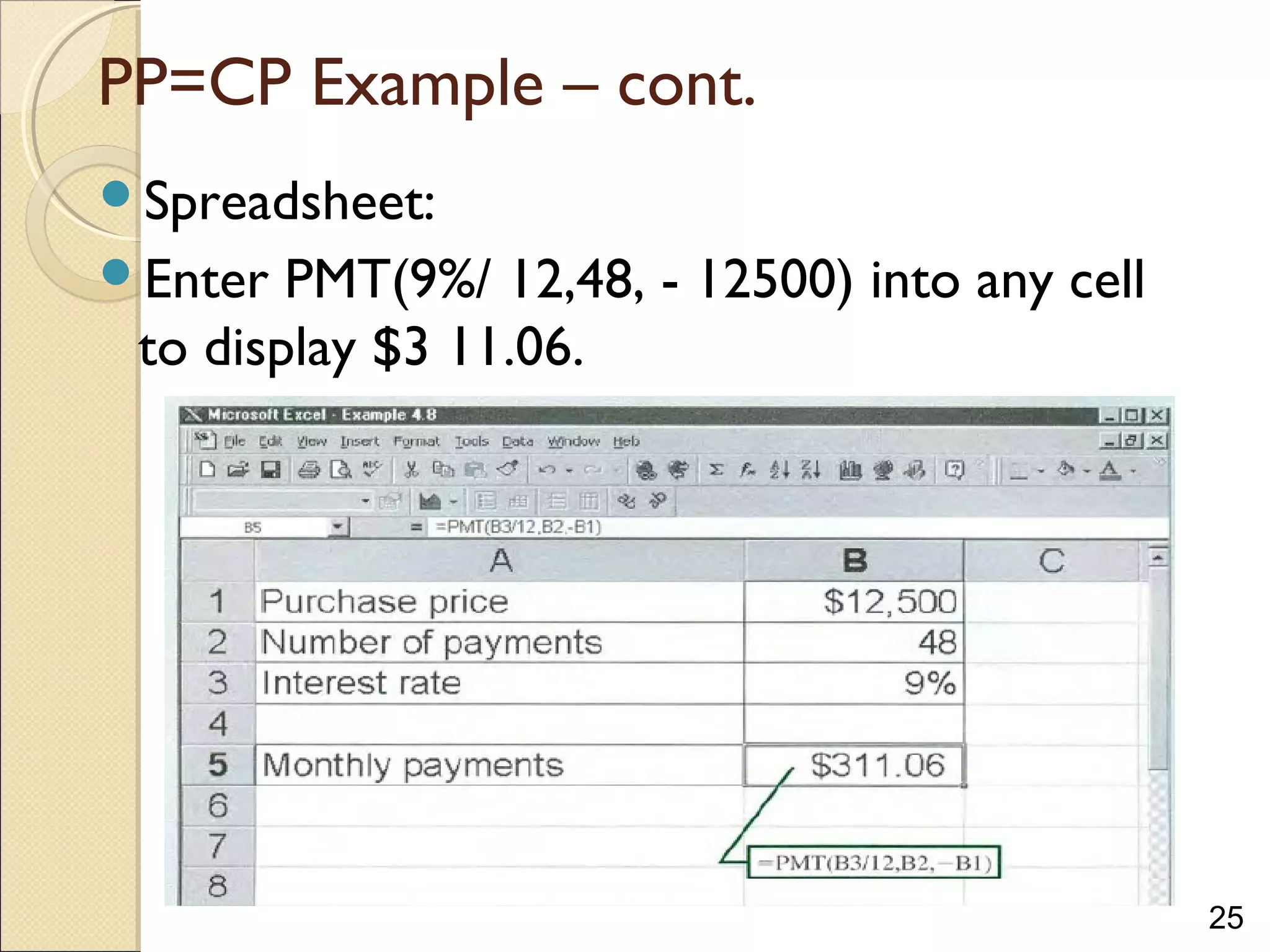

Downloaded 66 times

![10

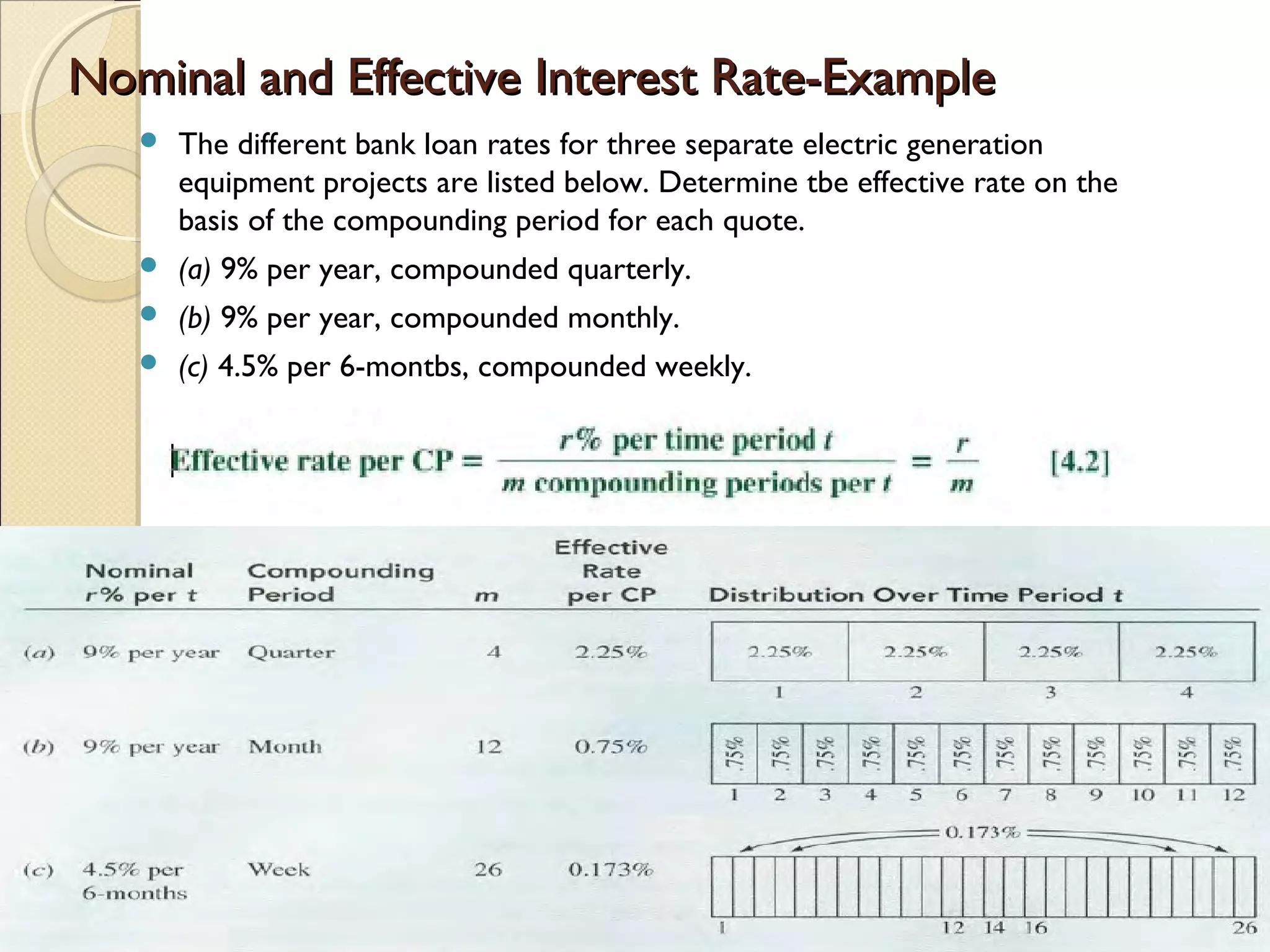

Effective interest Rates for Any PeriodEffective interest Rates for Any Period

Effective i =[1+ r/m]m

– 1

◦ i: effective interest rate per year (or certain period)

◦ m: number of compounding periods per payment period

◦ r: nominal interest rate per payment periods

it is possible to take a nominal rate (r% per

year or any other time period) and convert it

to an effective rate i for any time basis, the

most common of which will be the PP time

period.

