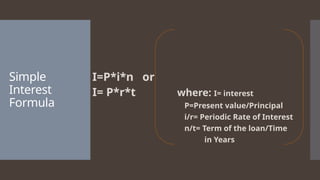

What is

Interest?

Interest isdefined as the cost of borrowing

money. It can also be the rate paid for money

on deposit, as in the case of a certificate of

deposit.

This extra amount is called the “INTEREST”

The original amount borrowed is known as the

“PRINCIPAL” or “CAPITAL” in different

situations.

The sum of both Principal and the interest is

known as “AMOUNT”

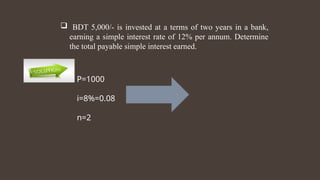

BDT 5,000/-is invested at a terms of two years in a bank,

earning a simple interest rate of 12% per annum. Determine

the total payable simple interest earned.

P=1000

i=8%=0.08

n=2

8.

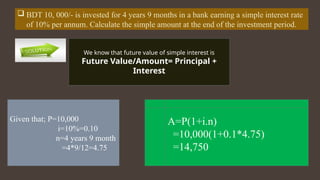

BDT 10,000/- is invested for 4 years 9 months in a bank earning a simple interest rate

of 10% per annum. Calculate the simple amount at the end of the investment period.

Given that; P=10,000

i=10%=0.10

n=4 years 9 month

=4*9/12=4.75

We know that future value of simple interest is

Future Value/Amount= Principal +

Interest

A=P(1+i.n)

=10,000(1+0.1*4.75)

=14,750

9.

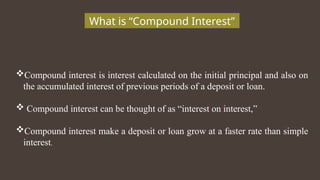

What is “CompoundInterest”

Compound interest is interest calculated on the initial principal and also on

the accumulated interest of previous periods of a deposit or loan.

Compound interest can be thought of as “interest on interest,”

Compound interest make a deposit or loan grow at a faster rate than simple

interest.

10.

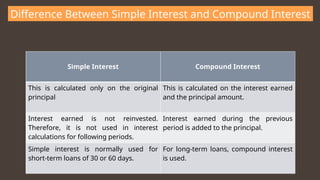

Difference Between SimpleInterest and Compound Interest

Simple Interest Compound Interest

This is calculated only on the original

principal

This is calculated on the interest earned

and the principal amount.

Interest earned is not reinvested.

Therefore, it is not used in interest

calculations for following periods.

Interest earned during the previous

period is added to the principal.

Simple interest is normally used for

short-term loans of 30 or 60 days.

For long-term loans, compound interest

is used.

11.

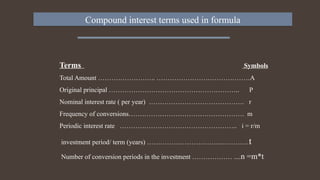

Compound interest termsused in formula

Terms Symbols

Total Amount …………………….. ……………………………………A

Original principal ………………………………………………….. P

Nominal interest rate ( per year) ……………………………………. r

Frequency of conversions……………………………………………. m

Periodic interest rate …………………………………………….. i = r/m

investment period/ term (years) …………………………….…………t

Number of conversion periods in the investment ……………… ....n =m*t

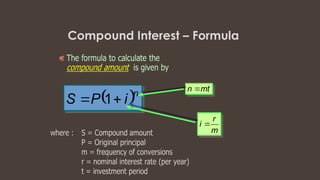

12.

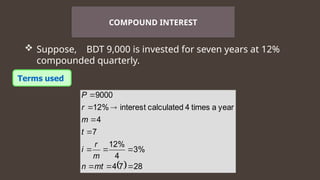

Suppose, BDT9,000 is invested for seven years at 12%

compounded quarterly.

COMPOUND INTEREST

28

7

4

%

3

4

%

12

7

4

year

a

times

4

calculated

interest

%

12

9000

mt

n

m

r

i

t

m

r

P

Suppose, BDT25,000 is invested for six years at 10%

compounded half-yearly. Find the compounded amount

and in turn, the total amount.

COMPOUND INTEREST PRACTICE

15.

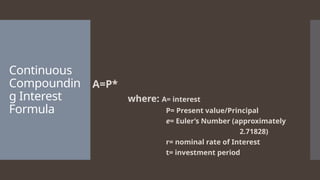

Continuous

Compoundin

g

While this isnot possible in practice, the concept of

continuously compounded interest is important in

finance. It is an extreme case of compounding, as

most interest is compounded on a monthly, quarterly,

or semiannual basis.

