Downloaded 1,864 times

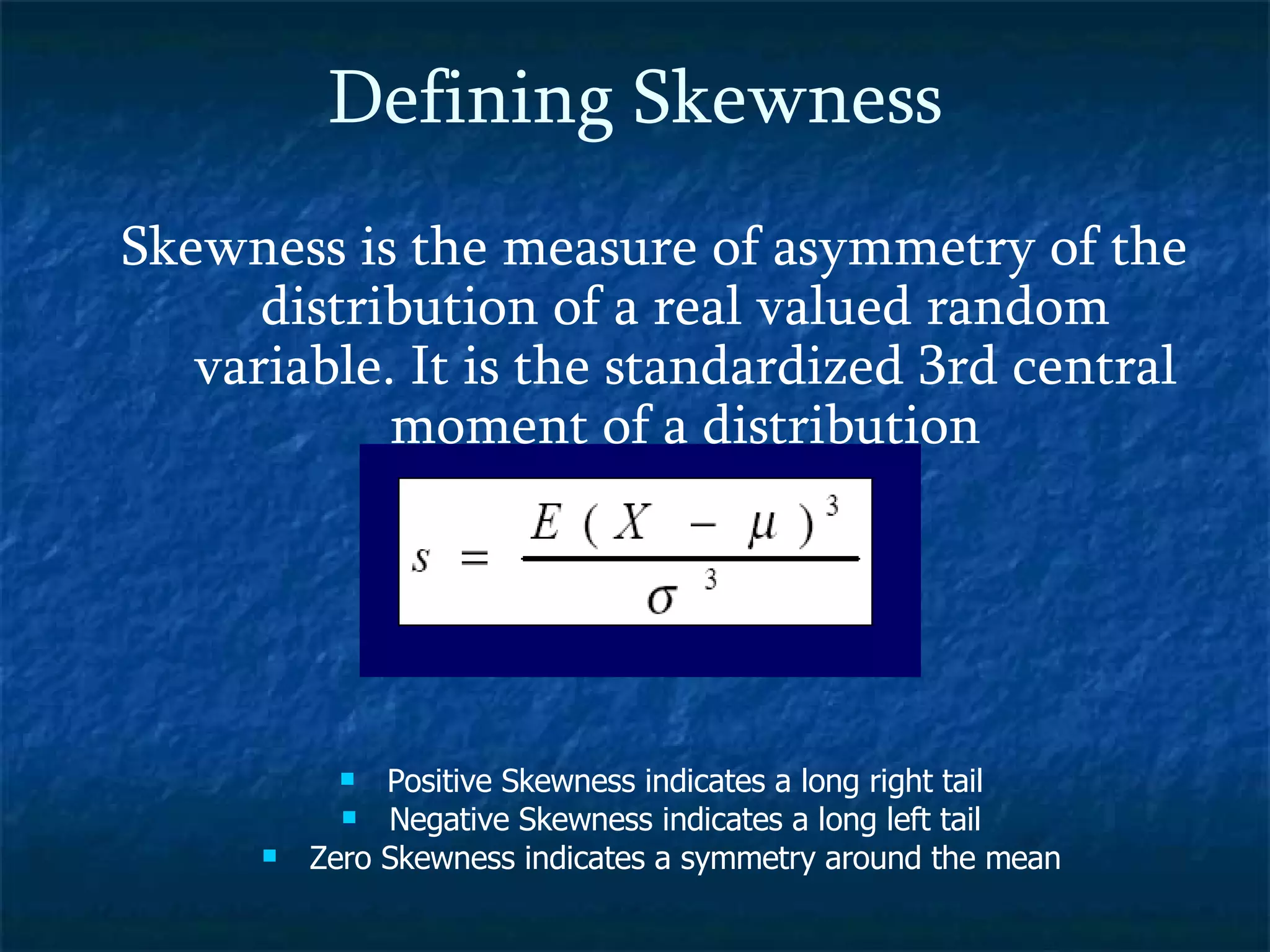

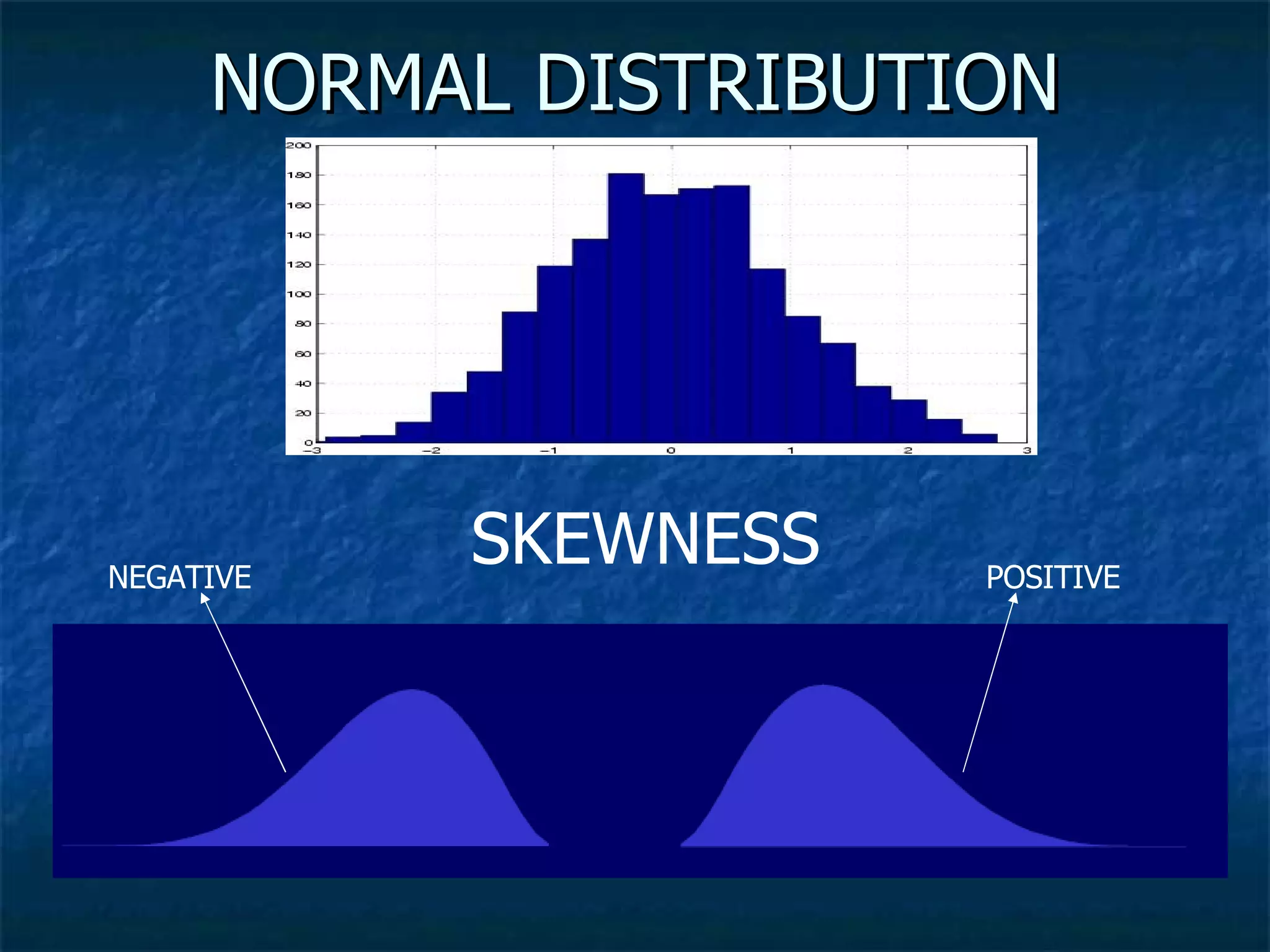

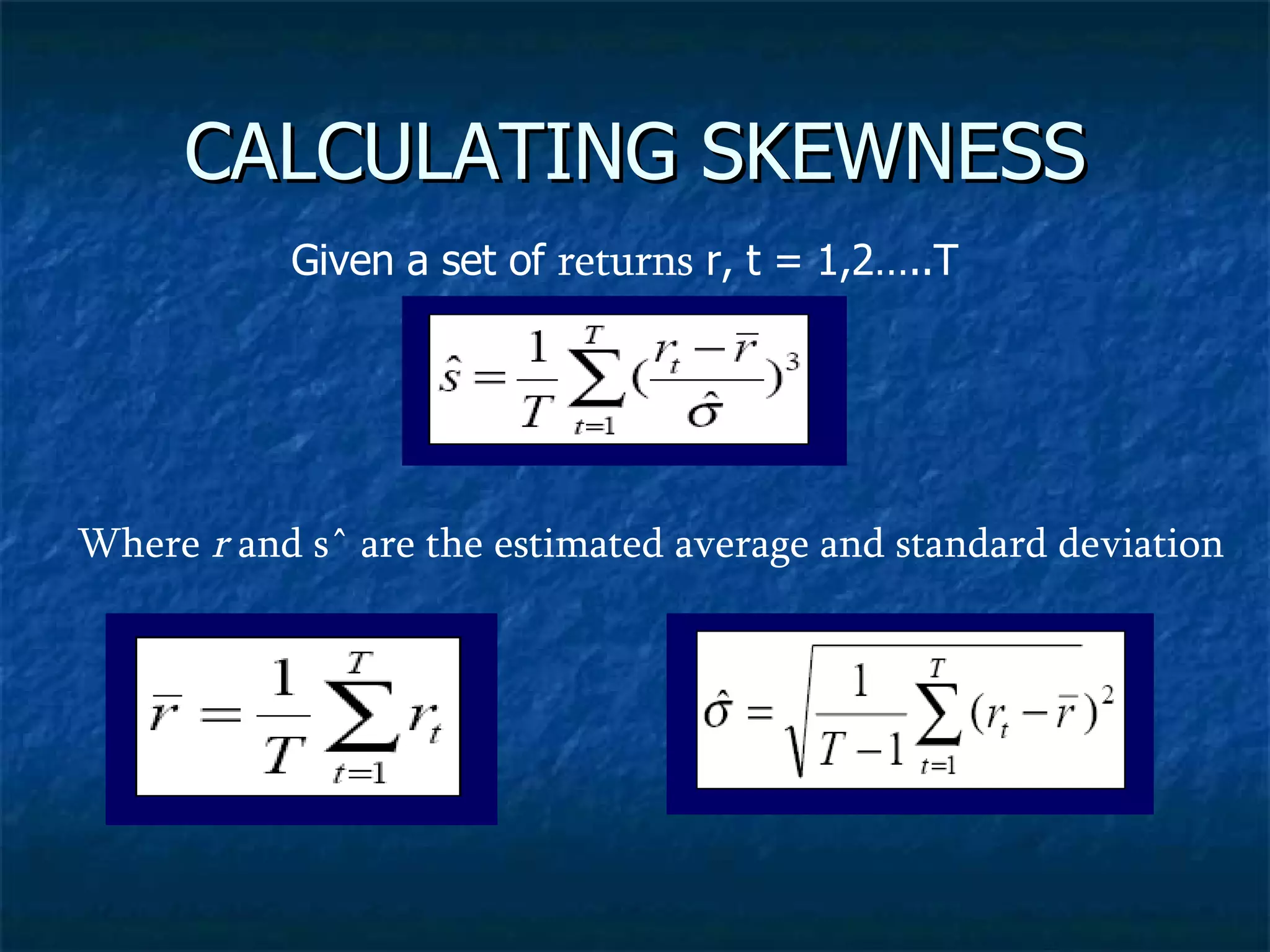

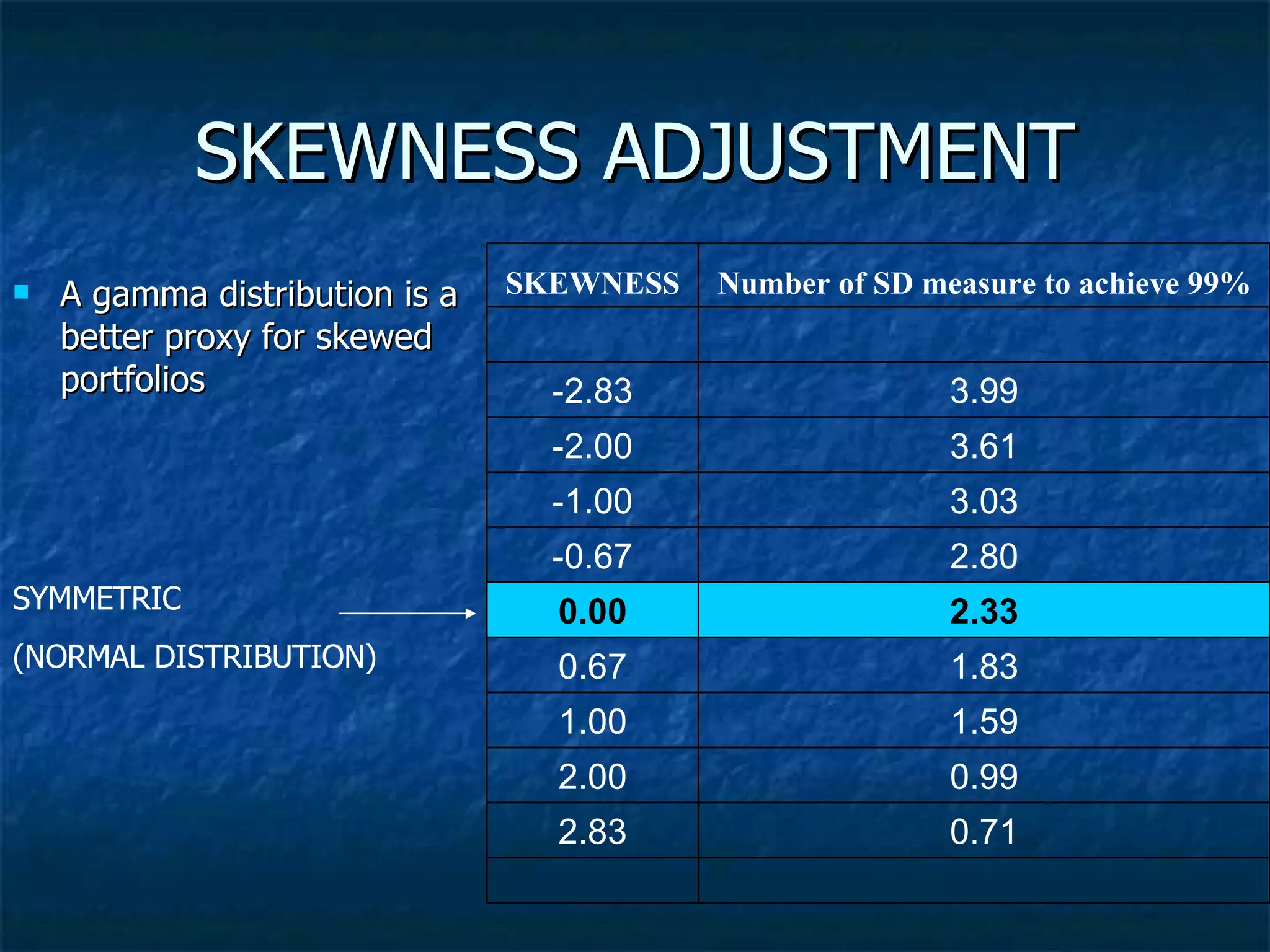

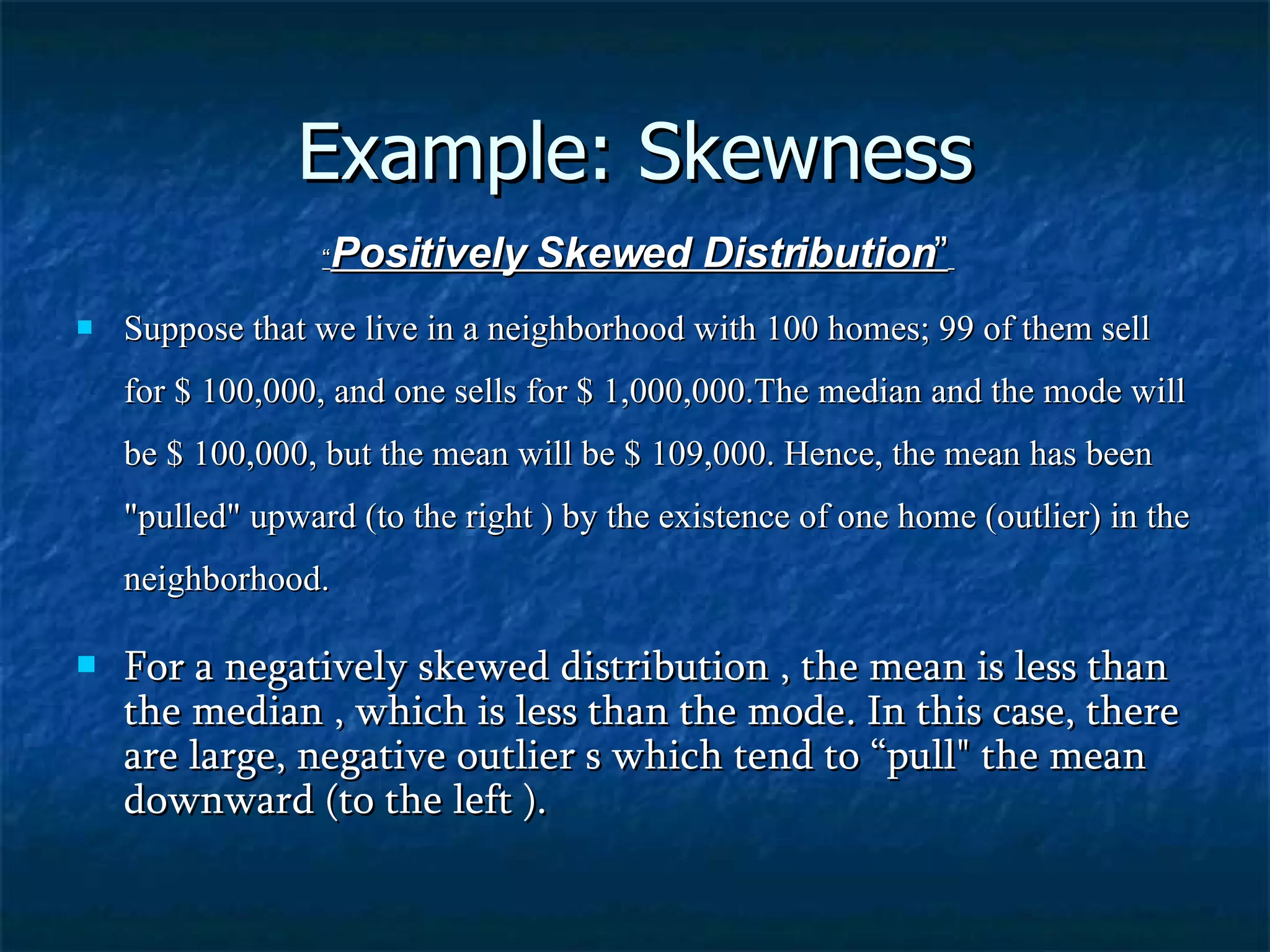

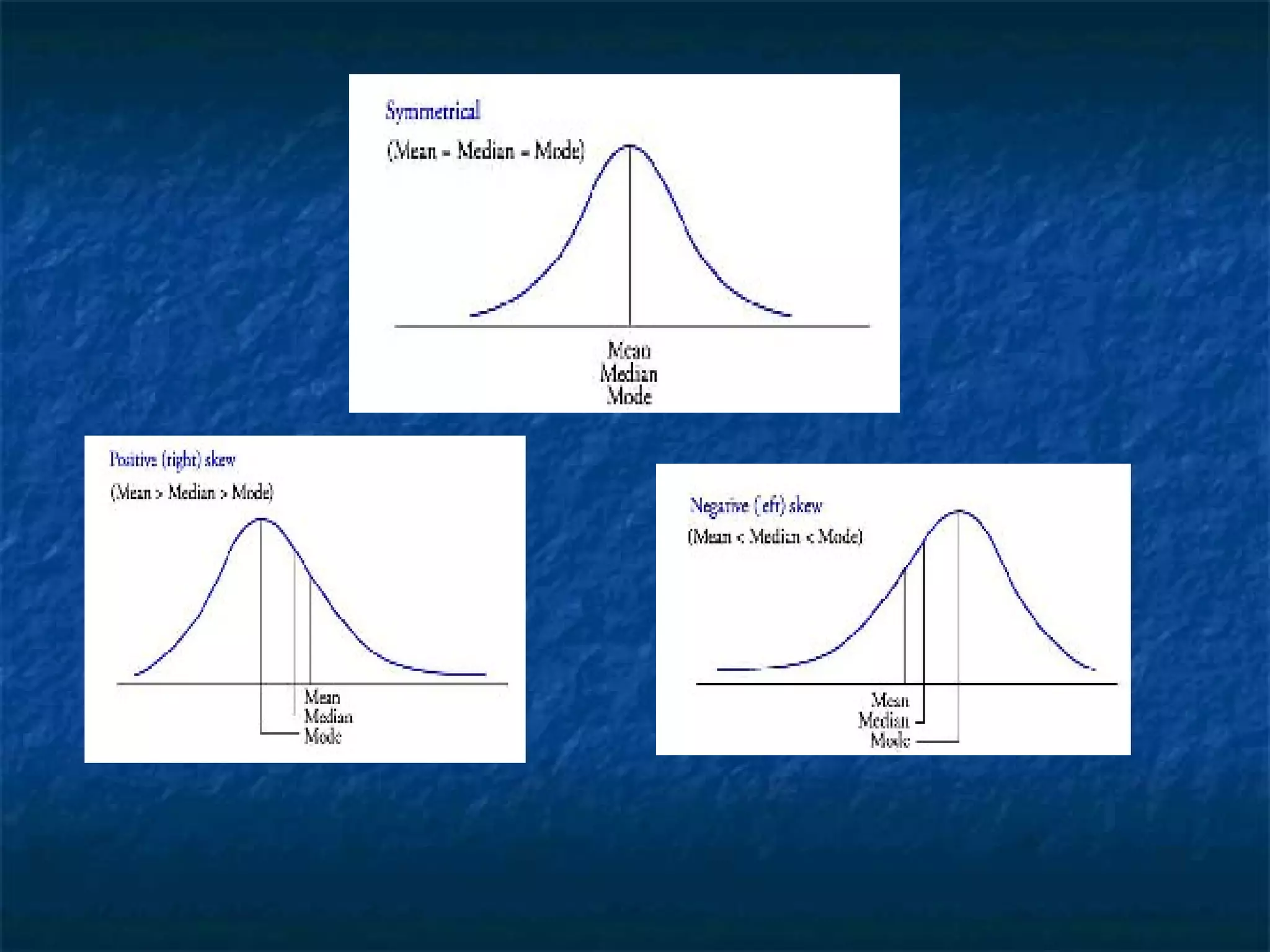

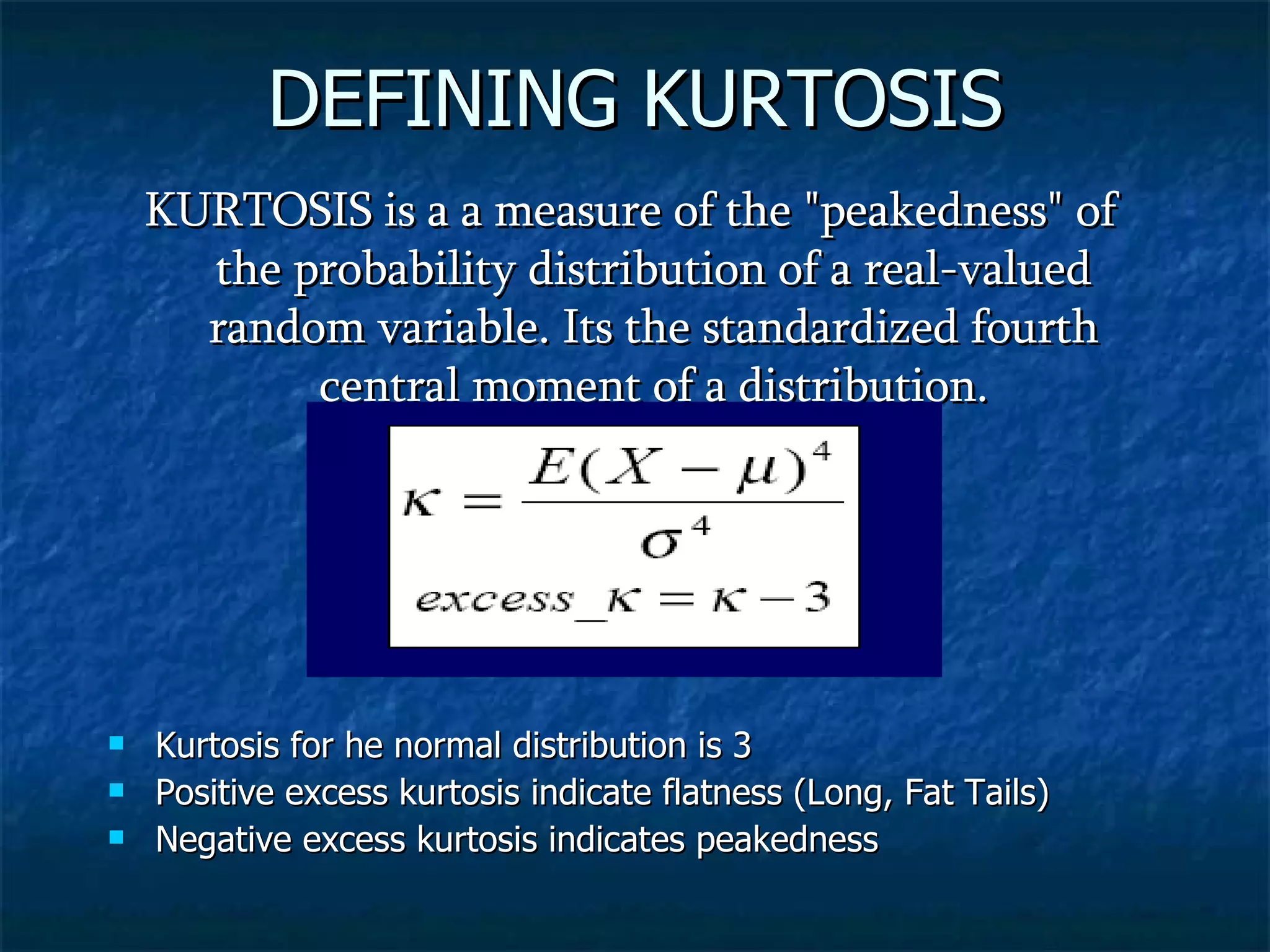

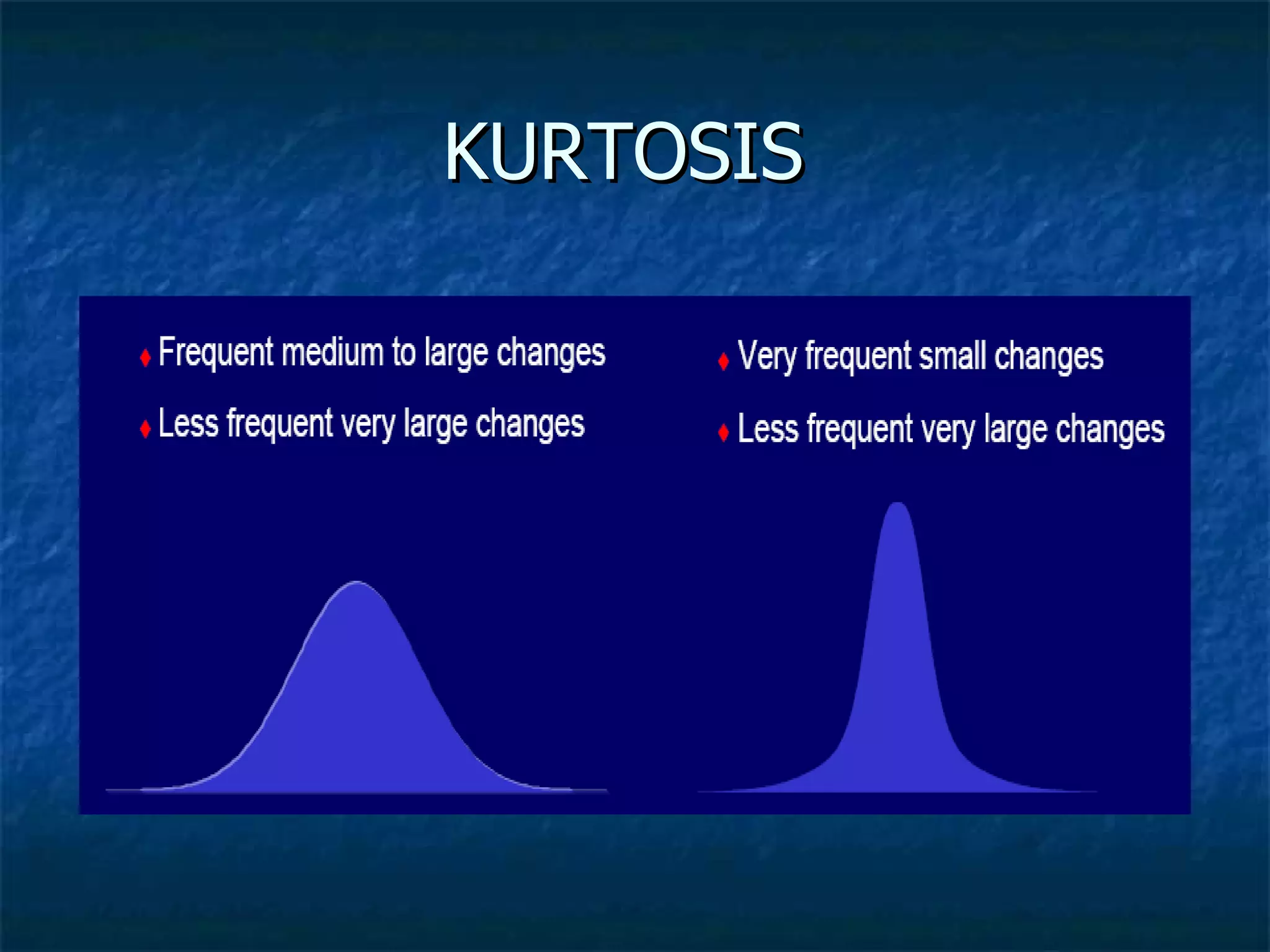