08/07/14 10](https://image.slidesharecdn.com/ch4nomeffectiveirrev2-140807162427-phpapp01/75/Ch4-nom-effective-ir_rev2-10-2048.jpg)

![12

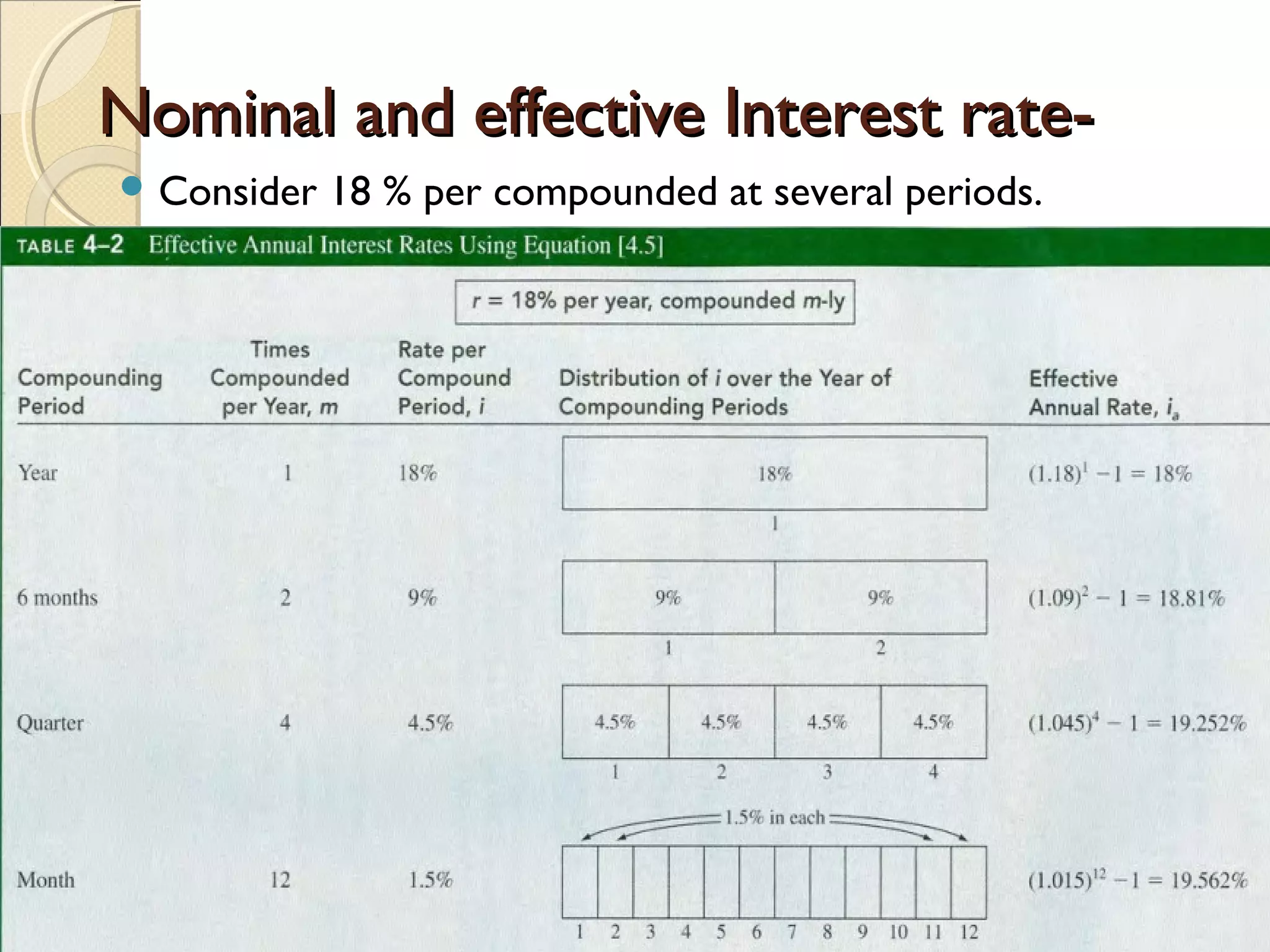

ExamplesExamples

1) Nominal rate of 18% compounded yearly

with time interval of one year (m=1)

i=[1+0.18/1]1

– 1=18% per year

2) Nominal rate of 18% compounded semi-

annual with a time interval of one year

i=[1+0.18/2]2

– 1= 18.81% per year

3) Nominal rate of 18% compounded quarterly

with a time interval of 1 year i=[1+0.18/4]4

-1= 19.252% per 1 year

08/07/14 12](https://image.slidesharecdn.com/ch4nomeffectiveirrev2-140807162427-phpapp01/75/Ch4-nom-effective-ir_rev2-12-2048.jpg)

