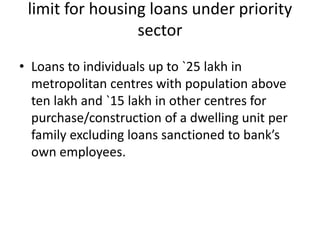

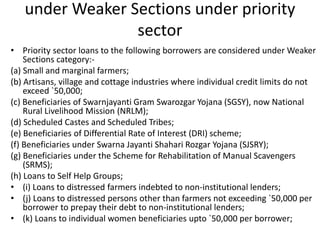

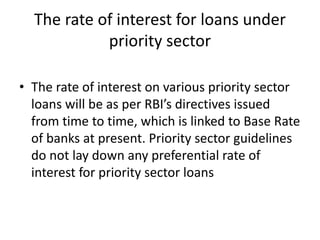

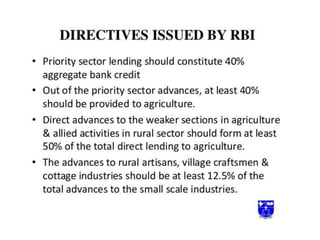

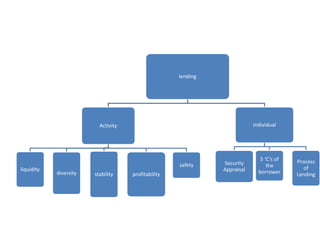

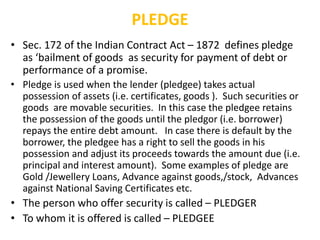

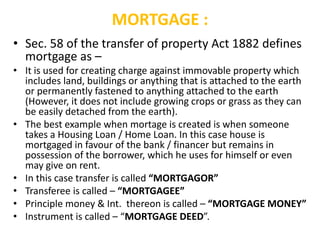

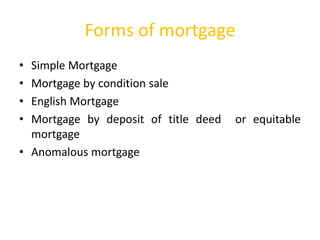

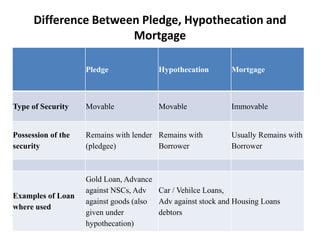

The document discusses principles of lending for banks. It covers key lending principles such as liquidity, safety, diversity, stability and profitability for banks' lending activities. It also discusses principles for individual loans including the 5 C's of lending (character, capacity, capital, collateral, conditions), types of security for loans (lien, negative lien, pledge, hypothecation, mortgage), and priority sector lending targets and categories (agriculture, micro/small enterprises, education, housing, weaker sections).

![HYPOTHECATION :

• It is used for creating charge against the security of movable assets, but

here the possession of the security remains with the borrower itself.

• Thus, in case of default by the borrower, the lender (i.e. to whom the

goods / security has been hypothecated) will have to first take

possession of the security and then sell the same.

• The best example of this type of arrangement are Car Loans. In this case

Car / Vehicle remains with the borrower but the same is hypothecated

to the bank / financer.

• In case the borrower, defaults, banks take possession of the vehicle

after giving notice and then sell the same and credit the proceeds to the

loan account.

• Other examples of these hypothecation are loans against stock and

debtors. [Sometimes, borrowers cheat the banker by partly selling

goods hypothecated to bank and not keeping the desired amount of

stock of goods.

• In such cases, if bank feels that borrower is trying to cheat, then it can

convert hypothecation to pledge i.e. it takes over possession of the

goods and keeps the same under lock and key of the bank].](https://image.slidesharecdn.com/principleoflending-150506051651-conversion-gate02/85/Principle-of-lending-13-320.jpg)

!['Direct Finance' for Agricultural

Purposes

(i) Loans to individual farmers [including Self Help Groups (SHGs) or

Joint Liability Groups (JLGs), i.e. groups of individual farmers]

engaged in Agriculture and Allied Activities, viz., dairy, fishery,

animal husbandry, poultry, bee-keeping and sericulture.

(ii) Loans to corporate including farmers' producer companies of

individual farmers, partnership firms and co-operatives of farmers

directly engaged in Agriculture and Allied Activities, viz., dairy,

fishery, animal husbandry, poultry, bee-keeping and sericultureup to

an aggregate limit of `2 crore per borrower.

(iii) Loans to small and marginal farmers for purchase of land for

agricultural purposes.

(iv) Loans to distressed farmers indebted to non-institutional lenders.

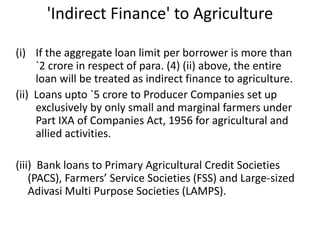

(v) Bank loans to Primary Agricultural Credit Societies (PACS),

Farmers’ Service Societies (FSS) and Large-sized Adivasi Multi

Purpose Societies (LAMPS) ceded to or managed/ controlled by

such banks for on lending to farmers for agricultural and allied

activities.](https://image.slidesharecdn.com/principleoflending-150506051651-conversion-gate02/85/Principle-of-lending-20-320.jpg)