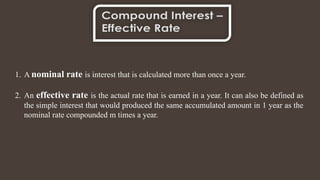

1. A nominalrate is interest that is calculated more than once a year.

2. An effective rate is the actual rate that is earned in a year. It can also be defined as

the simple interest that would produced the same accumulated amount in 1 year as the

nominal rate compounded m times a year.

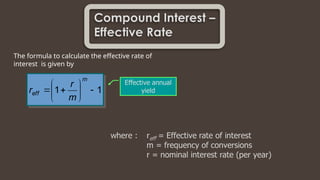

18.

The formula tocalculate the effective rate of

interest is given by

1

1

m

eff

m

r

r

19.

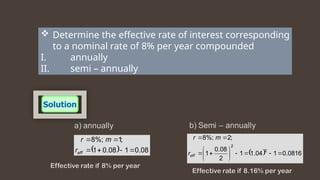

Determine theeffective rate of interest corresponding

to a nominal rate of 8% per year compounded

I. annually

II. semi – annually

08

.

0

1

08

.

0

1

;

1

%;

8

eff

r

m

r

0816

.

0

1

04

.

1

1

2

08

.

0

1

;

2

%;

8

2

2

eff

r

m

r

20.

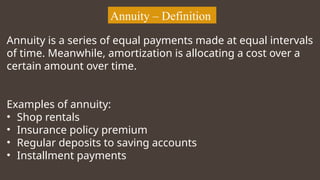

Annuity – Definition

Annuityis a series of equal payments made at equal intervals

of time. Meanwhile, amortization is allocating a cost over a

certain amount over time.

Examples of annuity:

• Shop rentals

• Insurance policy premium

• Regular deposits to saving accounts

• Installment payments

21.

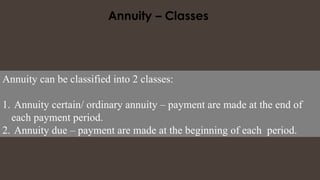

Annuity can beclassified into 2 classes:

1. Annuity certain/ ordinary annuity – payment are made at the end of

each payment period.

2. Annuity due – payment are made at the beginning of each period.

22.

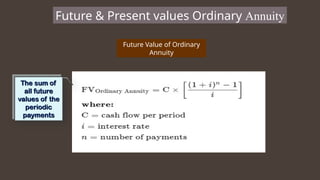

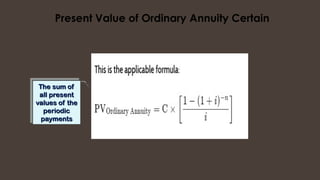

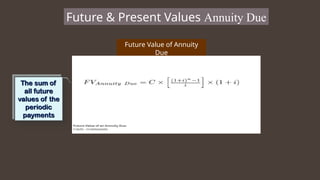

Future & Presentvalues Ordinary Annuity

Future Value of Ordinary

Annuity

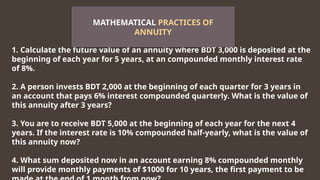

1. Calculate thefuture value of an annuity where BDT 3,000 is deposited at the

beginning of each year for 5 years, at an compounded monthly interest rate

of 8%.

2. A person invests BDT 2,000 at the beginning of each quarter for 3 years in

an account that pays 6% interest compounded quarterly. What is the value of

this annuity after 3 years?

3. You are to receive BDT 5,000 at the beginning of each year for the next 4

years. If the interest rate is 10% compounded half-yearly, what is the value of

this annuity now?

4. What sum deposited now in an account earning 8% compounded monthly

will provide monthly payments of $1000 for 10 years, the first payment to be

MATHEMATICAL PRACTICES OF

ANNUITY

27.

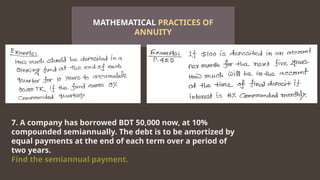

7. A companyhas borrowed BDT 50,000 now, at 10%

compounded semiannually. The debt is to be amortized by

equal payments at the end of each term over a period of

two years.

Find the semiannual payment.

MATHEMATICAL PRACTICES OF

ANNUITY