![16

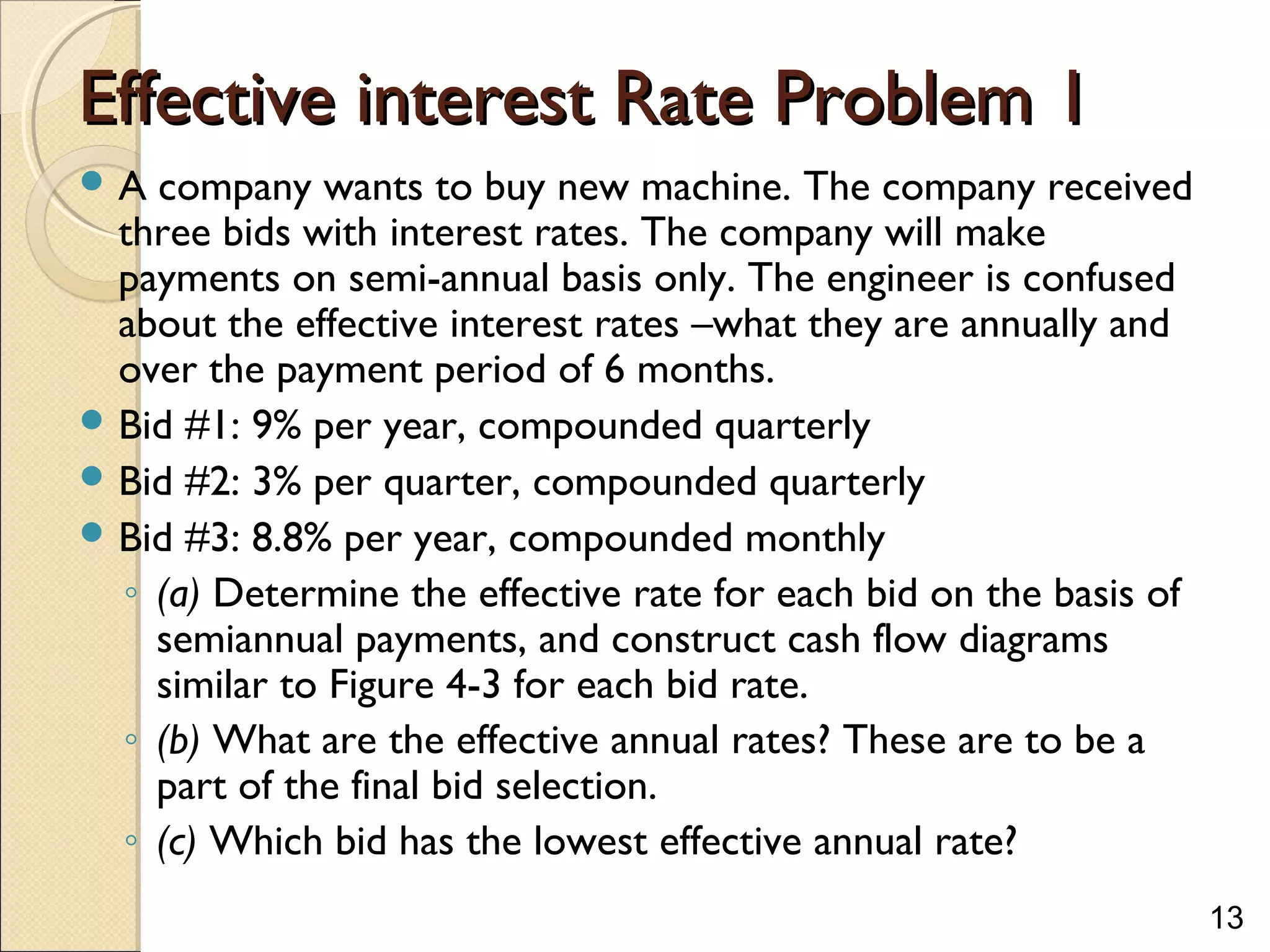

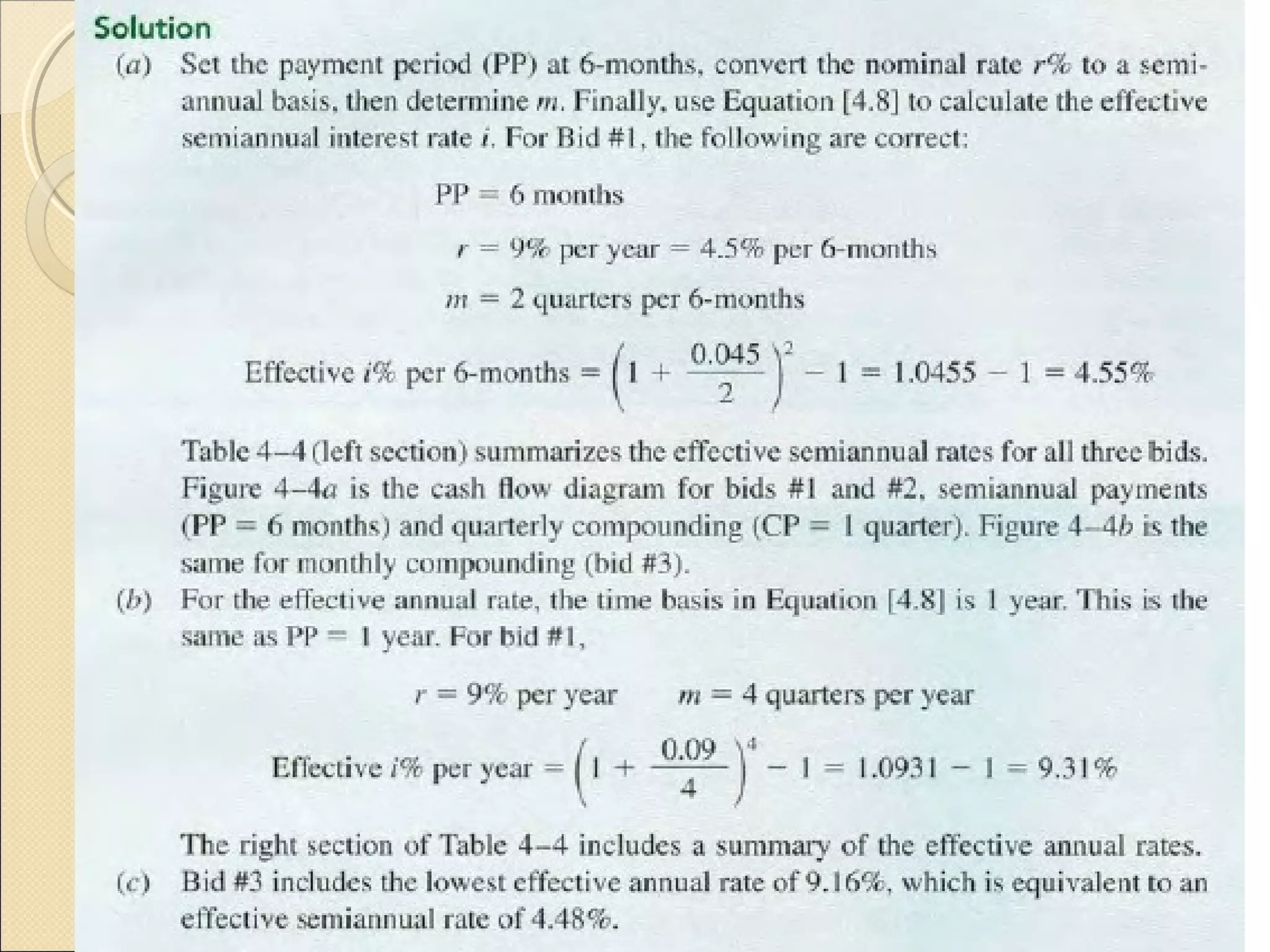

Effective Interest Rate Problem 2Effective Interest Rate Problem 2

The interest rate on a credit card is 1% per month. Calculate

the effective annual interest rate and use the interest factor

tables to find the corresponding P/F factor for n=8years?

1) 1% is an effective interest rate (Not nominal!!!!)

Nominal rate = 0.01per month*12months/year

= 0.12

i=[1+0.12/12]12

-1= 0.1268 = 12.68%

2) P/F = 1/ [1+0.1268]8

= 0.3848

3) by interpolation:

◦ 12% 0.4039

◦ 12.68% P/F

◦ 14% 0.3506

(P/F, 12.68%, 8) = 0.4039-0.0181= 0.3858

08/07/14 16](https://image.slidesharecdn.com/ch4nomeffectiveirrev2-140807162427-phpapp01/75/Ch4-nom-effective-ir_rev2-16-2048.jpg)

