Download to read offline

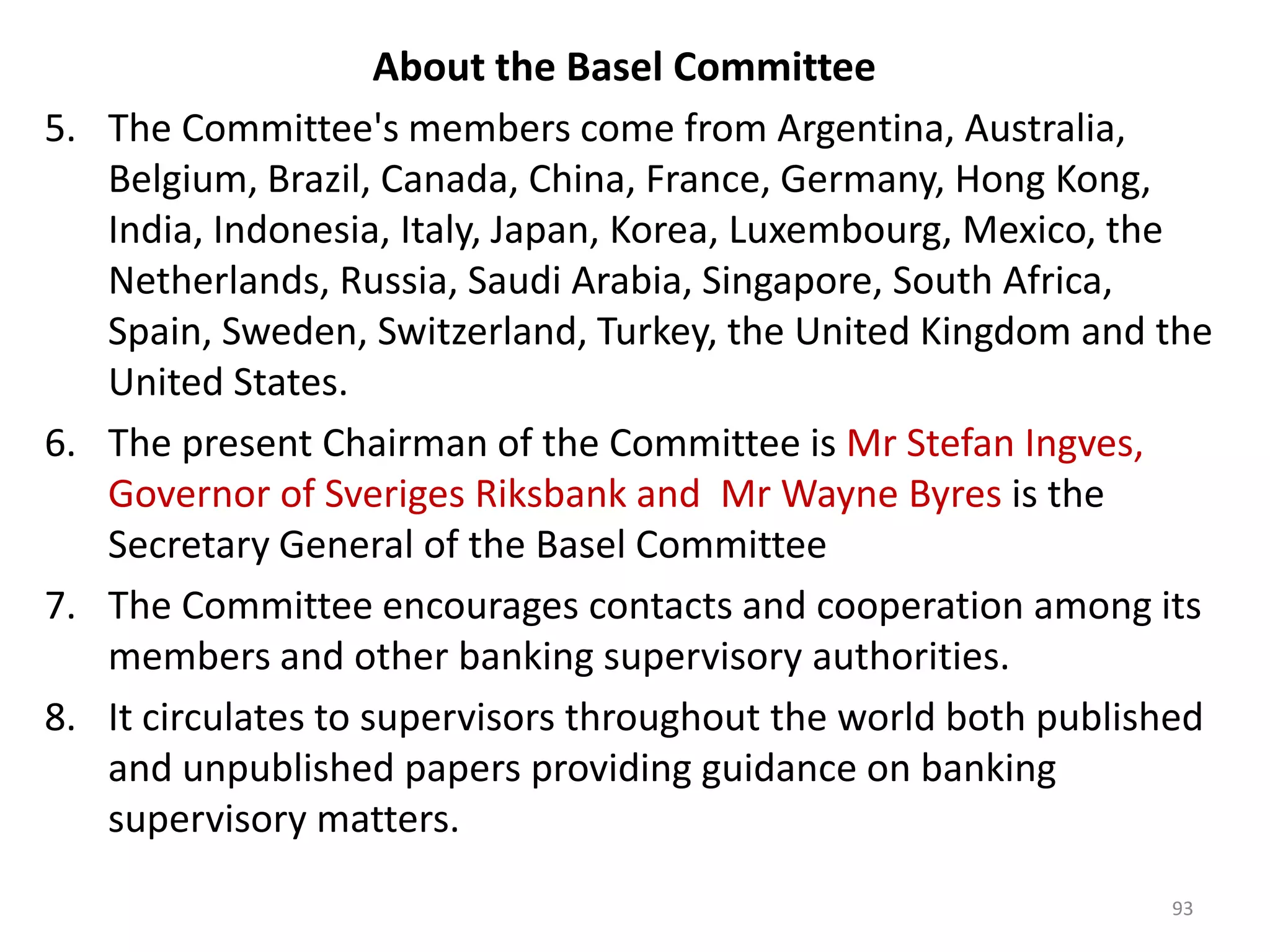

![ALM STATEMENTS TO

BE SUBMITTED TO RBI

1. Statement of Structural Liquidity

(Annexure - I) [DSB Statement No.8] - Rupee

2. Statement of Interest Rate Sensitivity

(Annexure - II) [DSB Statement No. 9] - Rupee

3. Statement of Dynamic Liquidity (Annexure -

III)

