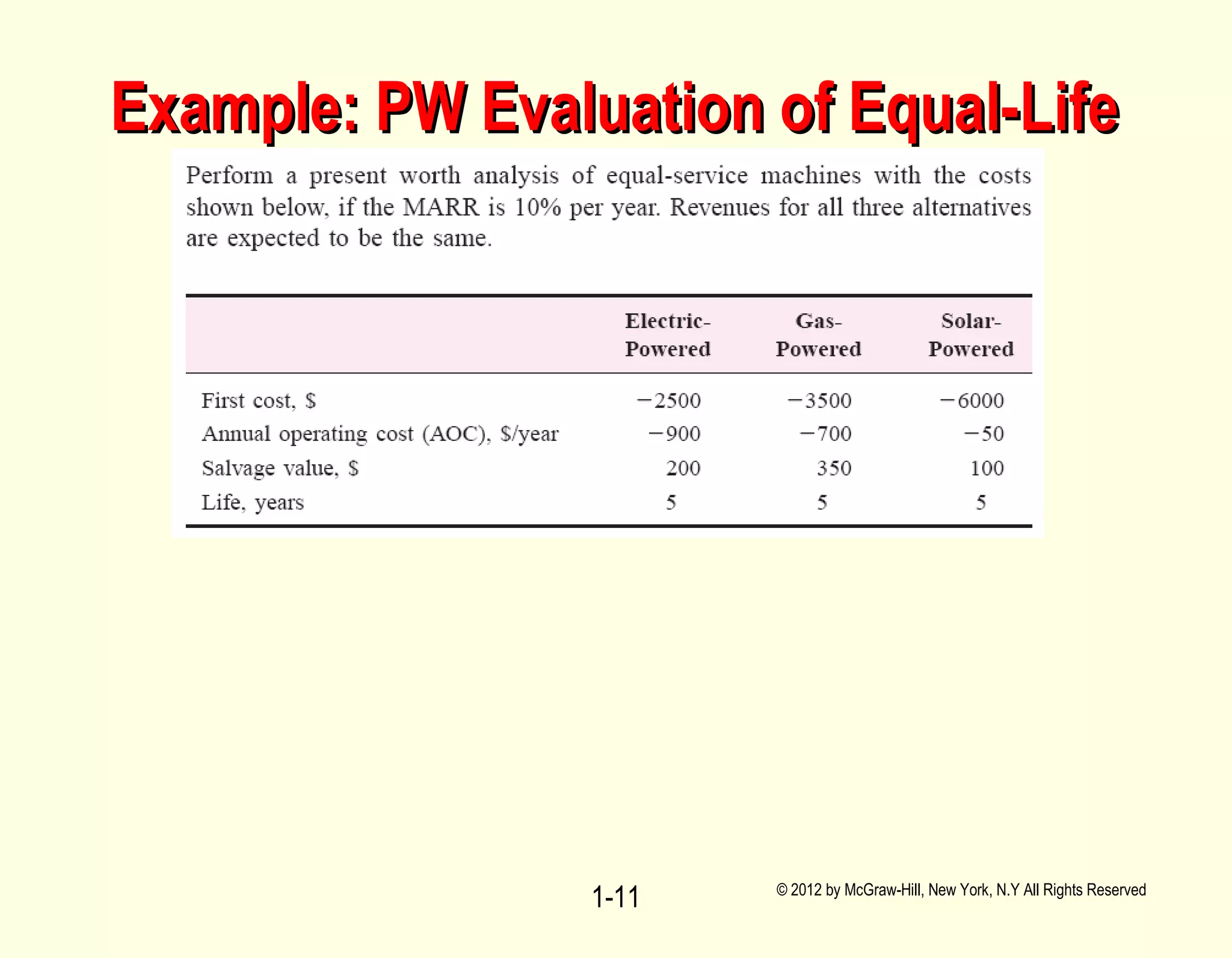

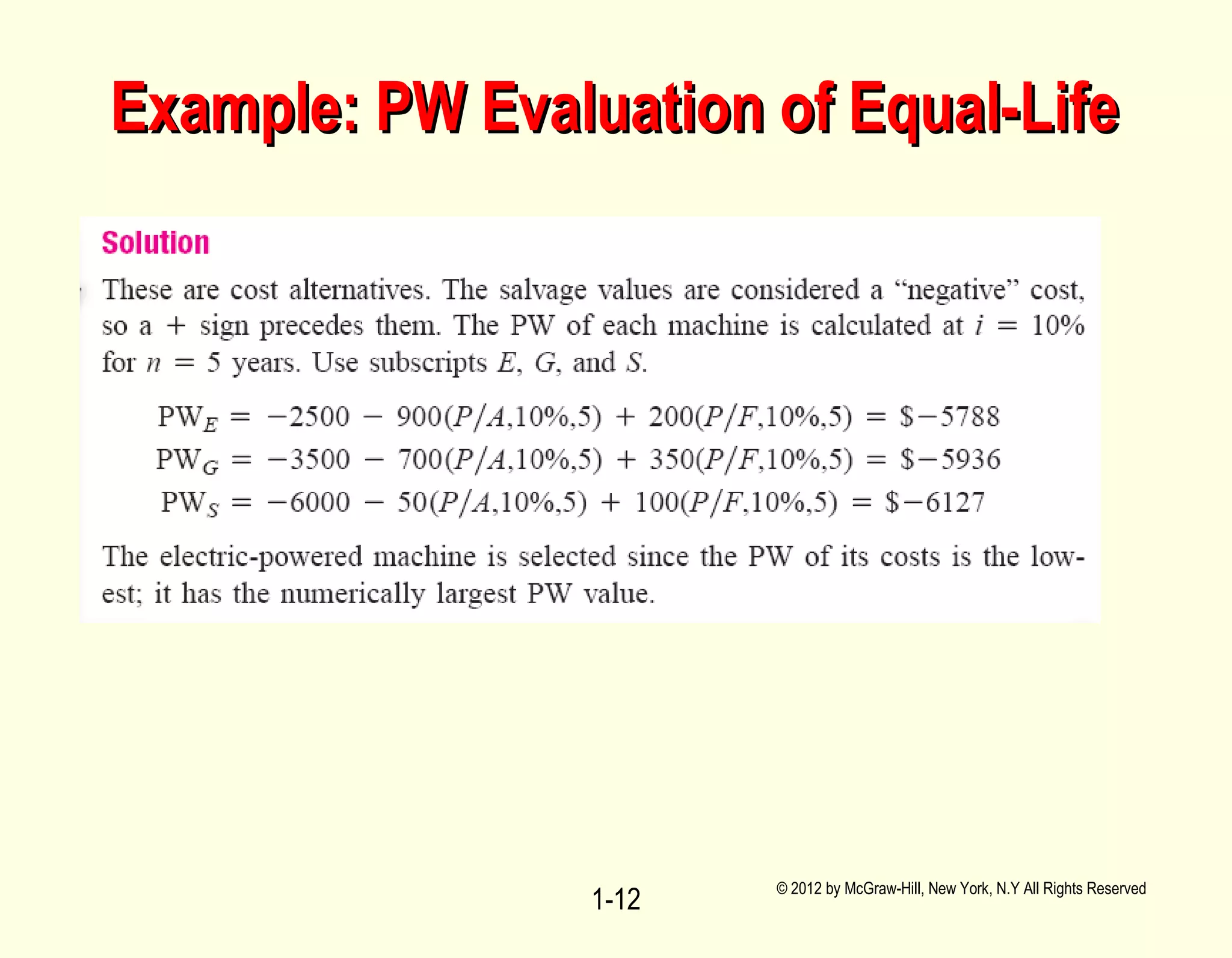

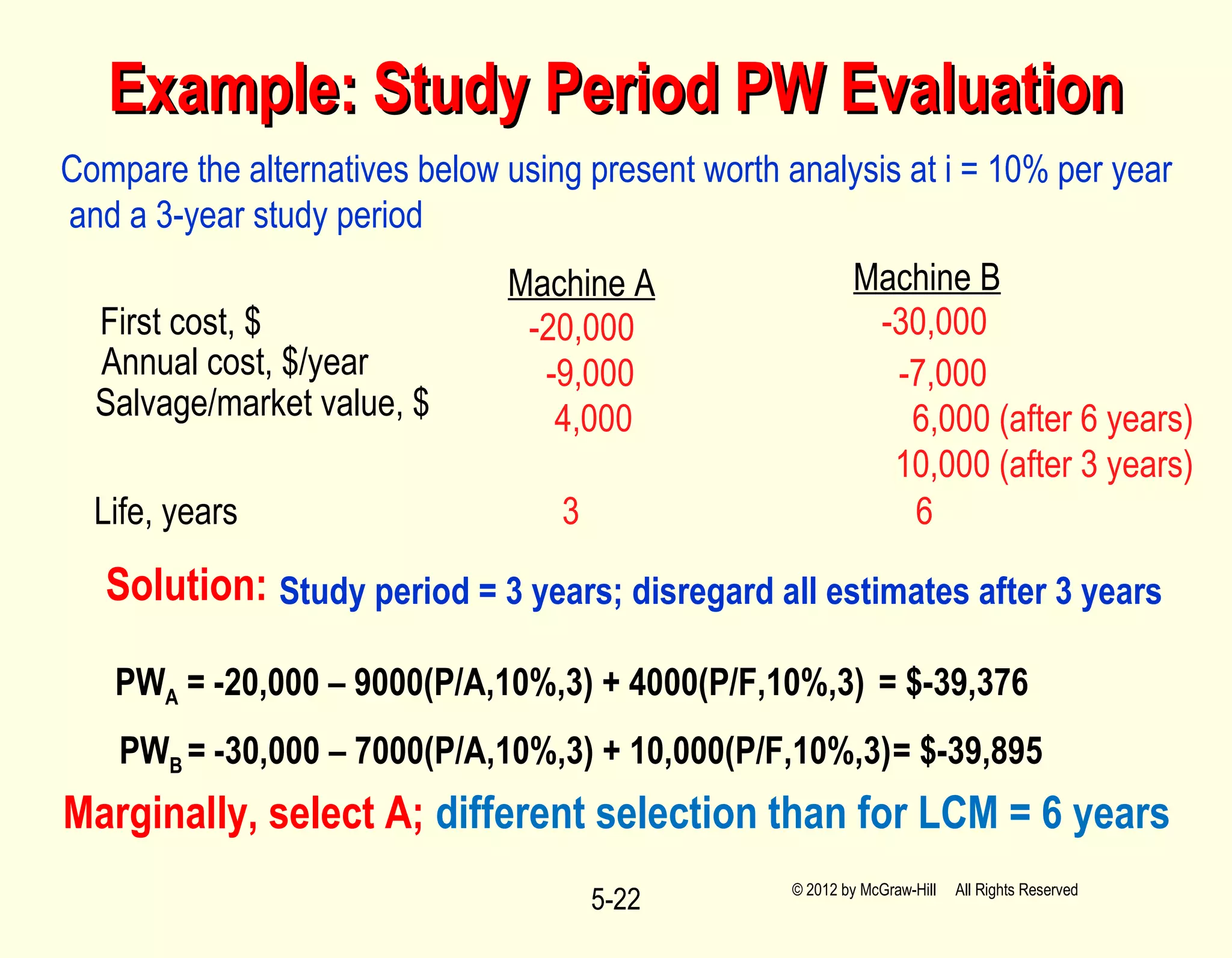