![23

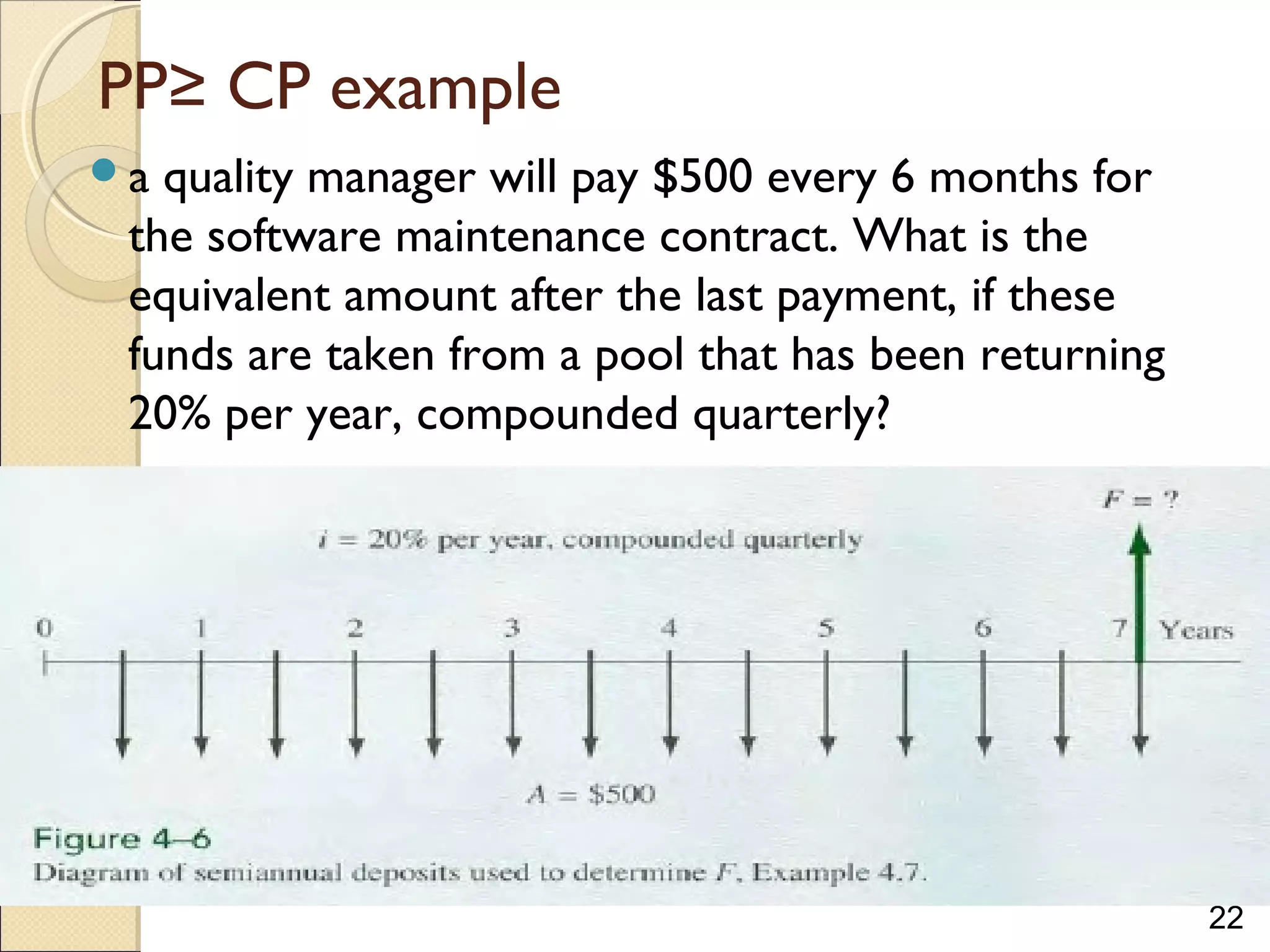

PP≥ CP example –cont.

PP= 6 months, CP is quarterly = 3 months, so PP > CP.

based on PP (every 6 months), r=20% per year is converted to

semi-annual, r = 0.20/2=0.10,

m based on r = 6/3=2

Use Equation (4.8) with r = 0.10 per 6-month period and 2 CP

periods per semiannual period.

Effective i semi-annual =[1+ r/m]m

– 1= [1+0.10/2]2

-1=10.25%

Total number of semi-annual payments = 7 yrs*2 = 14

F=A(F/A,10.25%,14)= 500(28,4891)=14,244.50](https://image.slidesharecdn.com/ch4nomeffectiveirrev2-140807162427-phpapp01/75/Ch4-nom-effective-ir_rev2-23-2048.jpg)

This document discusses nominal and effective interest rates, including continuous compounding. It defines nominal and effective interest rates, and how to calculate effective rates for different compounding periods. It provides examples of calculating effective rates for annual, semi-annual, quarterly, and continuous compounding. It also discusses how to handle calculations when the payment period is equal to, longer than, or shorter than the compounding period. This includes using the appropriate effective rate and number of periods in calculations.

Introduction to nominal and effective interest rates, continuous compounding, and equivalence calculations.

Differences between nominal and effective interest rates; importance of effective rates for compounding frequency.

Definitions of time period, compounding period, and how to calculate effective interest for different compounding scenarios.

Calculating effective interest rates for different compounding scenarios with examples and formulas.

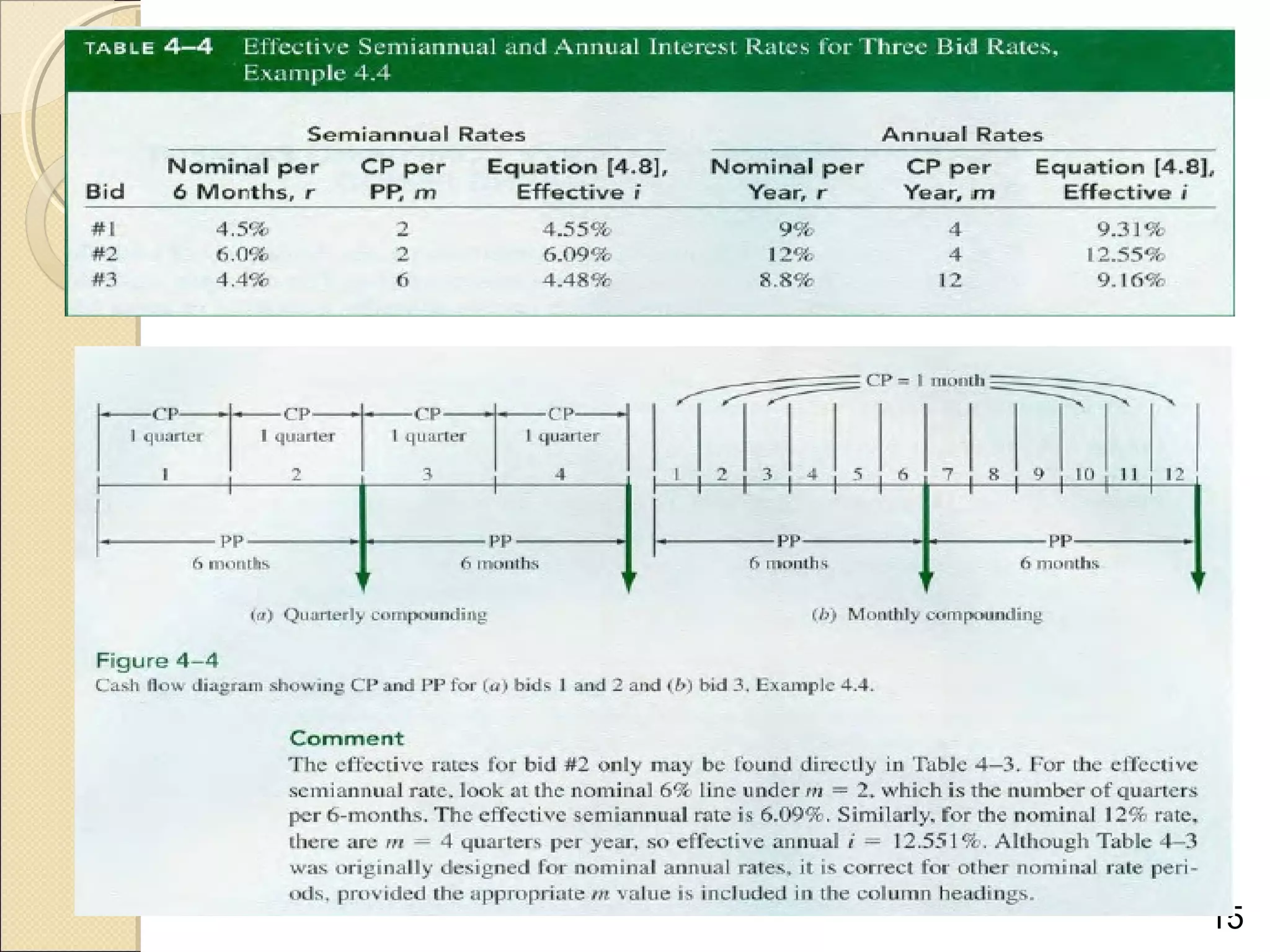

Examples of determining effective rates for bids and credit cards with explanations of cash flow diagrams.

