Download to read offline

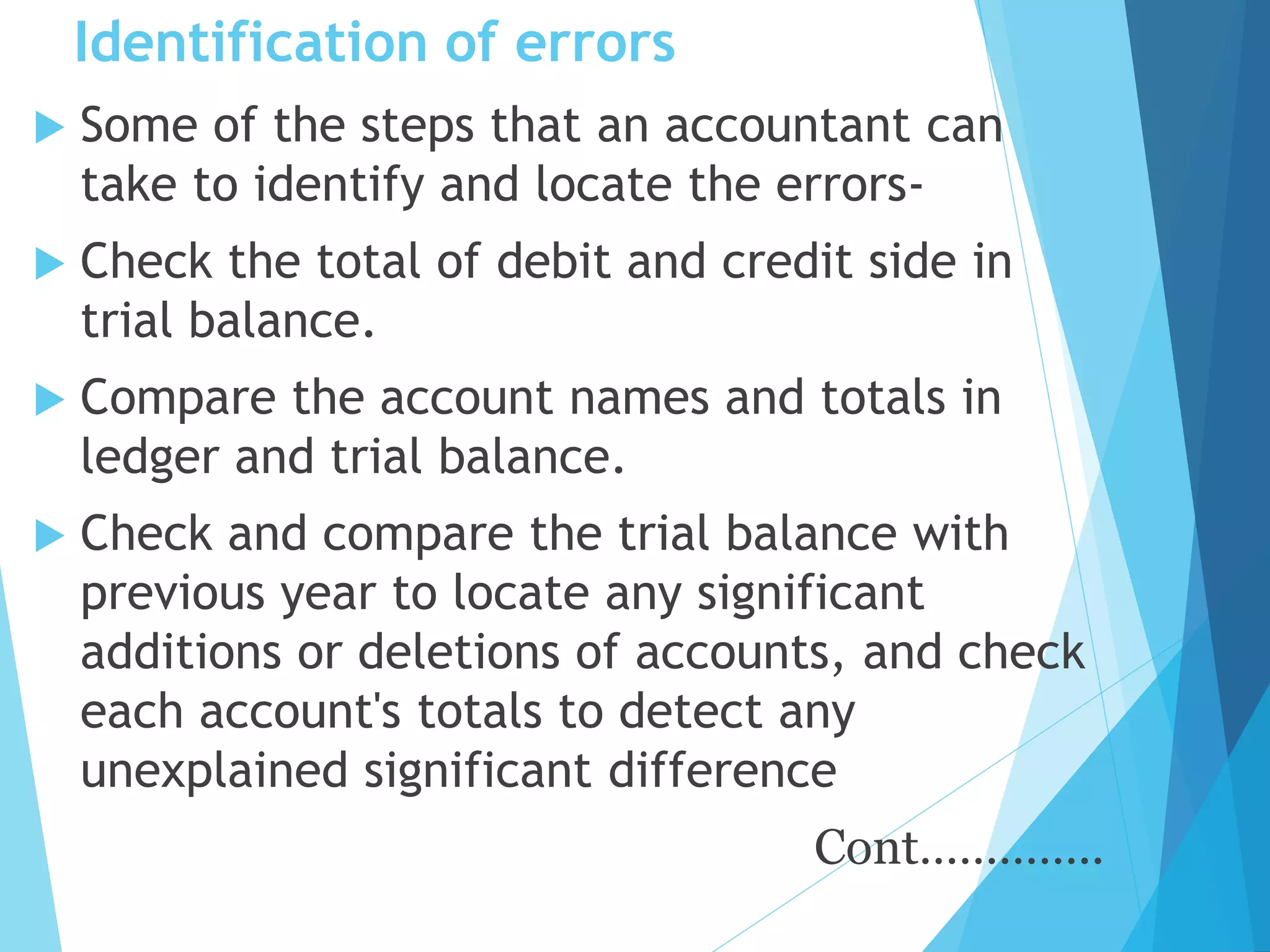

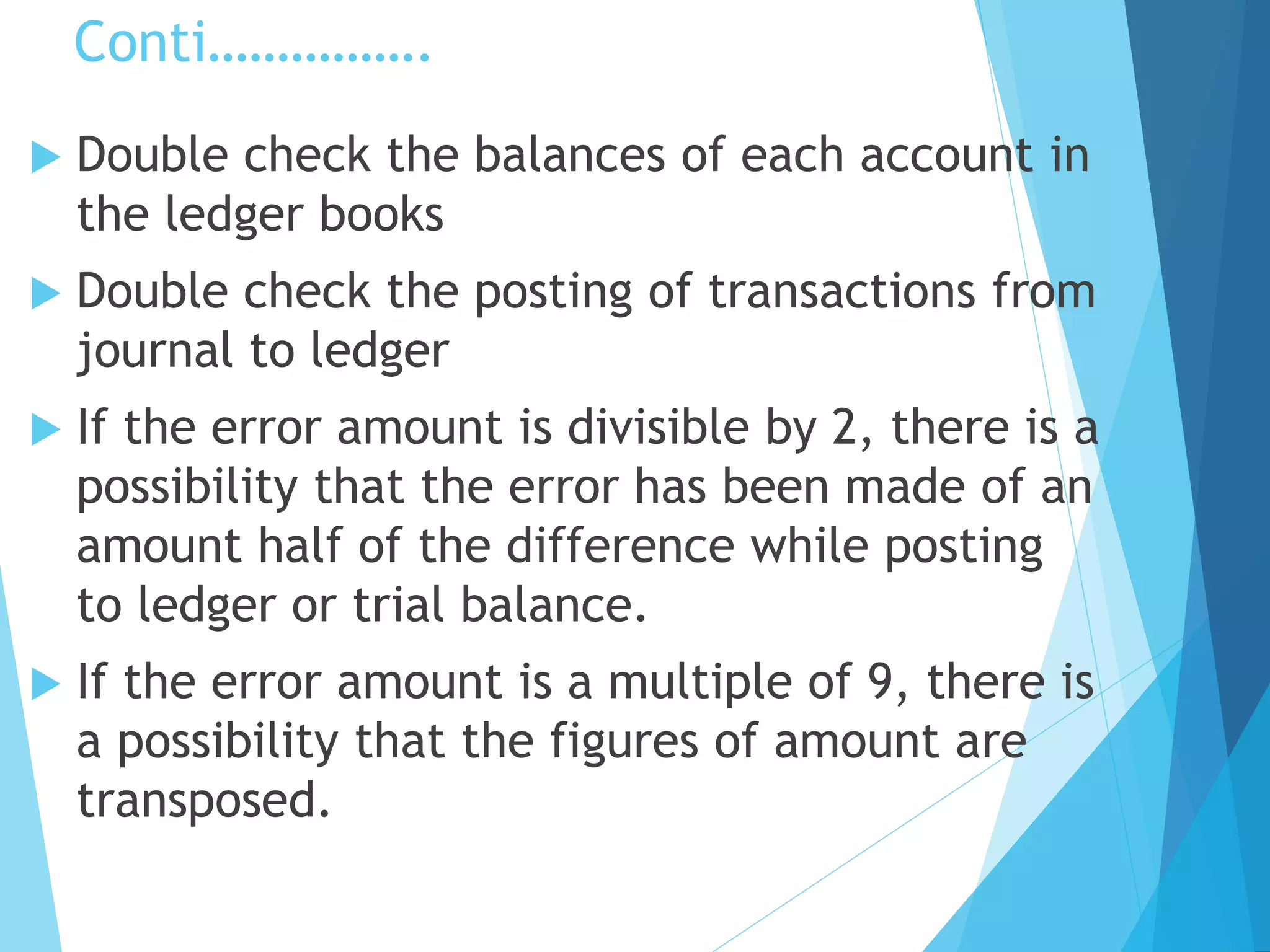

