Downloaded 261 times

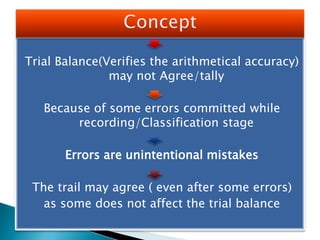

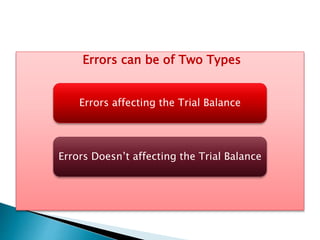

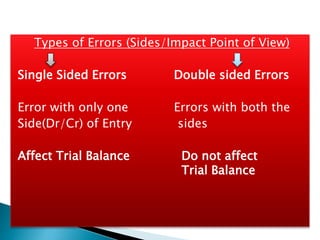

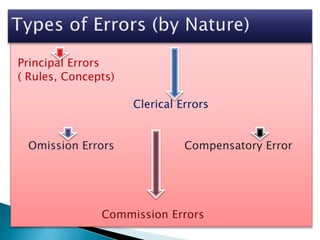

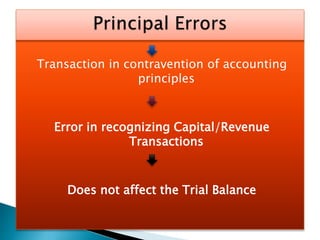

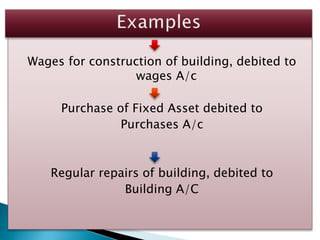

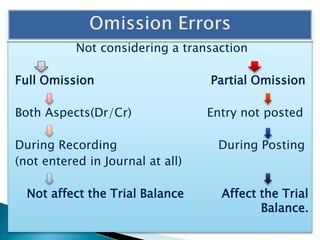

The document discusses various types of errors in accounting and their impact on the trial balance, categorizing them as errors that do and do not affect it. It details methods for rectifying these errors, depending on whether they are detected before or after the trial balance is prepared. The document further provides examples and questions related to accounting errors and their rectification processes.