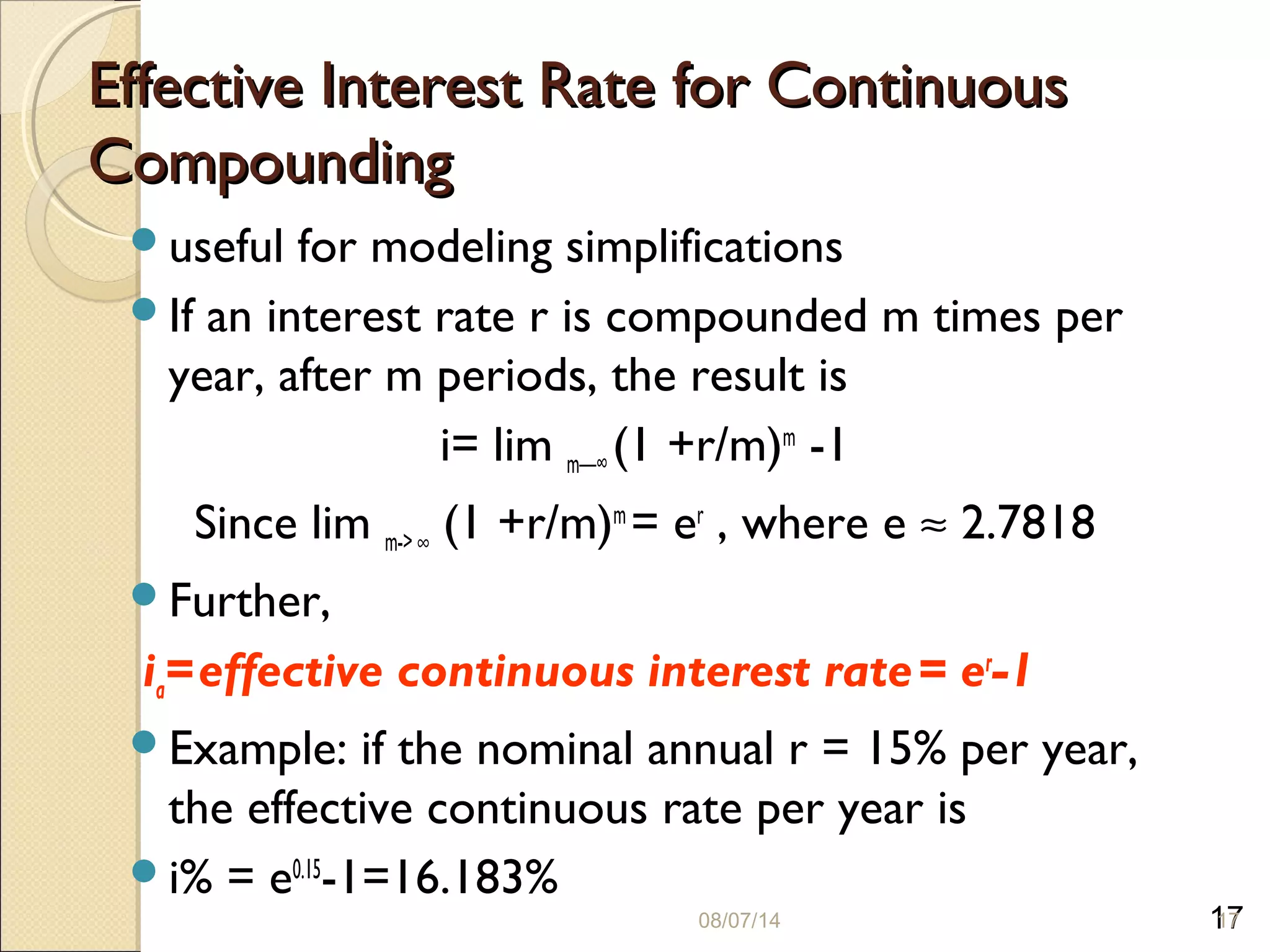

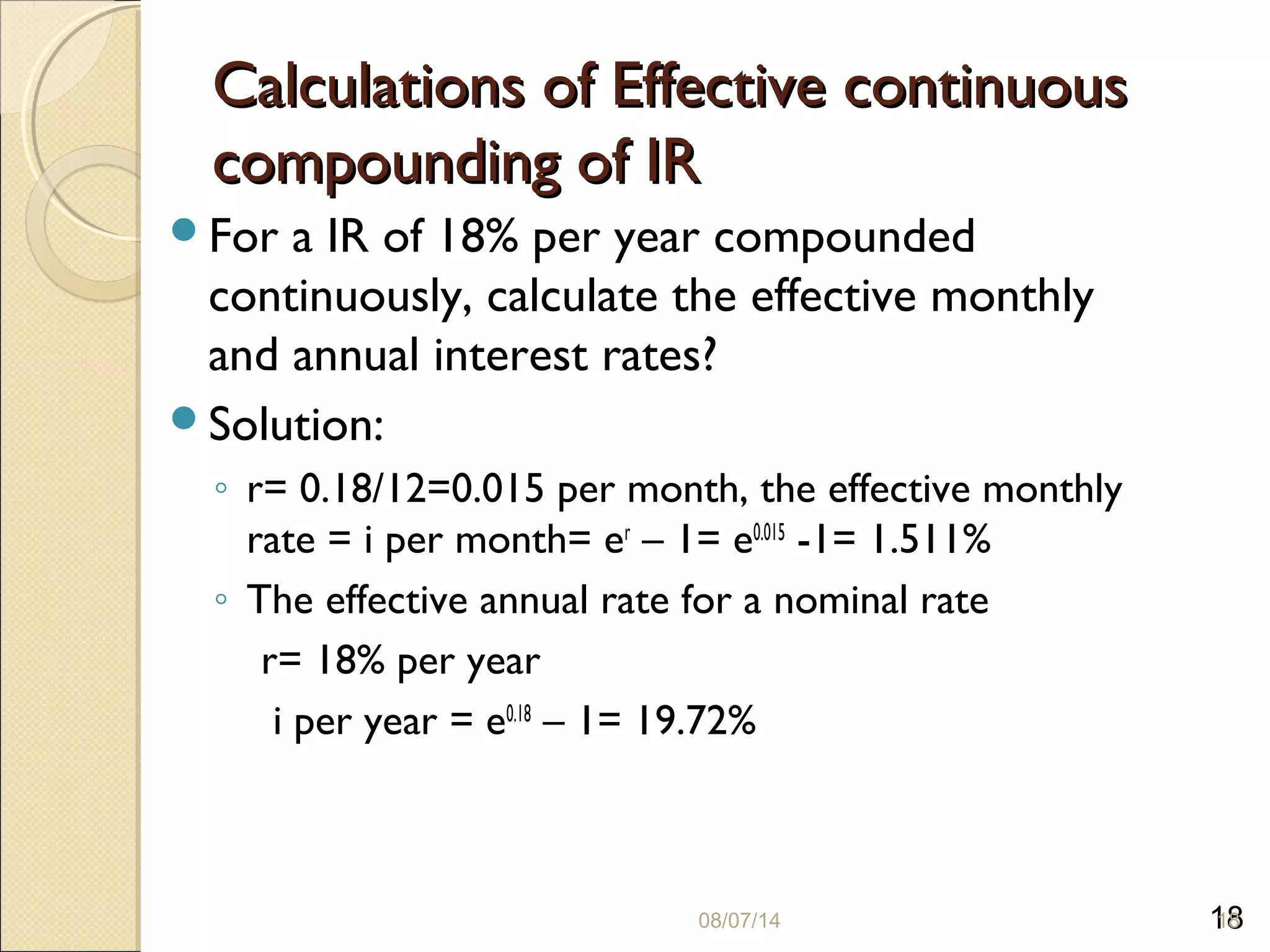

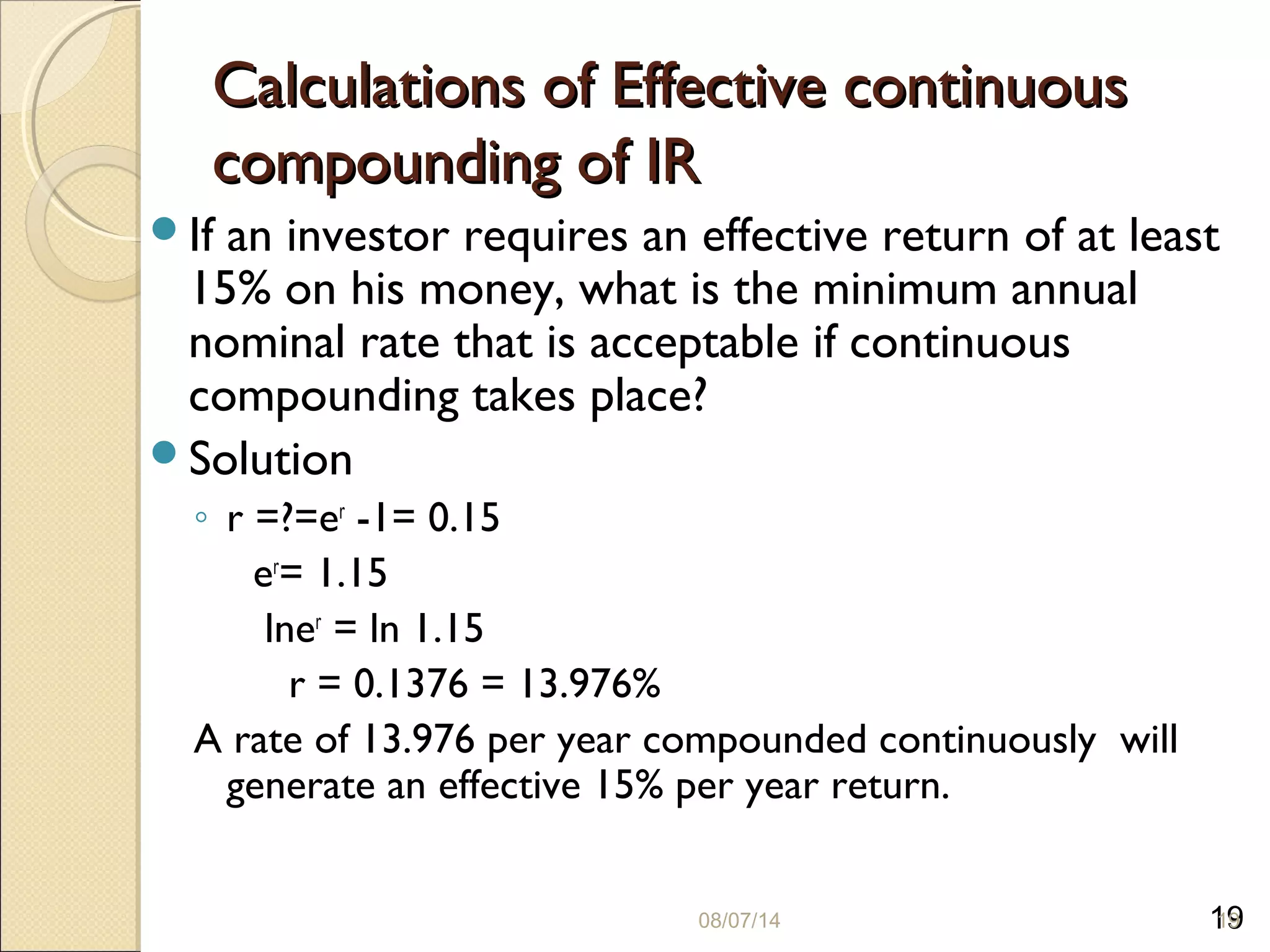

Understanding continuous compounding and calculating effective interest rates using limits and examples.