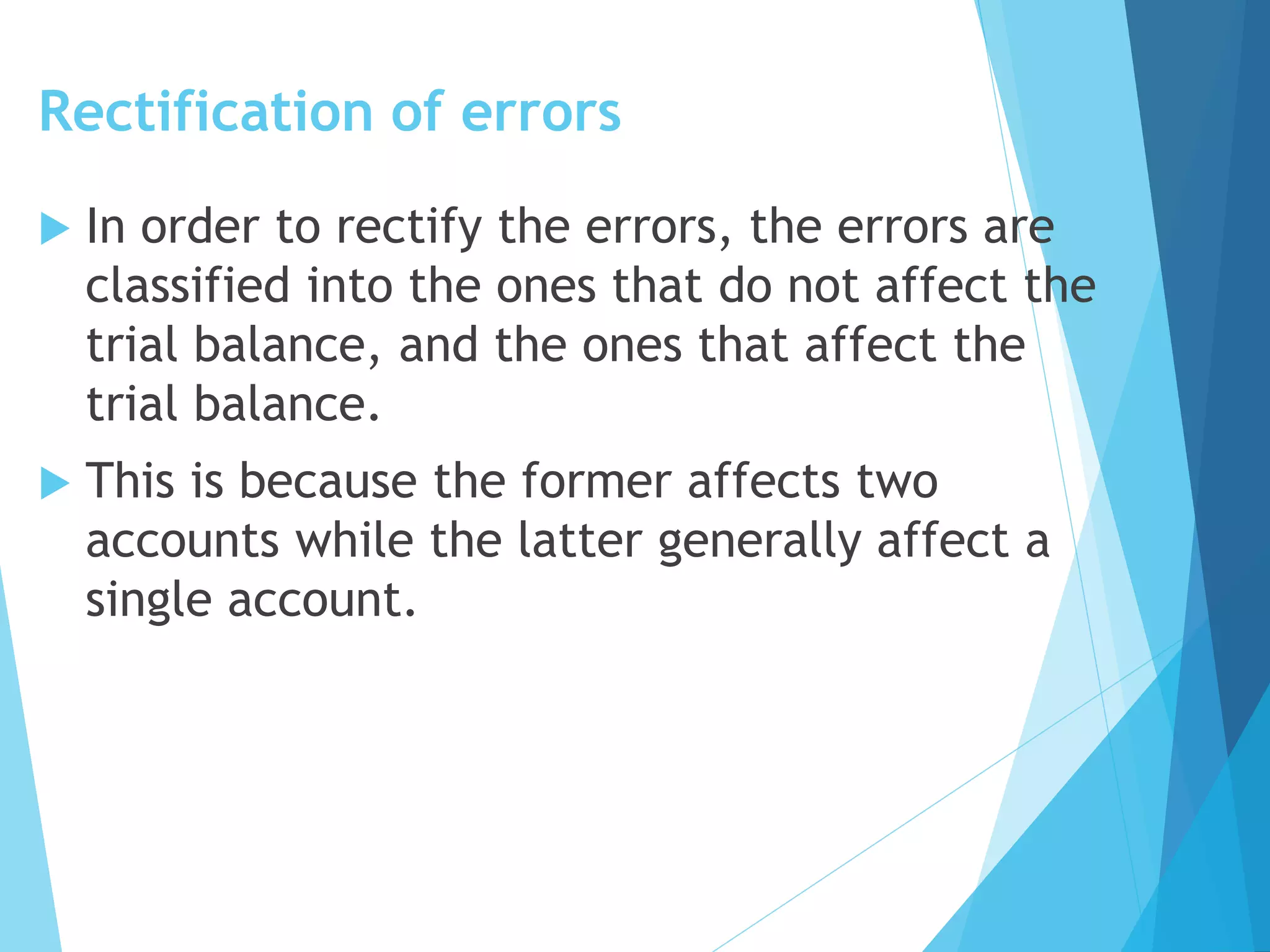

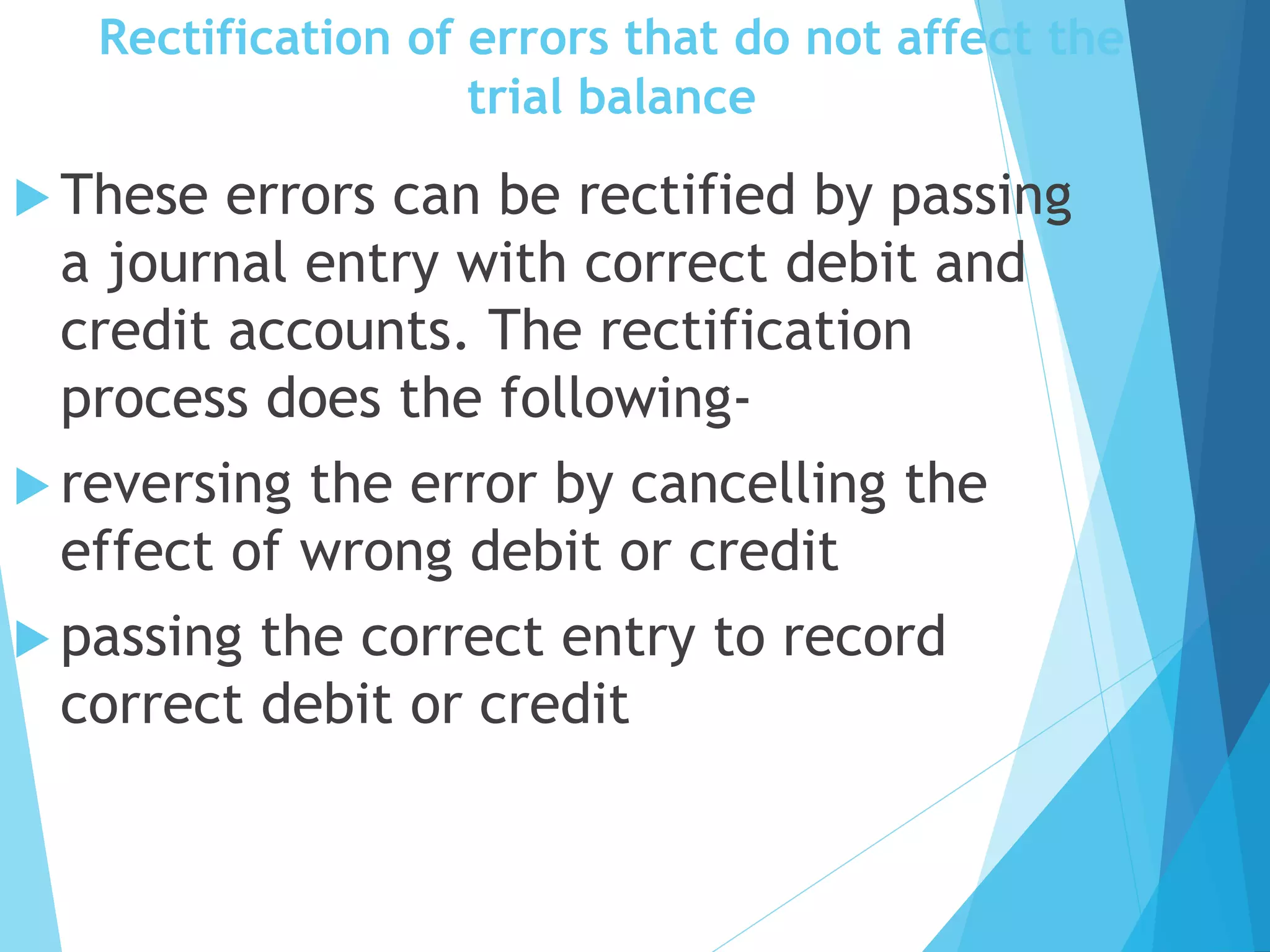

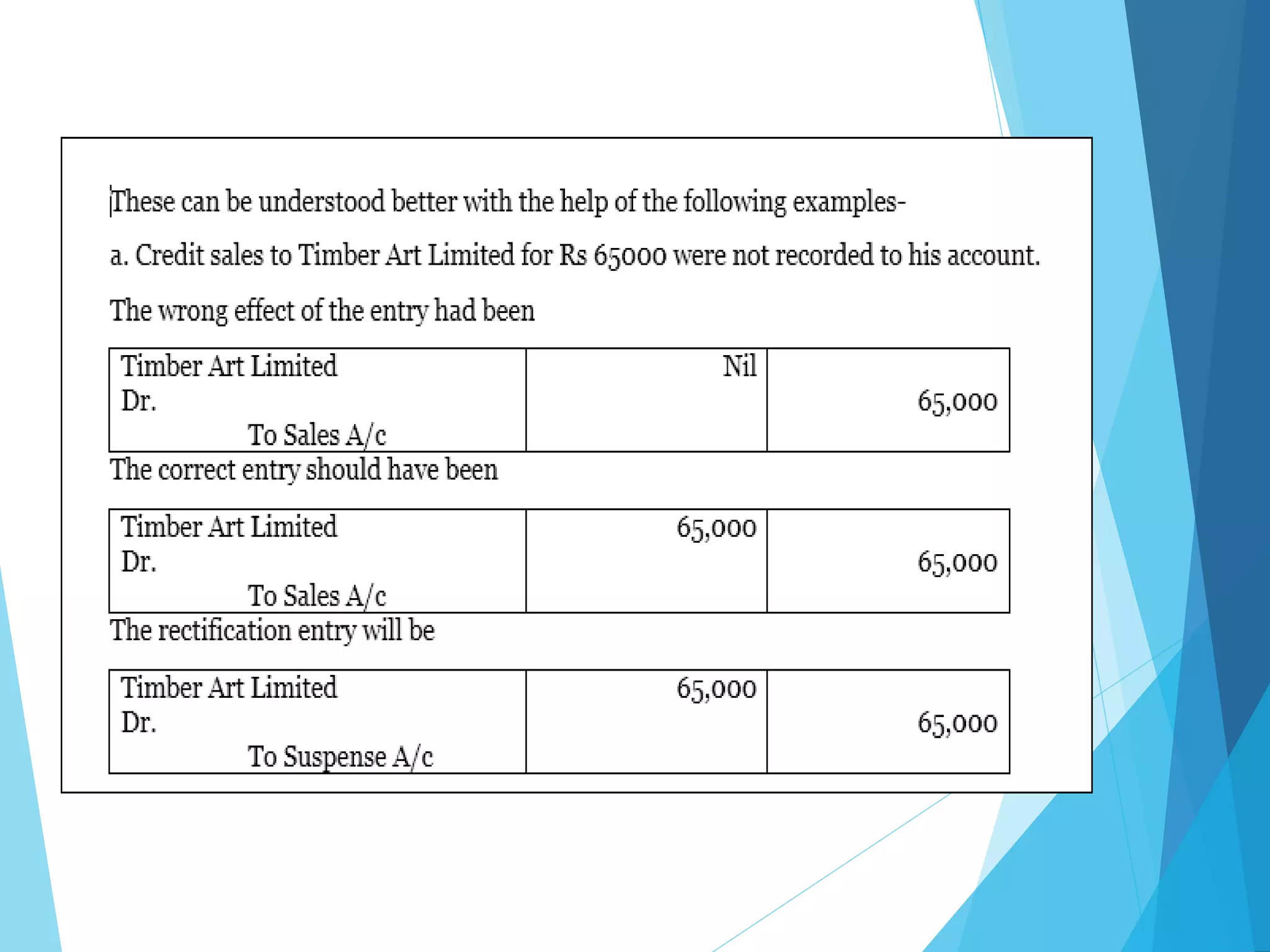

