The document discusses the three tiers of capital requirements under the Basel II accord:

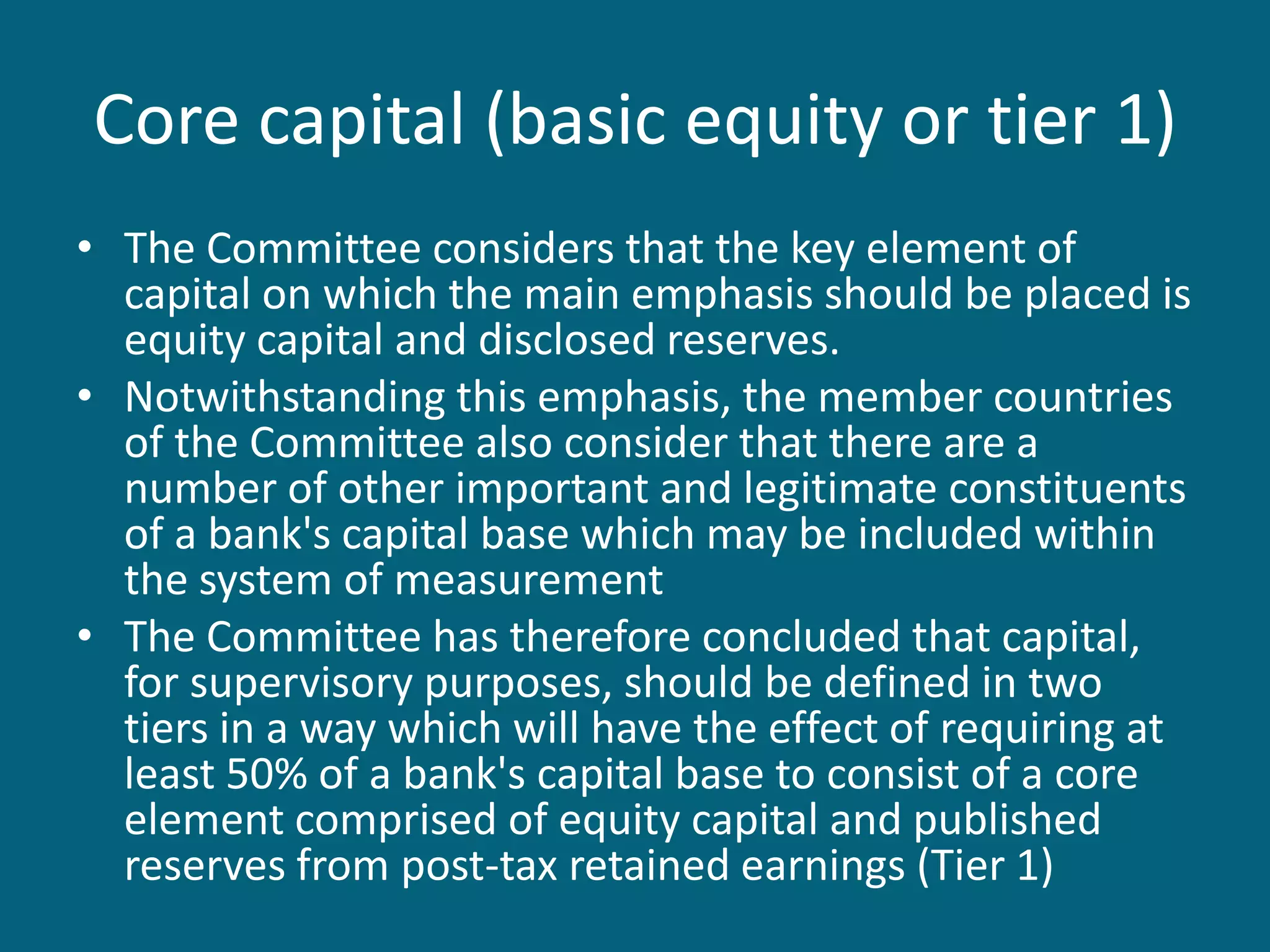