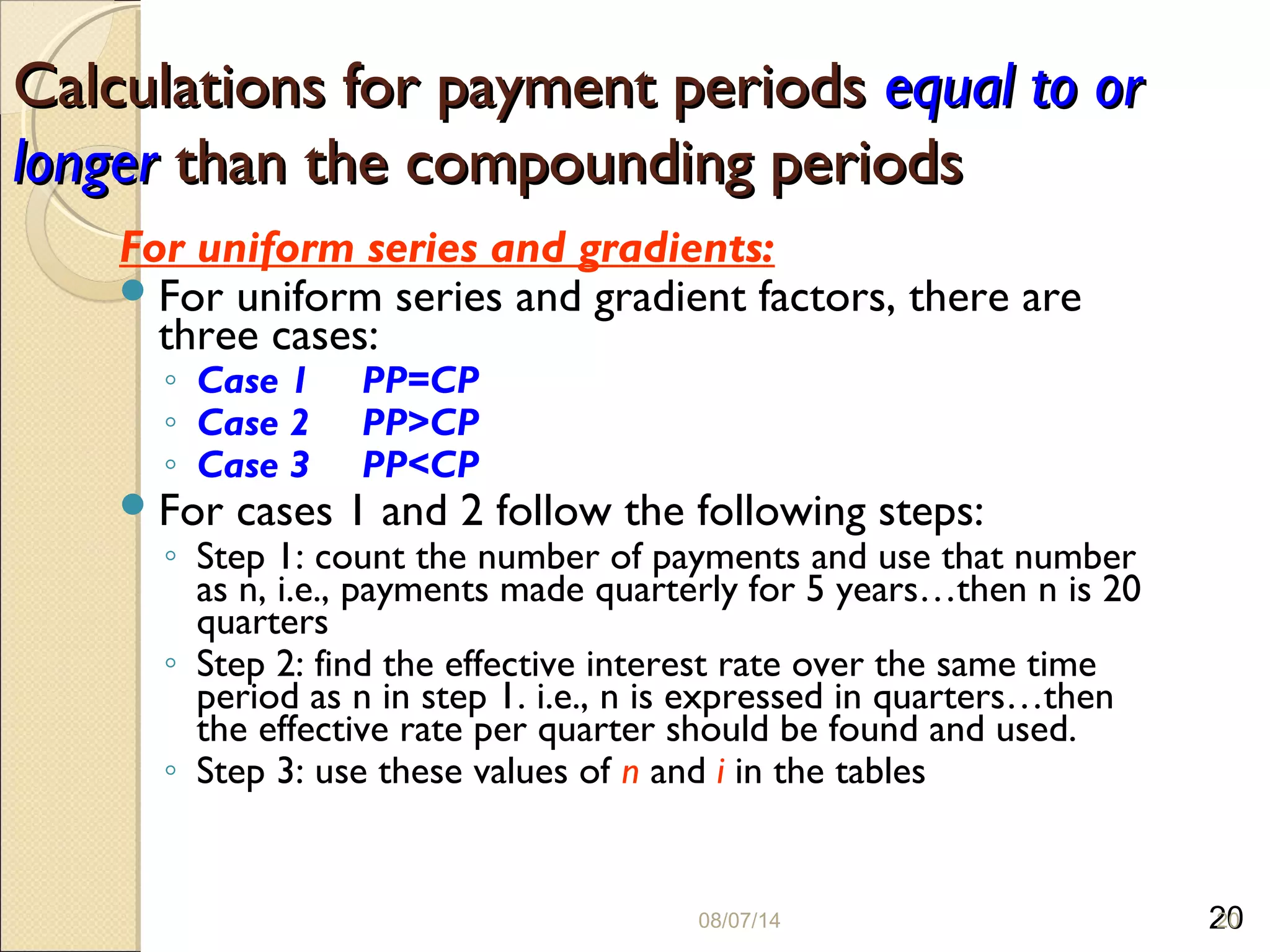

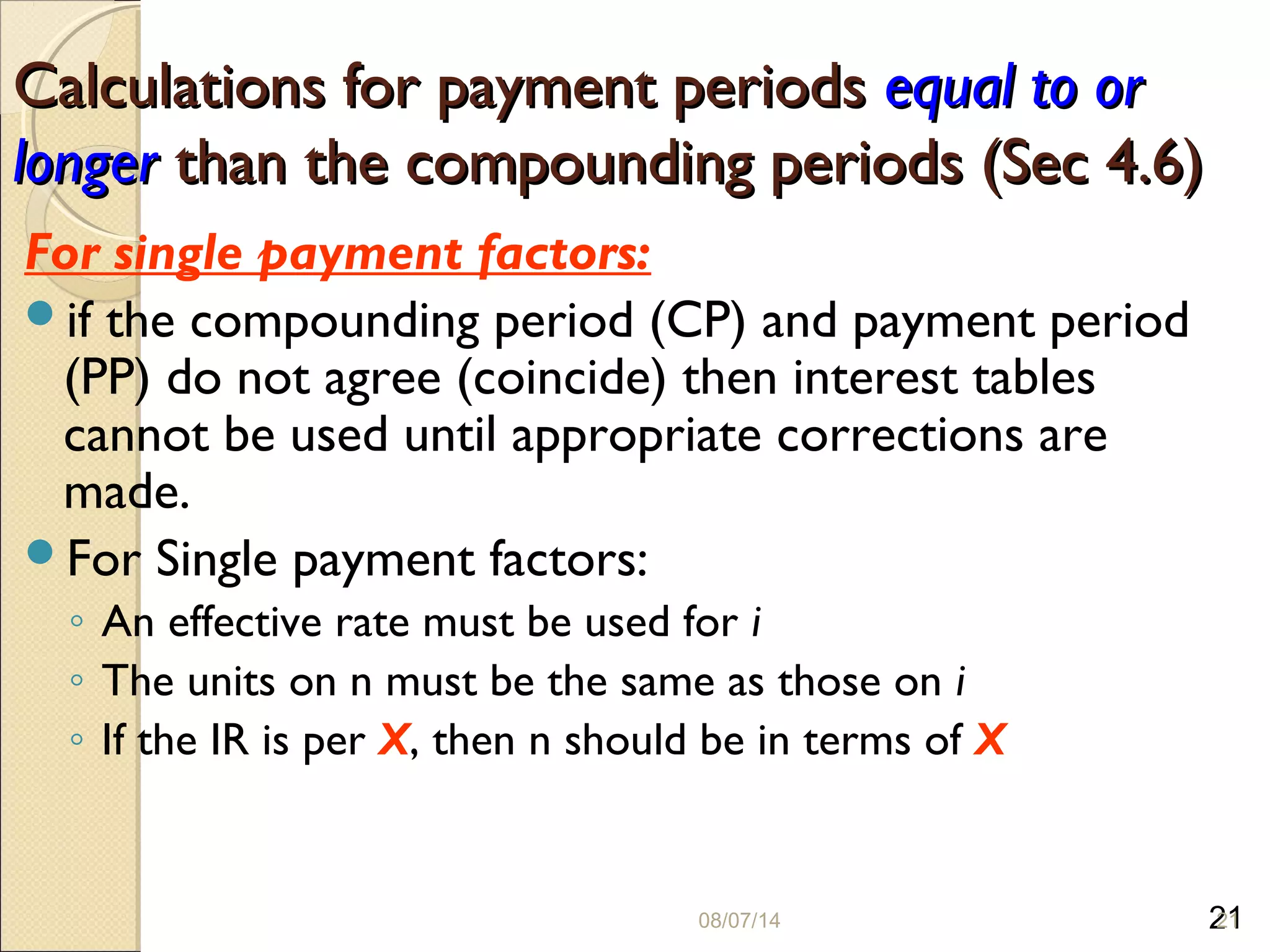

Calculating effective interest and payment periods especially when payment is