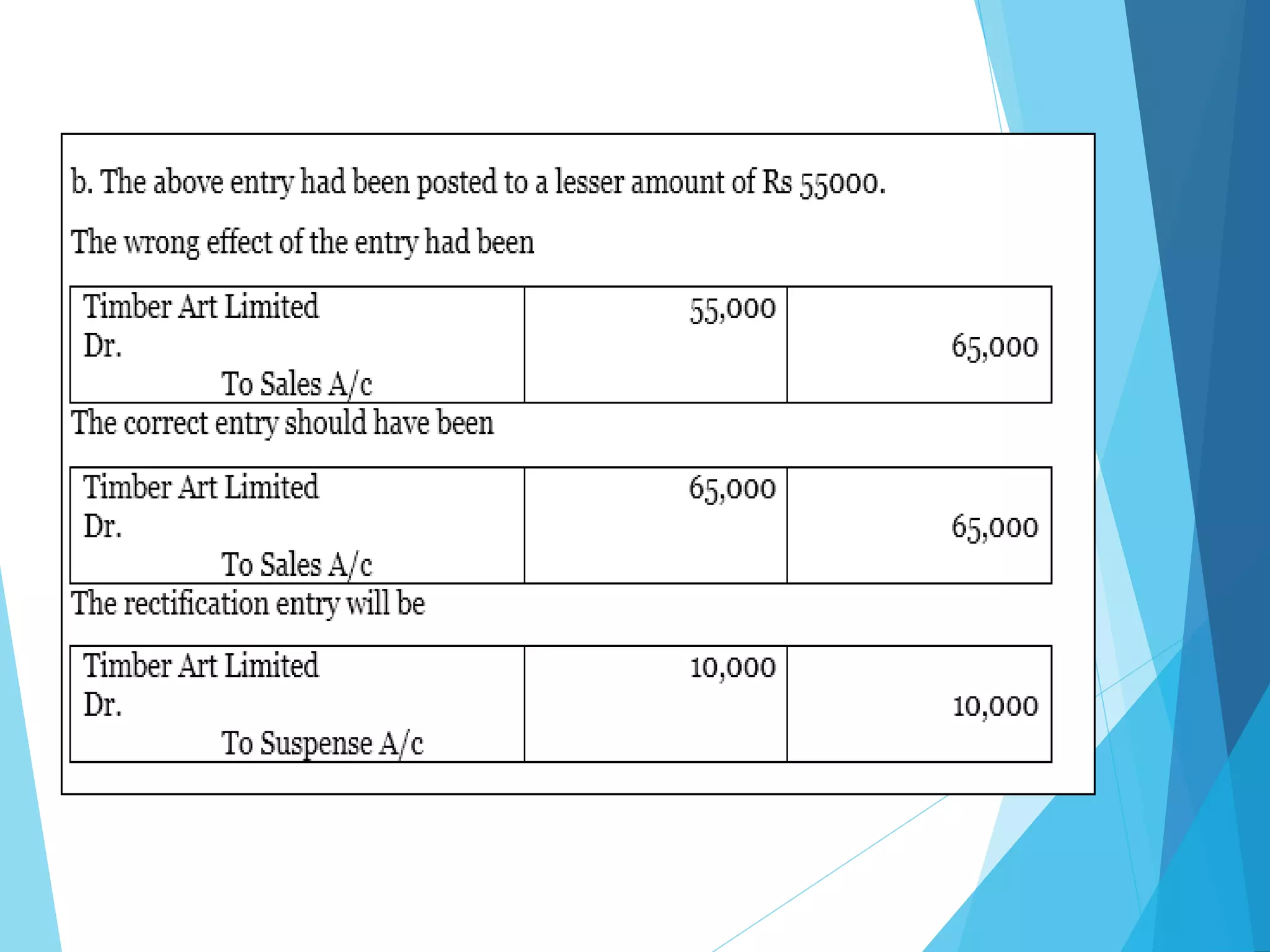

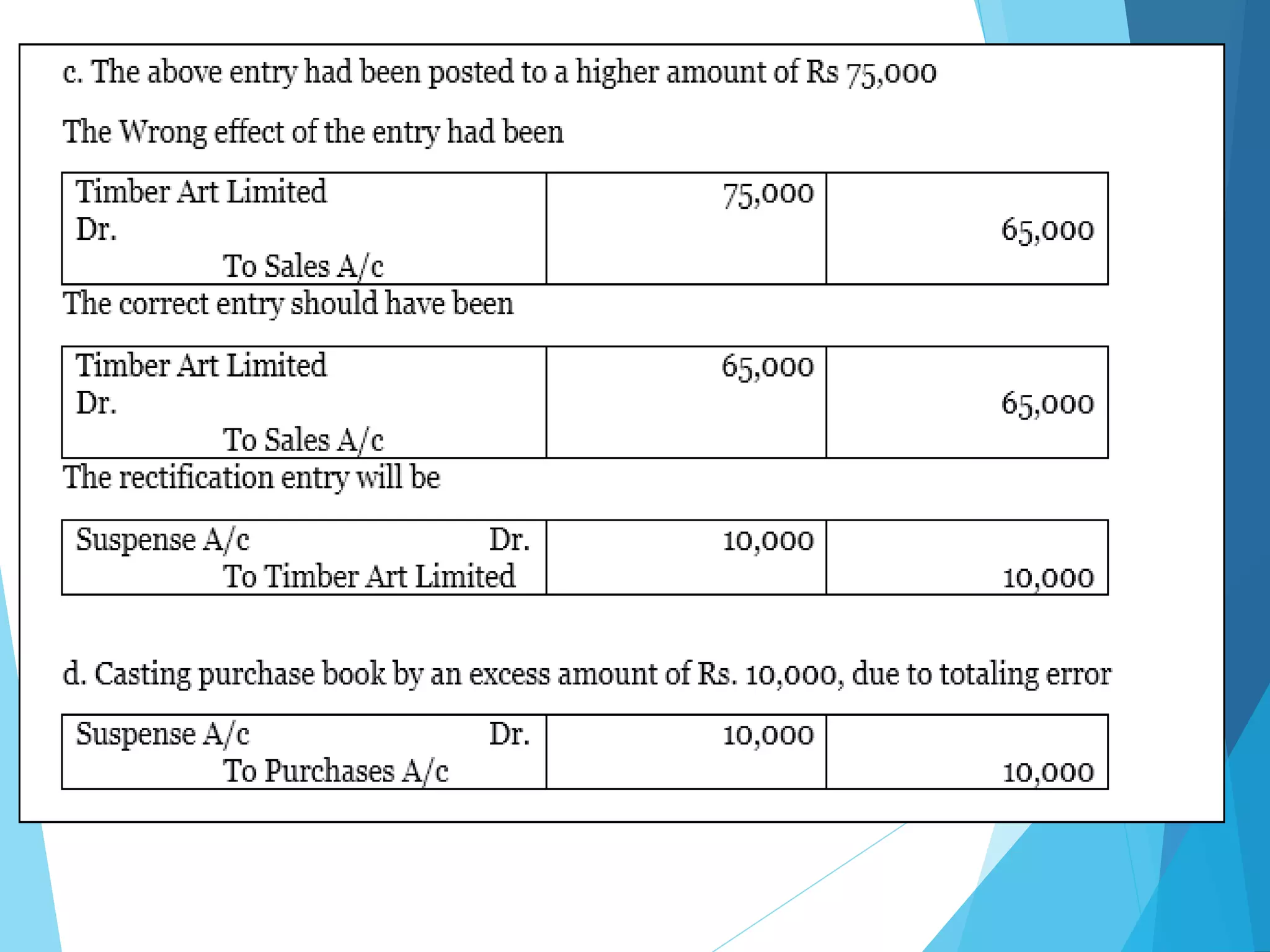

