Downloaded 14,260 times

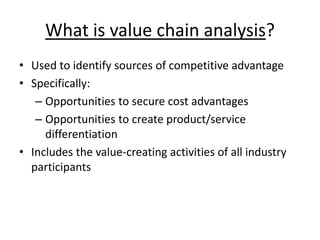

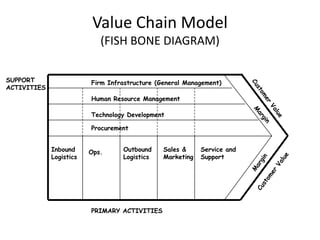

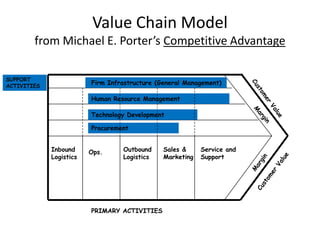

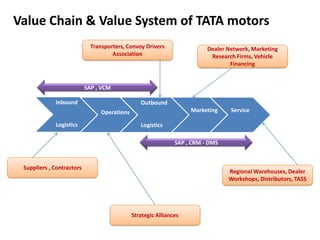

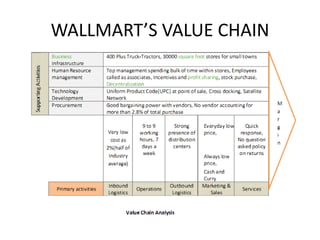

Value chain analysis is a tool used to identify sources of competitive advantage. It examines a firm's activities and how they interact and affect costs and performance. Michael Porter developed the value chain model which divides a firm's activities into primary and support activities. Primary activities directly involve creating and delivering a product. Support activities provide inputs for primary activities. Tata Motors' value chain includes long-term supplier contracts, efficient manufacturing processes, a large dealer network, and investments in research and development. Analyzing a firm's value chain can reveal opportunities to lower costs or differentiate products compared to competitors.