longer than compounding.

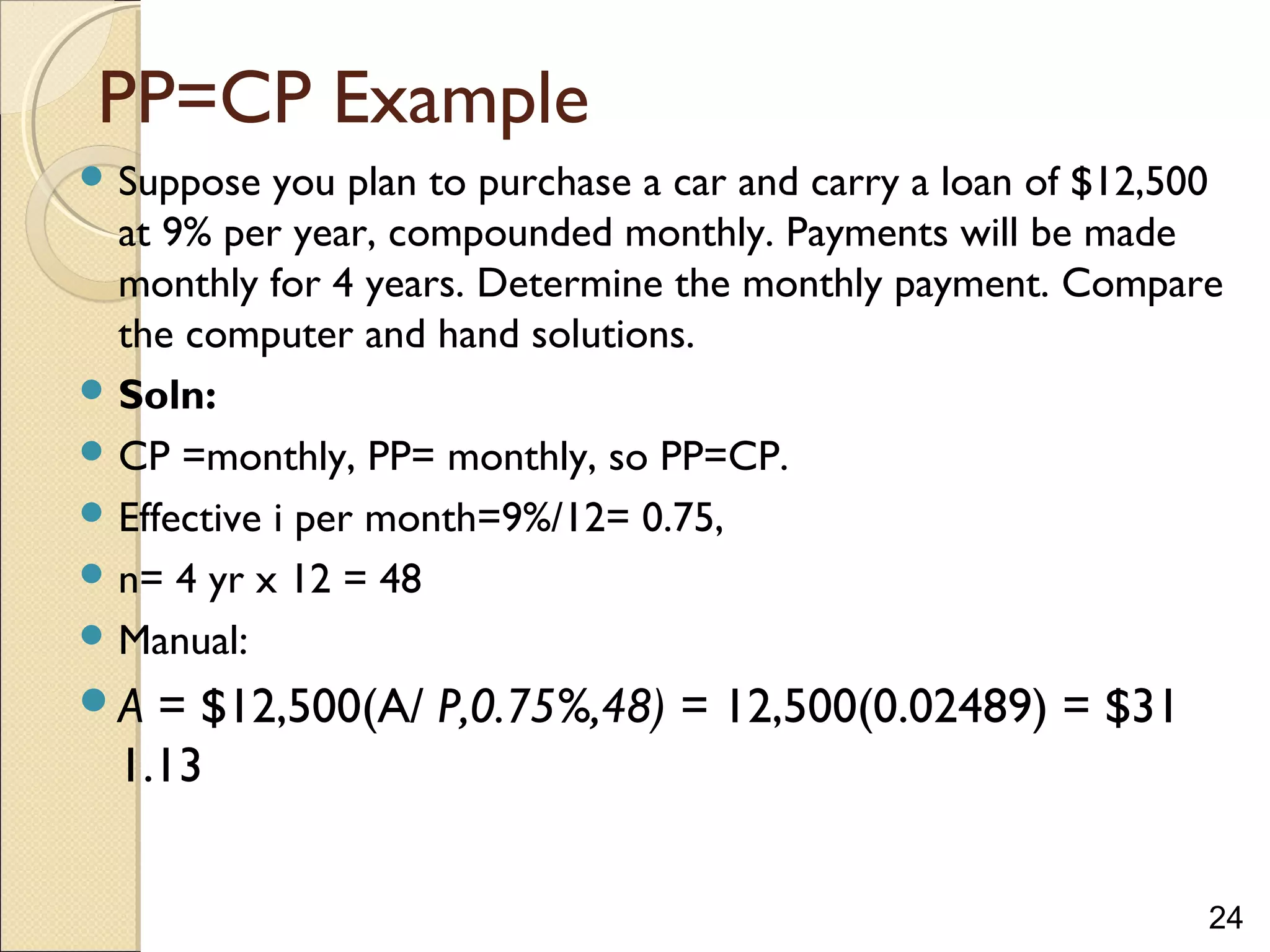

Determining payments and comparing solutions when payment period matches compounding period.

