Downloaded 60 times

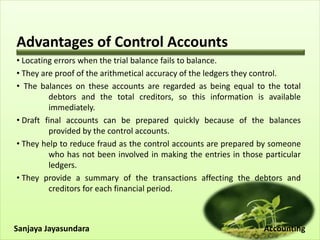

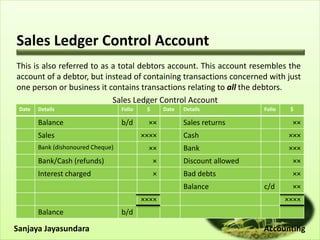

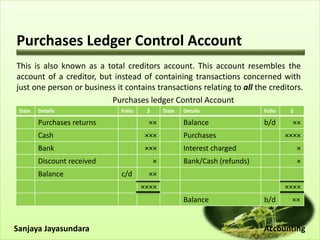

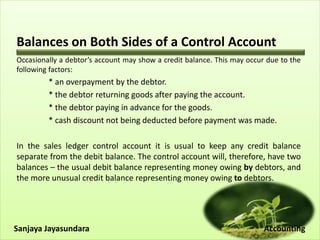

The document explains control accounts, which are tools used in accounting to summarize customer and supplier transactions, helping to identify errors in the sales and purchase ledgers. It discusses the advantages of control accounts, including facilitating error detection, ensuring arithmetical accuracy, and reducing fraud. Furthermore, it provides an overview of the sales and purchases ledger control accounts, detailing balances and contra entries.