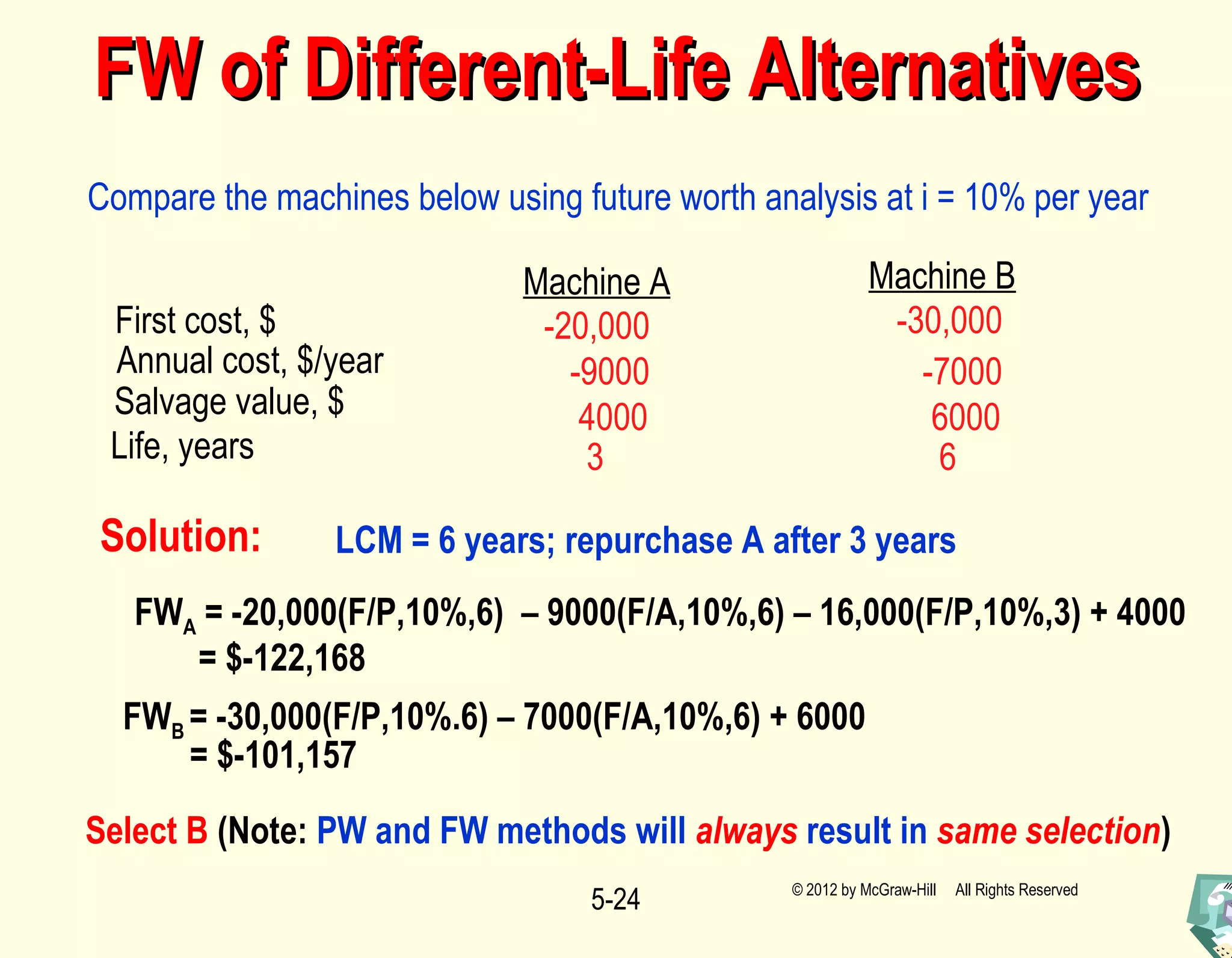

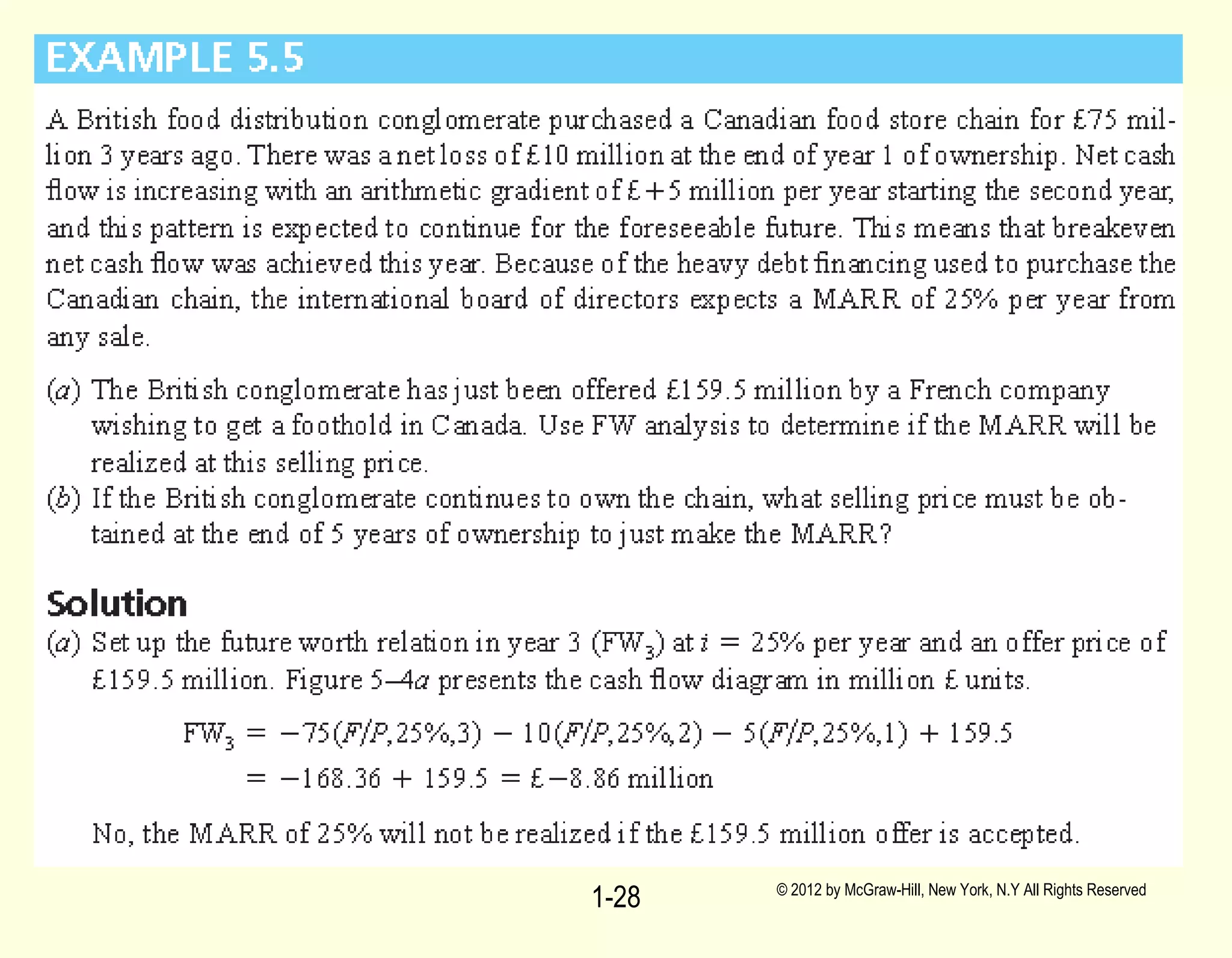

3. The examples demonstrate how to use these present worth analysis methods to evaluate alternatives, convert cash flows to present worth, and select the alternative with the highest present worth value or lowest capitalized cost.

![Engineering Economics: Solved exam problems [ch1-ch4]](https://cdn.slidesharecdn.com/ss_thumbnails/solvedexamproblemsch1-ch4-200220070043-thumbnail.jpg?width=640&height=640&fit=bounds)