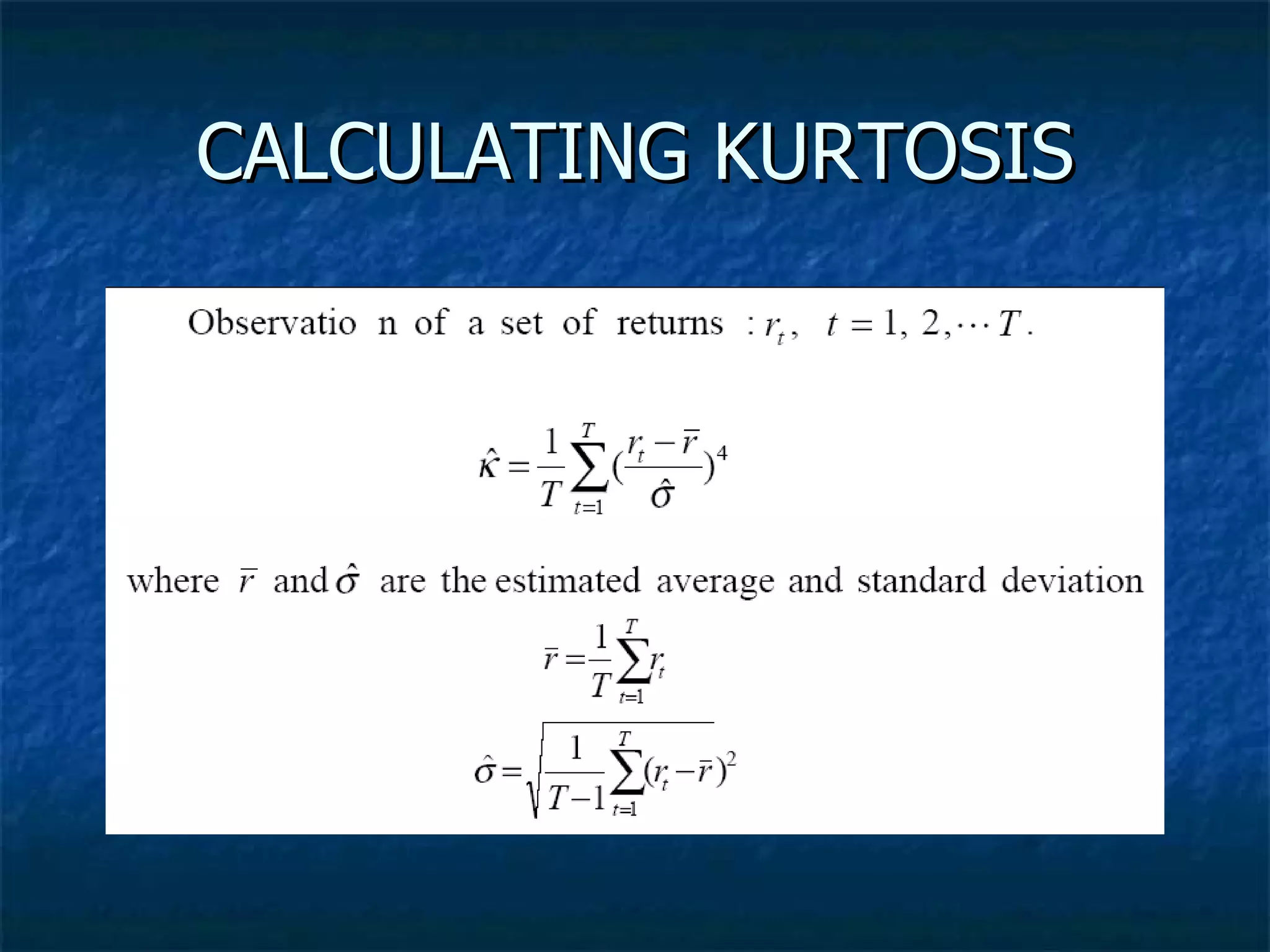

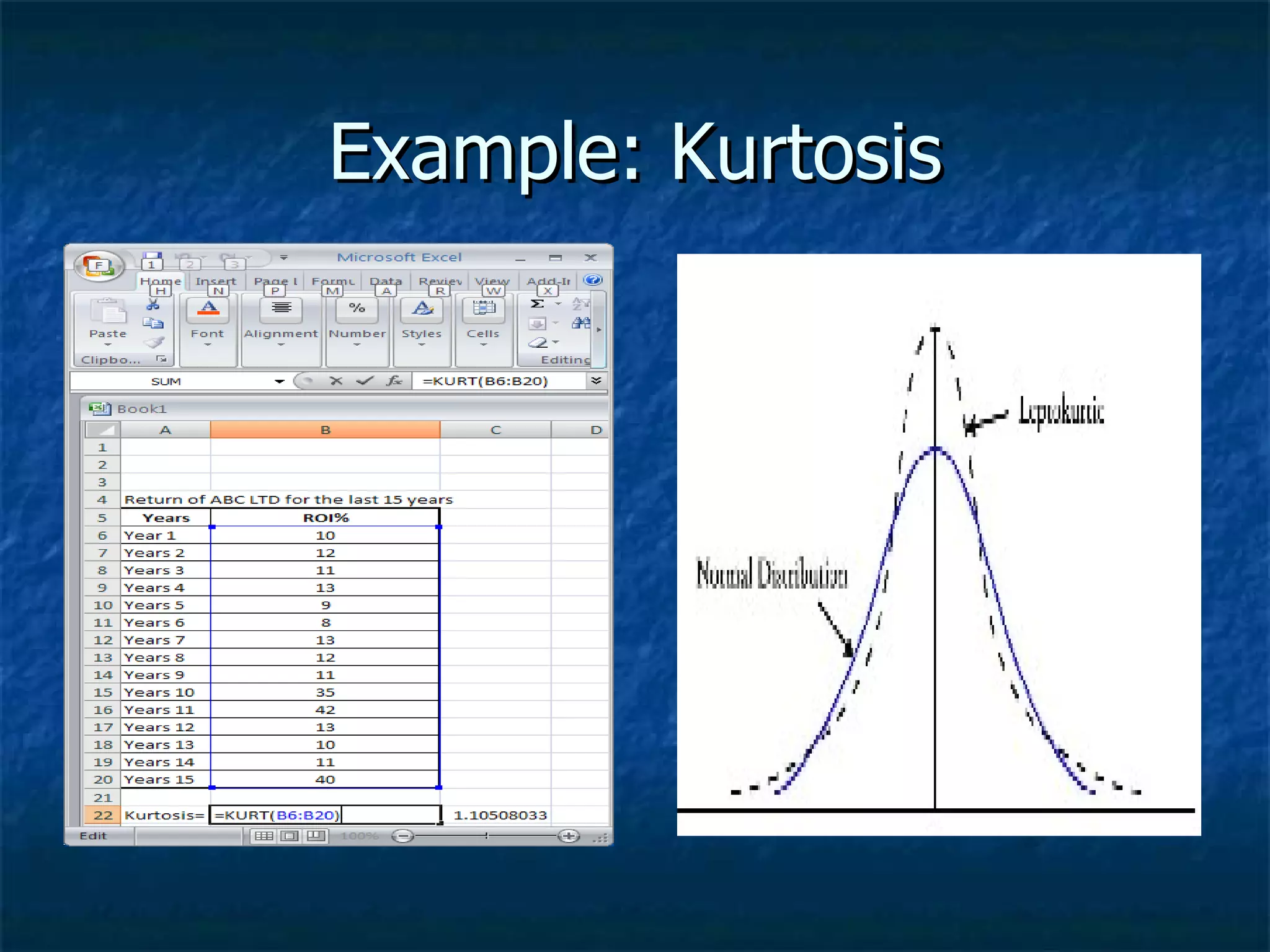

This document discusses skewness and kurtosis in a financial context. It defines skewness as a measure of asymmetry in a distribution, with positive skewness indicating a long right tail and negative skewness a long left tail. Kurtosis is defined as a measure of the "peakedness" of a probability distribution, with positive excess kurtosis indicating flatness/long fat tails and negative excess kurtosis indicating peakedness. Formulas are provided for calculating skewness and kurtosis from a data set. Examples of positively and negatively skewed distributions are given to illustrate these concepts.

![Skewness and Kurtosis[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/skewnessandkurtosis1-230825165704-d8480639-thumbnail.jpg?width=640&height=640&fit=bounds)

![ANALYSIS_OF_CONSTANTS[1].pptxggggggggggggggggggggggggggg](https://cdn.slidesharecdn.com/ss_thumbnails/analysisofconstants1-241002101844-cdec51f2-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DevFest Strasbourg 2025] - NodeJs Can do that !!](https://cdn.slidesharecdn.com/ss_thumbnails/devfeststrasbourg2025-nodejscandothat-251127142731-da65b6fd-thumbnail.jpg?width=640&height=640&fit=bounds)

![[BDD 2025 - Full-Stack Development] Digital Accessibility: Why Developers nee...](https://cdn.slidesharecdn.com/ss_thumbnails/fs-digitalaccessibilitywhydevelopersneedtoknowandcarein2025-251127011019-0674441d-thumbnail.jpg?width=640&height=640&fit=bounds)

![[BDD 2025 - Full-Stack Development] PHP in AI Age: The Laravel Way. (Rizqy Hi...](https://cdn.slidesharecdn.com/ss_thumbnails/fs-phpinaiagethelaravelway-251125012602-ef9d330e-thumbnail.jpg?width=640&height=640&fit=bounds)

![[BDD 2025 - Mobile Development] Crafting Immersive UI with E2E and AGSL Shade...](https://cdn.slidesharecdn.com/ss_thumbnails/md-craftingimmersiveuiwithe2eandagslshaderveronicaputrianggraini-251124030840-0c677f44-thumbnail.jpg?width=640&height=640&fit=bounds)

![[BDD 2025 - Mobile Development] Exploring Apple’s On-Device FoundationModels](https://cdn.slidesharecdn.com/ss_thumbnails/md-exploringappleson-devicefoundationmodels-251124030840-d690542c-thumbnail.jpg?width=640&height=640&fit=bounds)

![[BDD 2025 - Artificial Intelligence] Building AI Systems That Users (and Comp...](https://cdn.slidesharecdn.com/ss_thumbnails/ai-buildingaisystemsthatusersandcompanieslove-251124030845-038f7732-thumbnail.jpg?width=640&height=640&fit=bounds)