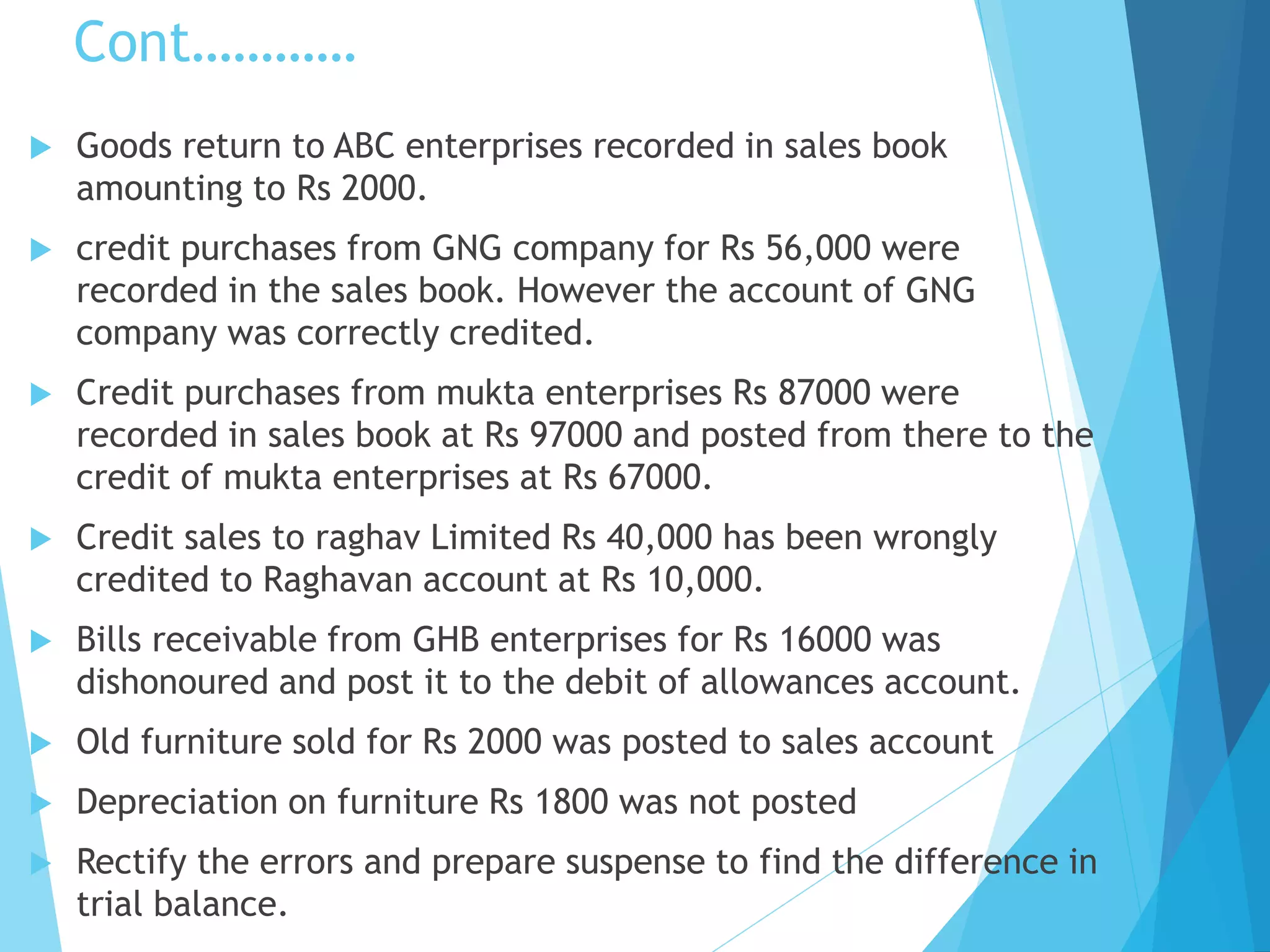

This document discusses the identification and rectification of errors in a trial balance. It outlines steps that can be taken to identify errors, such as checking totals and comparing to previous periods. Errors are classified as those that do or do not affect the trial balance. Errors not affecting the trial balance are rectified through reversing and correcting journal entries. Errors affecting the trial balance are rectified by journal entry or through a suspense account. The document provides examples and practice questions.