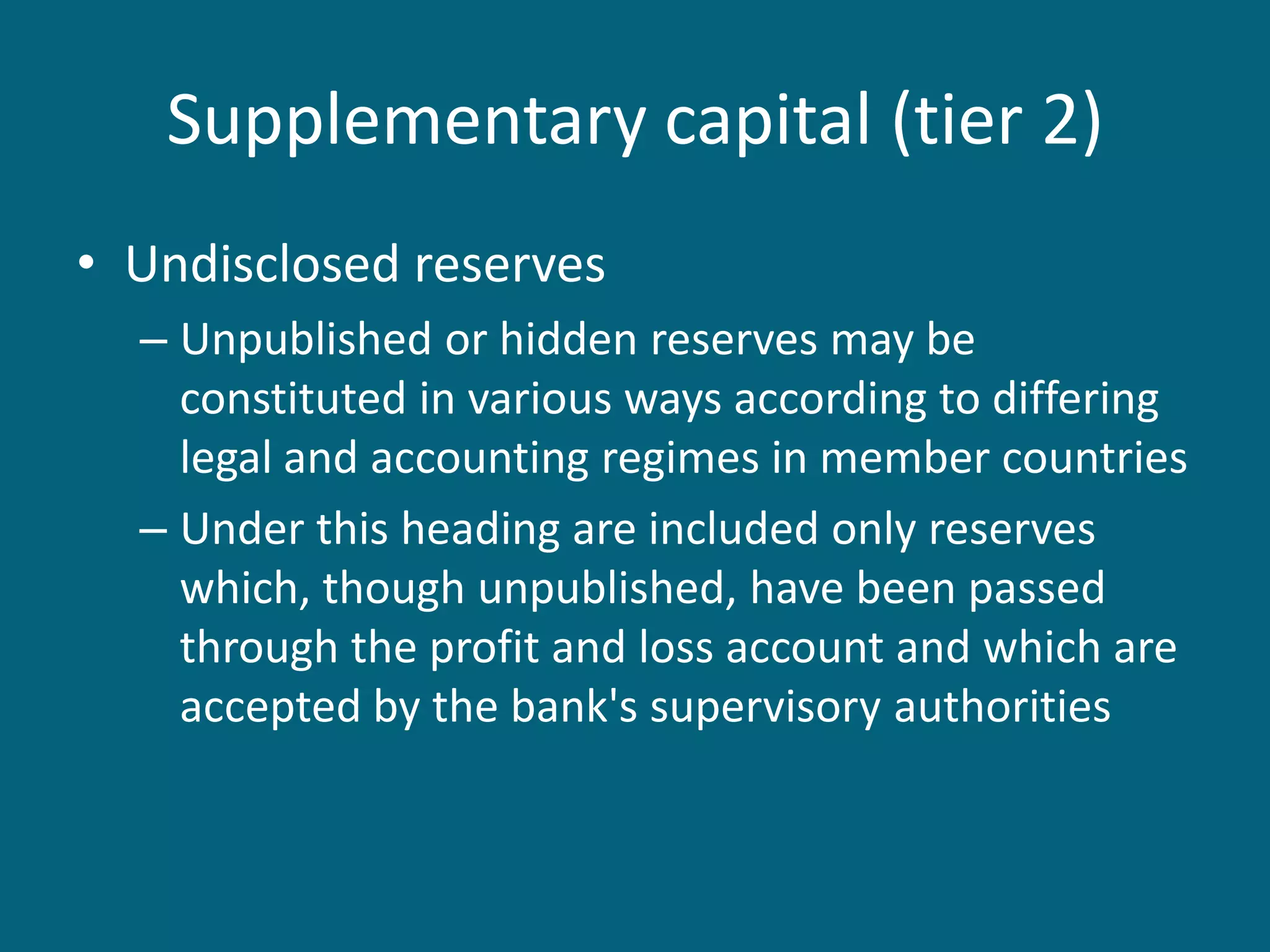

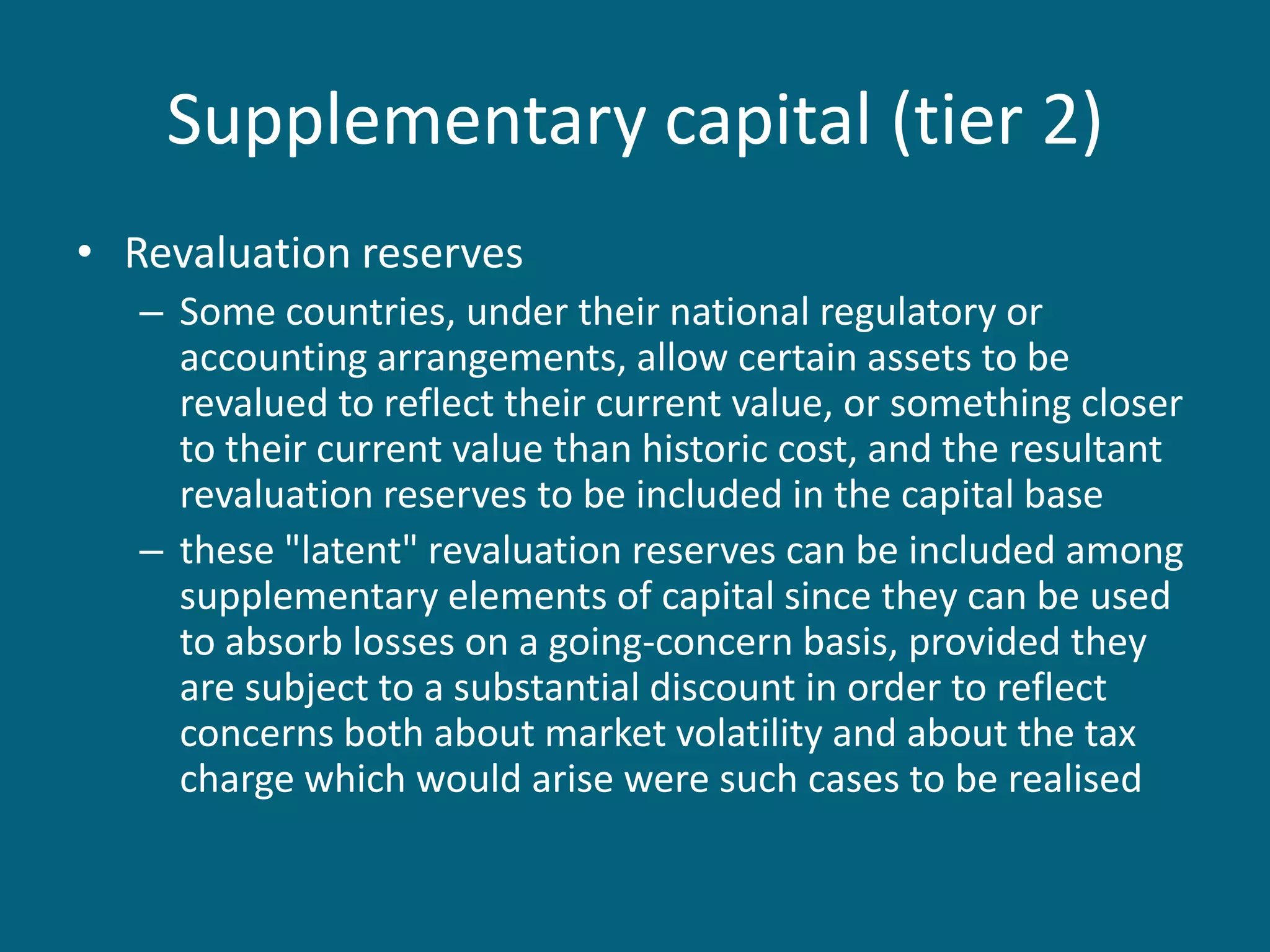

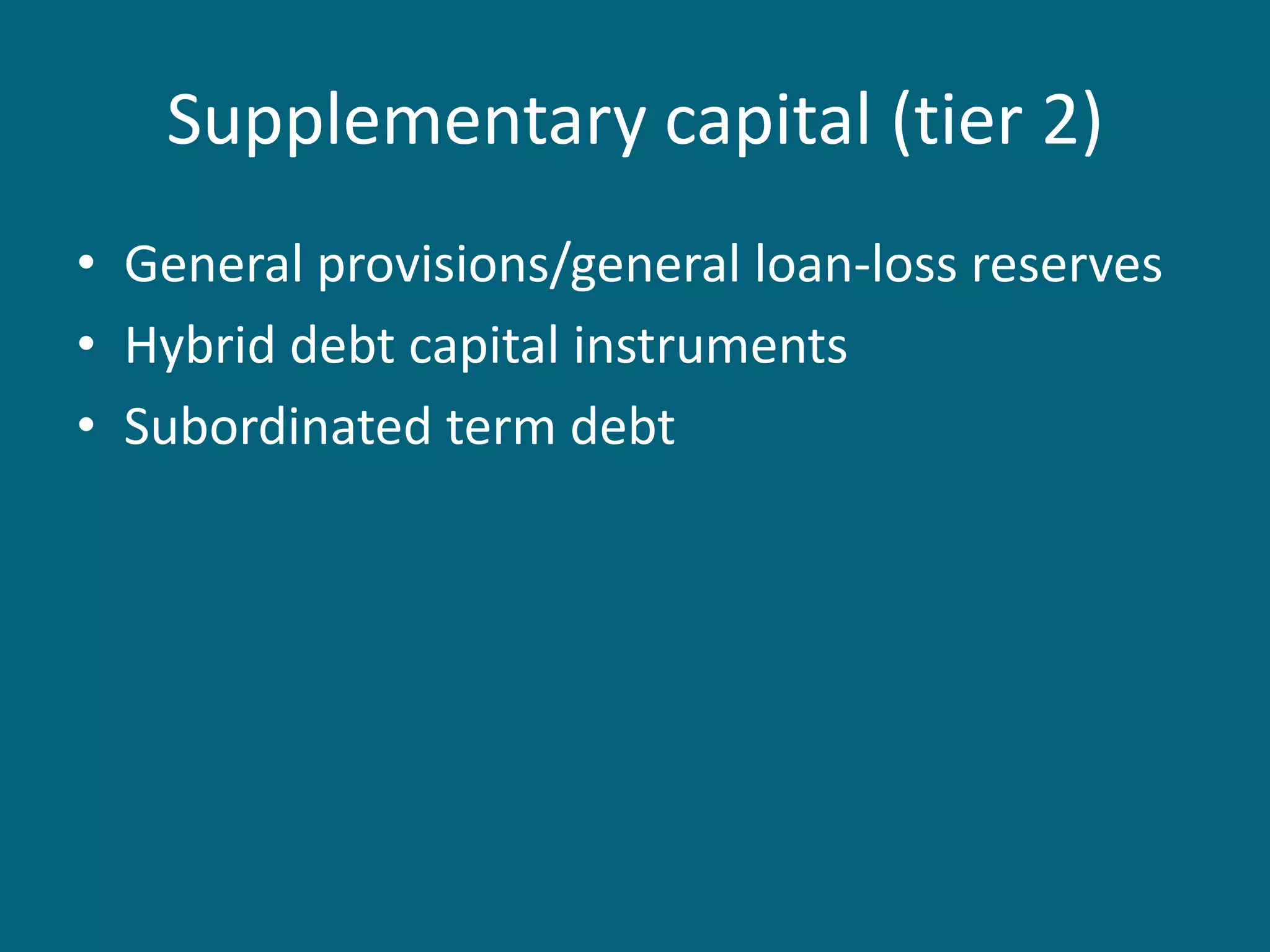

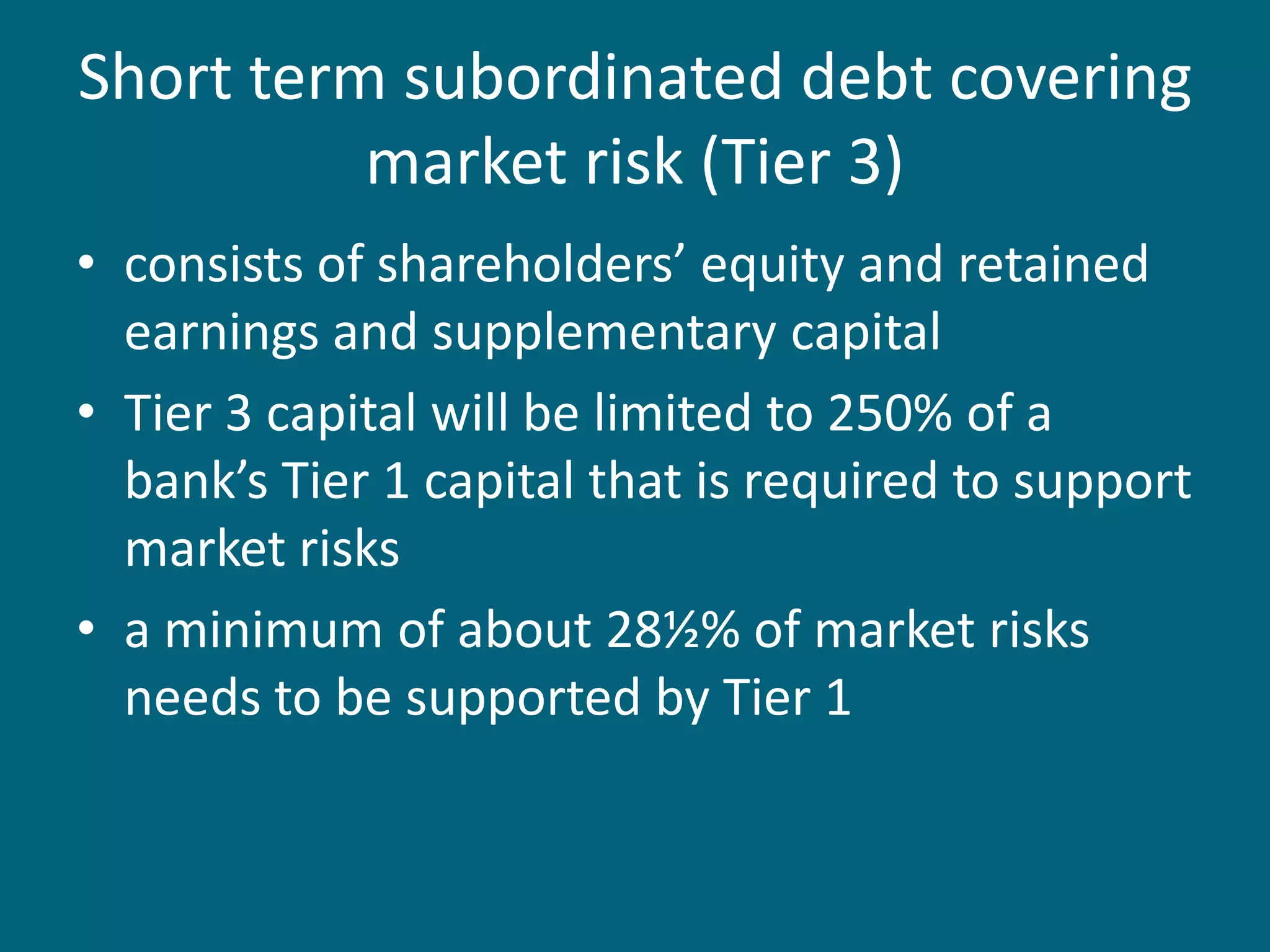

Tier 1 capital consists of core equity and reserves, and must comprise at least 50% of a bank's total capital base. Tier 2, or supplementary capital, includes undisclosed reserves, revaluation reserves, general provisions, and various subordinated debt instruments. Tier 3 capital is short-term subordinated debt limited to 250% of Tier 1 capital required to support market risks, with a minimum of 281⁄2% of market risks supported by Tier 1 capital.