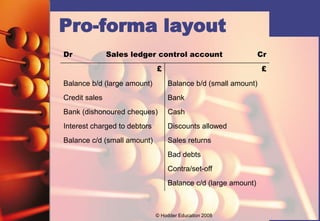

Control accounts are ledger accounts used to control sections of the ledger. The balance on a control account should equal the total balances of the individual accounts it controls. Examples include a sales ledger control account that summarizes customer accounts and a purchases ledger control account that summarizes supplier accounts. Control accounts are kept in the general ledger and help locate errors, prevent fraud, and calculate totals for the financial statements.