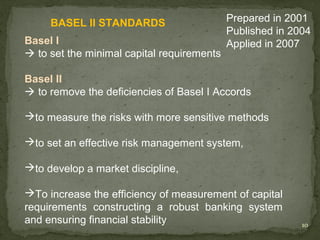

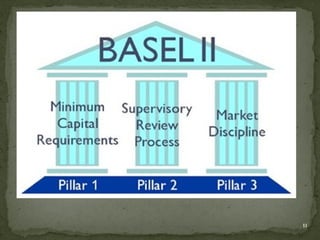

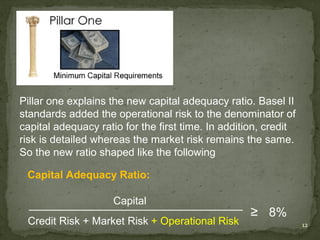

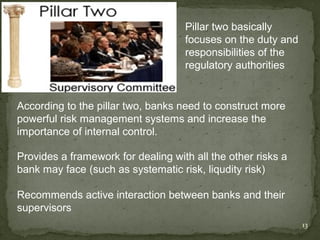

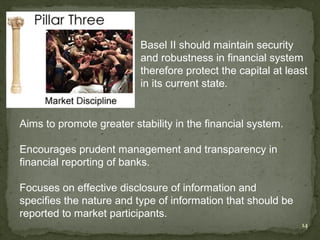

The document discusses Basel regulations on bank capital requirements. It provides an overview of Basel I, Basel II, and Basel III. Basel I introduced uniform capital adequacy calculations but had limitations. Basel II aimed to address Basel I deficiencies by introducing operational risk and more risk-sensitive credit risk calculations. Basel III further strengthened regulations by requiring higher quality capital holdings and introducing leverage ratios. The implications for small- and medium-sized enterprises include potentially higher credit costs, an increased focus on risk ratings, and a need for greater financial transparency.