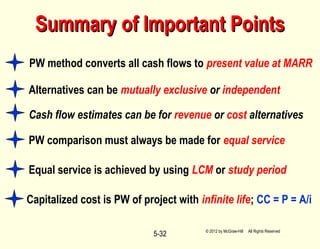

The document discusses various techniques for economic analysis of alternatives using present worth analysis:

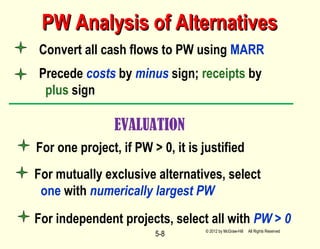

1. Present worth analysis requires converting all cash flows to their present value using the minimum attractive rate of return. Costs are assigned a negative sign and revenues a positive sign.

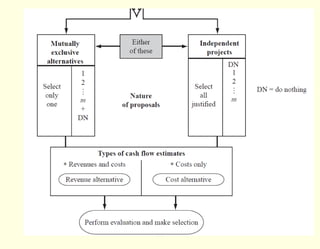

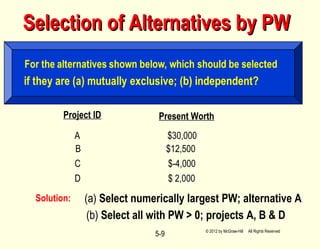

2. For mutually exclusive alternatives, the alternative with the highest positive present worth is selected. For independent projects, all alternatives with a positive present worth are selected.

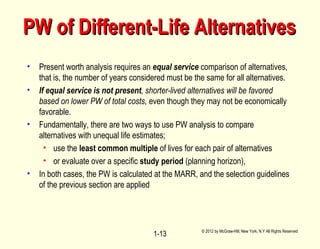

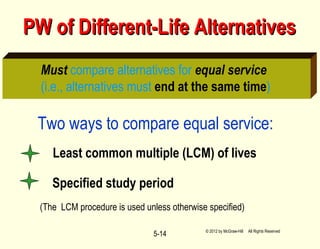

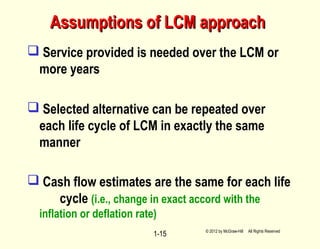

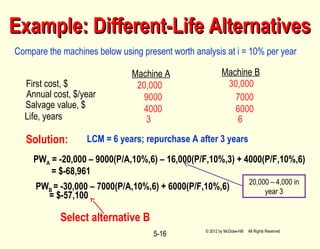

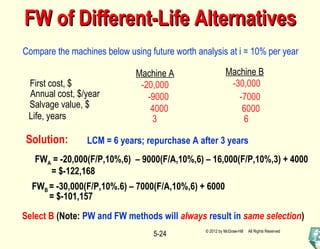

3. When alternatives have unequal lives, they must be compared over an equal period of time using either the least common multiple of lives or a specified study period.

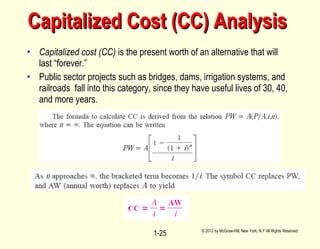

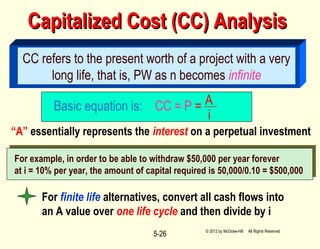

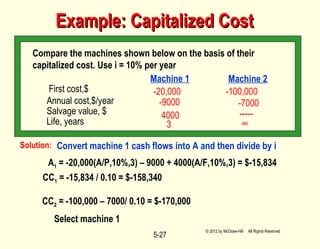

4. Capitalized cost analysis is used to evaluate alternatives that have an extremely long useful life and is calculated as the annual

![Engineering Economics: Solved exam problems [ch1-ch4]](https://cdn.slidesharecdn.com/ss_thumbnails/solvedexamproblemsch1-ch4-200220070043-thumbnail.jpg?width=640&height=640&fit=bounds)