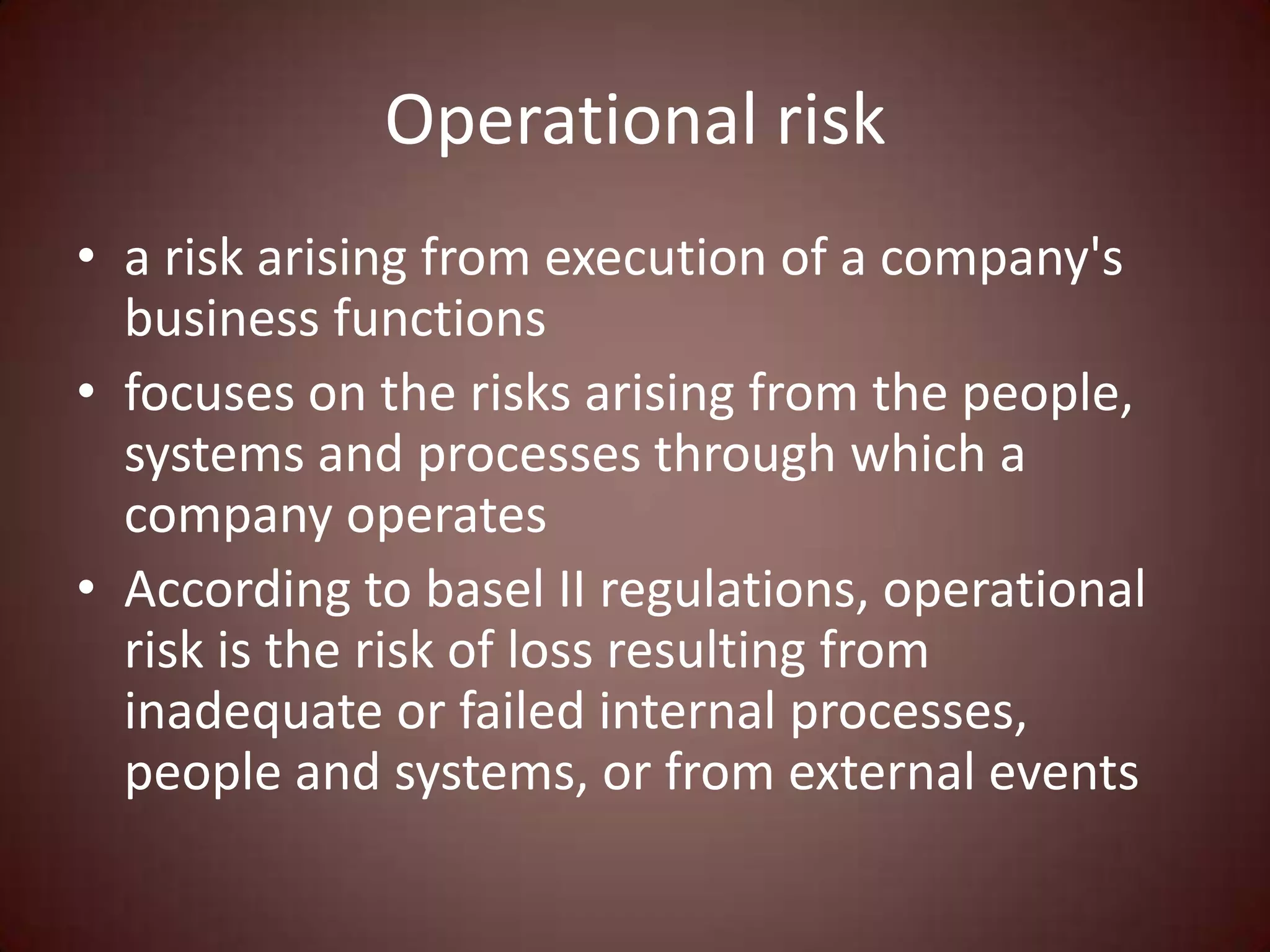

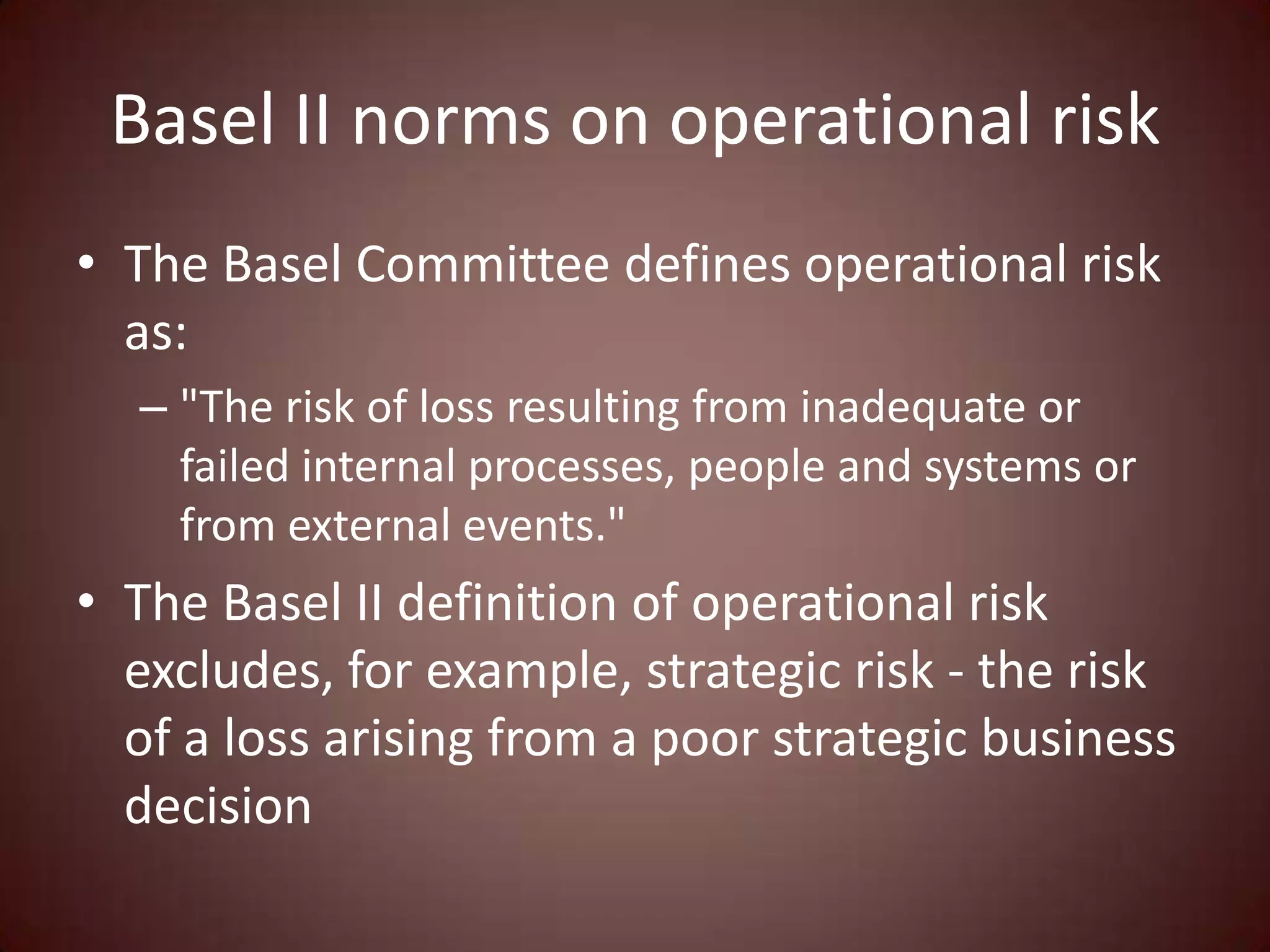

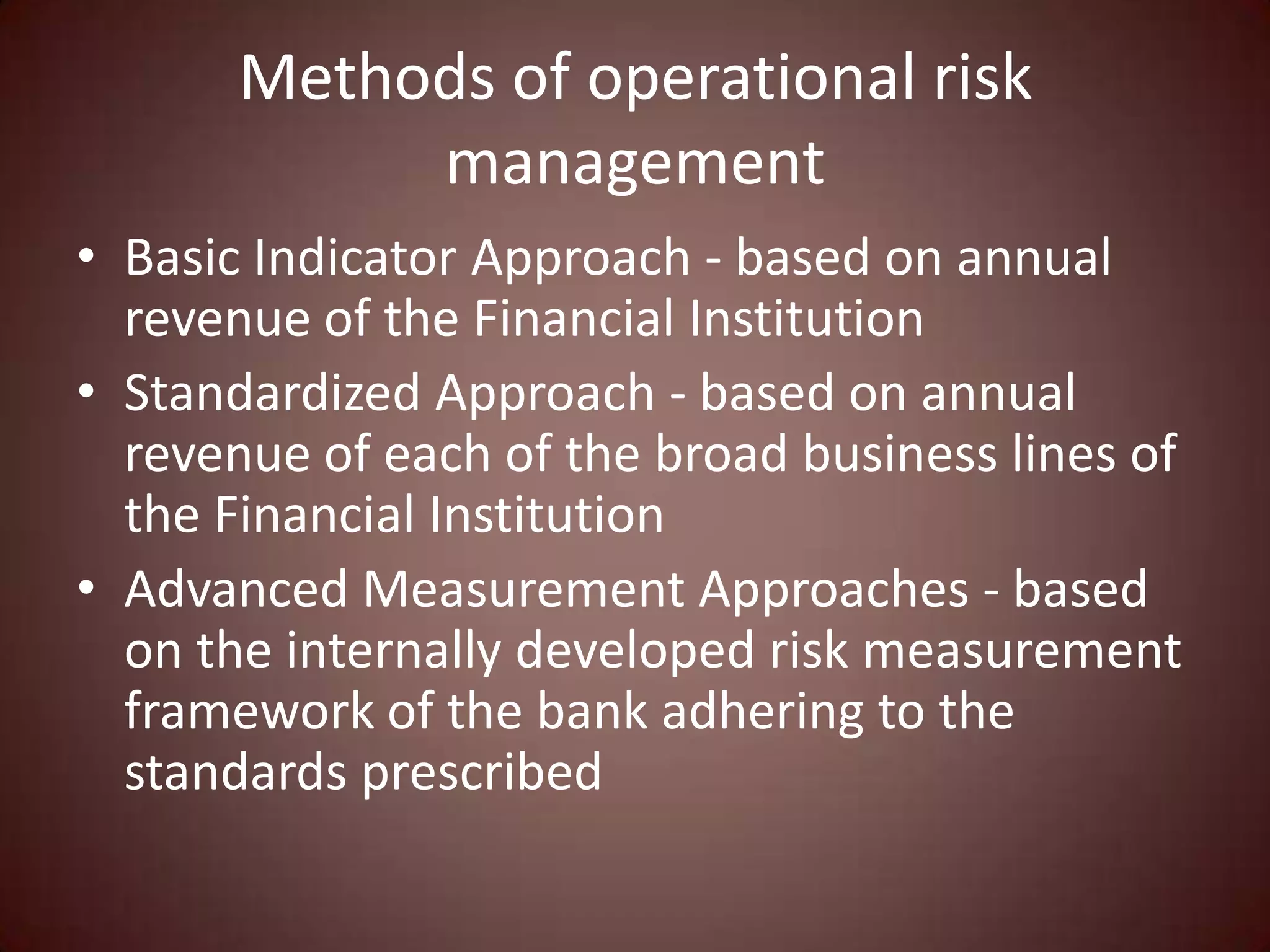

Basel II norms define operational risk as the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events. Basel II is the international capital adequacy framework for banks that prescribes capital requirements for credit risk, market risk and operational risk. There are three approaches under Basel II to measure and manage operational risk: the Basic Indicator Approach, which is based on annual revenue of the Financial Institution; the Standardized Approach, which is based on annual revenue of each broad business line; and the Advanced Measurement Approaches, which rely on the bank's internally developed risk measurement framework.