Downloaded 150 times

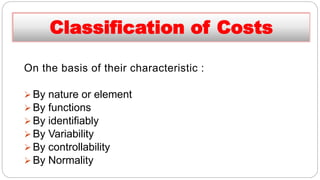

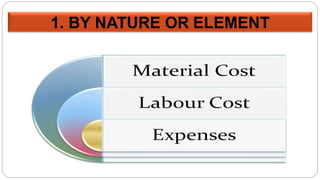

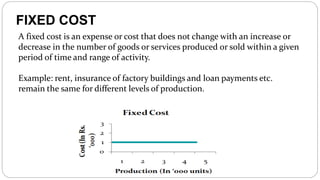

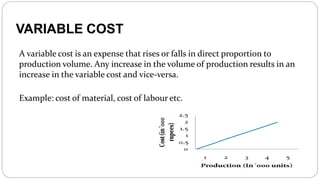

Cost accounting involves classifying costs according to their nature, function, variability, and controllability. There are several types of costs: - Direct costs like materials and labor that are clearly traceable to production. Indirect costs like utilities that are not directly traceable. - Fixed costs that do not vary with production like rent. Variable costs that vary with production like materials. Semi-variable costs that vary but not proportionately. - Controllable costs a manager can influence like direct labor. Uncontrollable costs outside a manager's control like depreciation. - Normal costs incurred during regular operations. Abnormal costs from unexpected events like fires.

![7_C's_OF_COMMUNIOCATION[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7csofcommuniocation1-230801063320-9af405b3-thumbnail.jpg?width=640&height=640&fit=bounds)