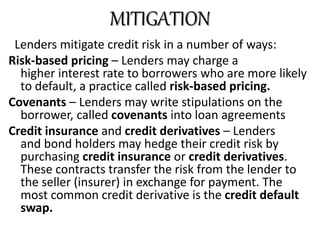

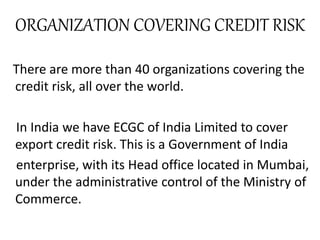

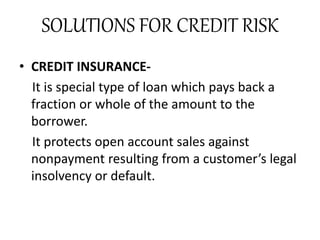

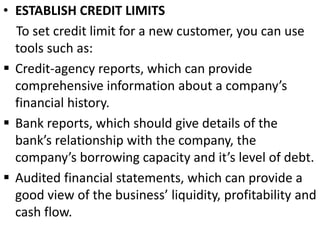

Credit risk is the risk that a borrower may not repay a loan, resulting in potential loss for the lender. It is assessed through factors like the borrower's credit history and capacity to repay, and can be mitigated through methods such as risk-based pricing, covenants, and credit insurance. Various organizations, including India's ECGC, help cover credit risk, while solutions like credit limits and factoring can further manage this risk.