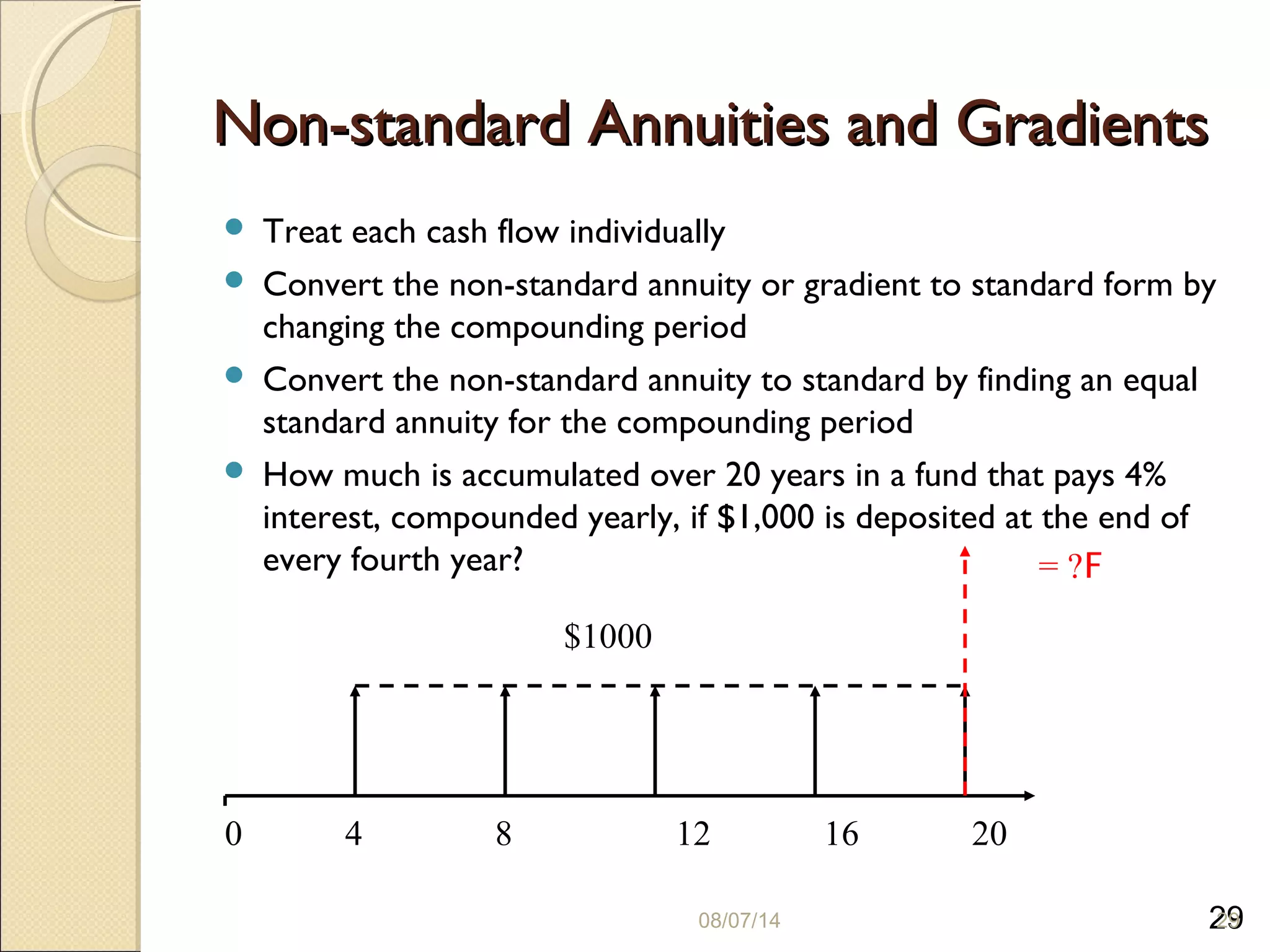

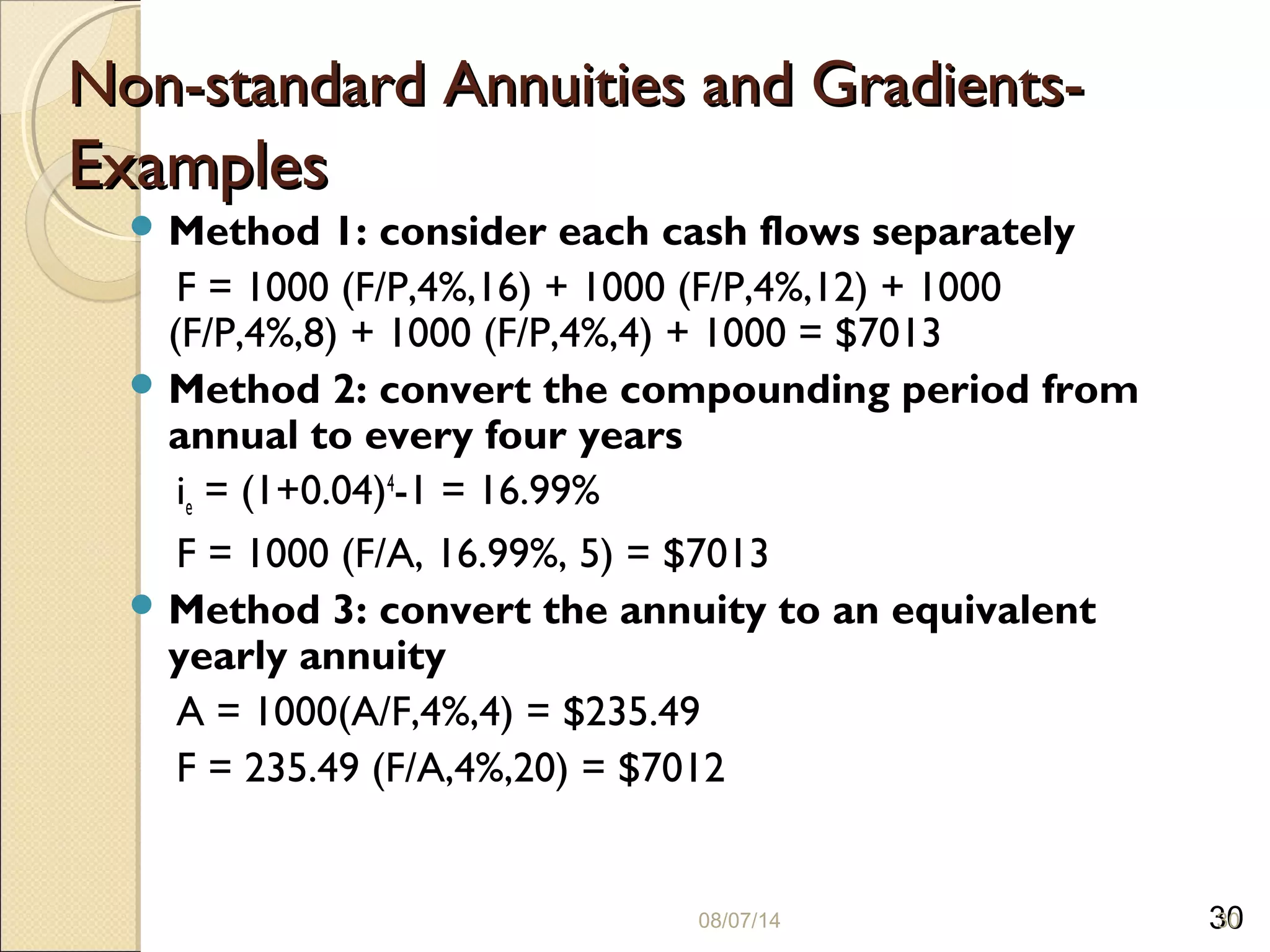

Scenarios where payment is shorter than compounding; comparisons and calculations.Approaches to evaluate non-standard annuities and gradients to standard forms with methods.