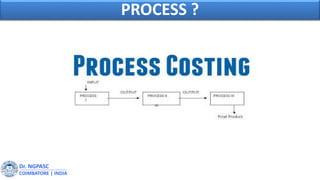

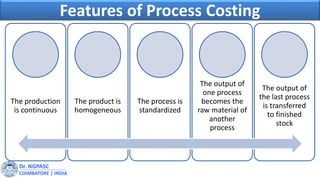

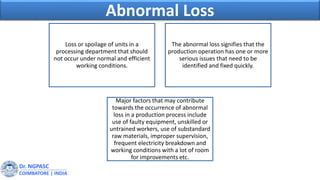

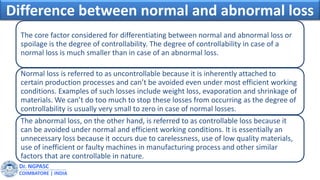

The document discusses process costing, which is a method used to account for the costs of continuous production processes. It defines process costing as dealing with mass production of homogeneous units that pass through a series of production steps or processes. Key characteristics of process costing include continuous production, standardized processes, and accumulating costs by process. The document provides examples of industries that typically use process costing and compares it to job costing. It also defines normal and abnormal losses that can occur in production processes.