4. Statement of Maturity and Position (MAP)

(Annexure - IV) [DSB Statement No.10 ] -

Forex

5. Statement of Sensitivity to Interest Rate

(SIR)(Annexure - V)[DSB Statement No.11] -](https://image.slidesharecdn.com/banking-130407142723-phpapp01/75/Banking-54-2048.jpg)

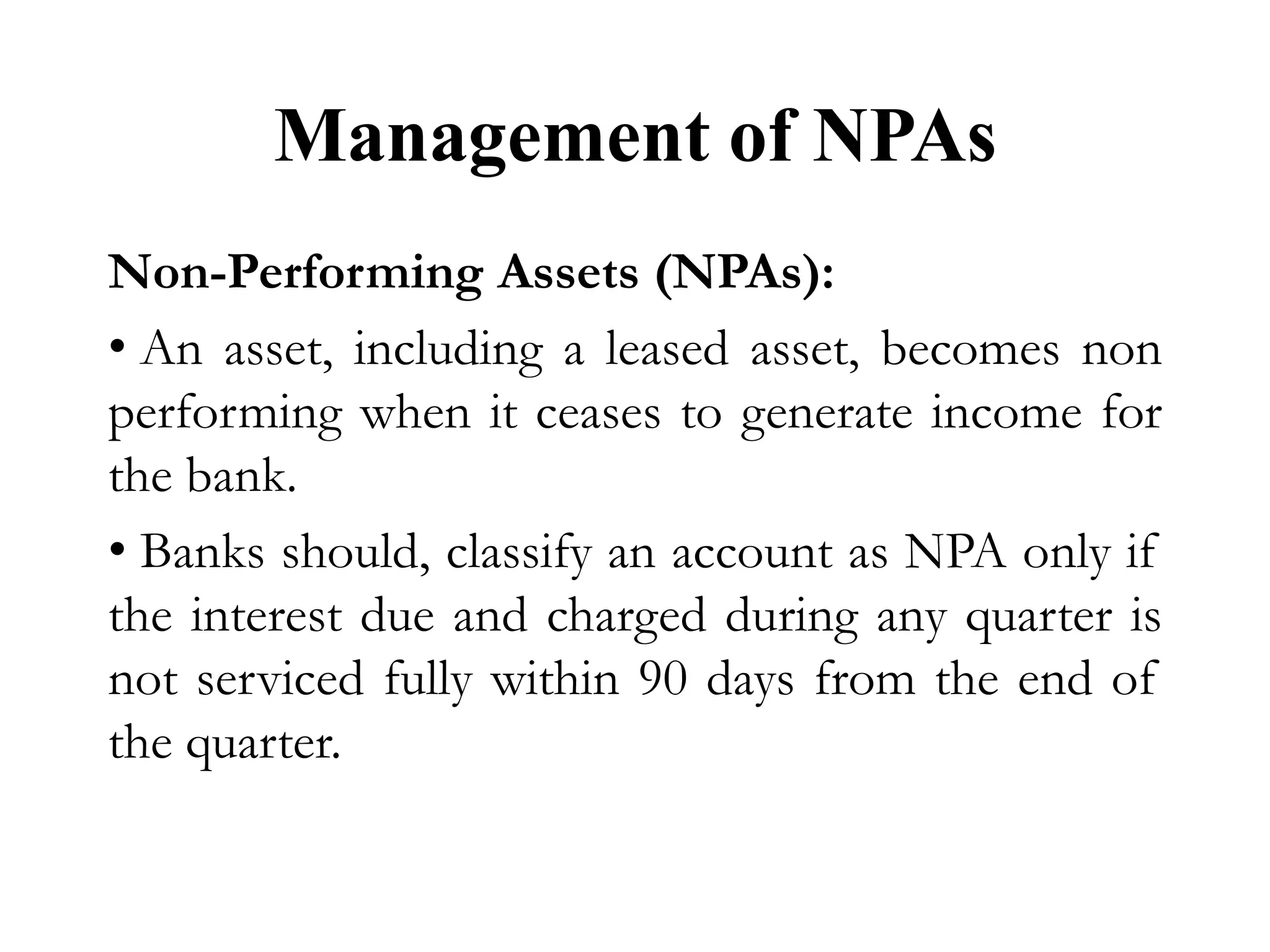

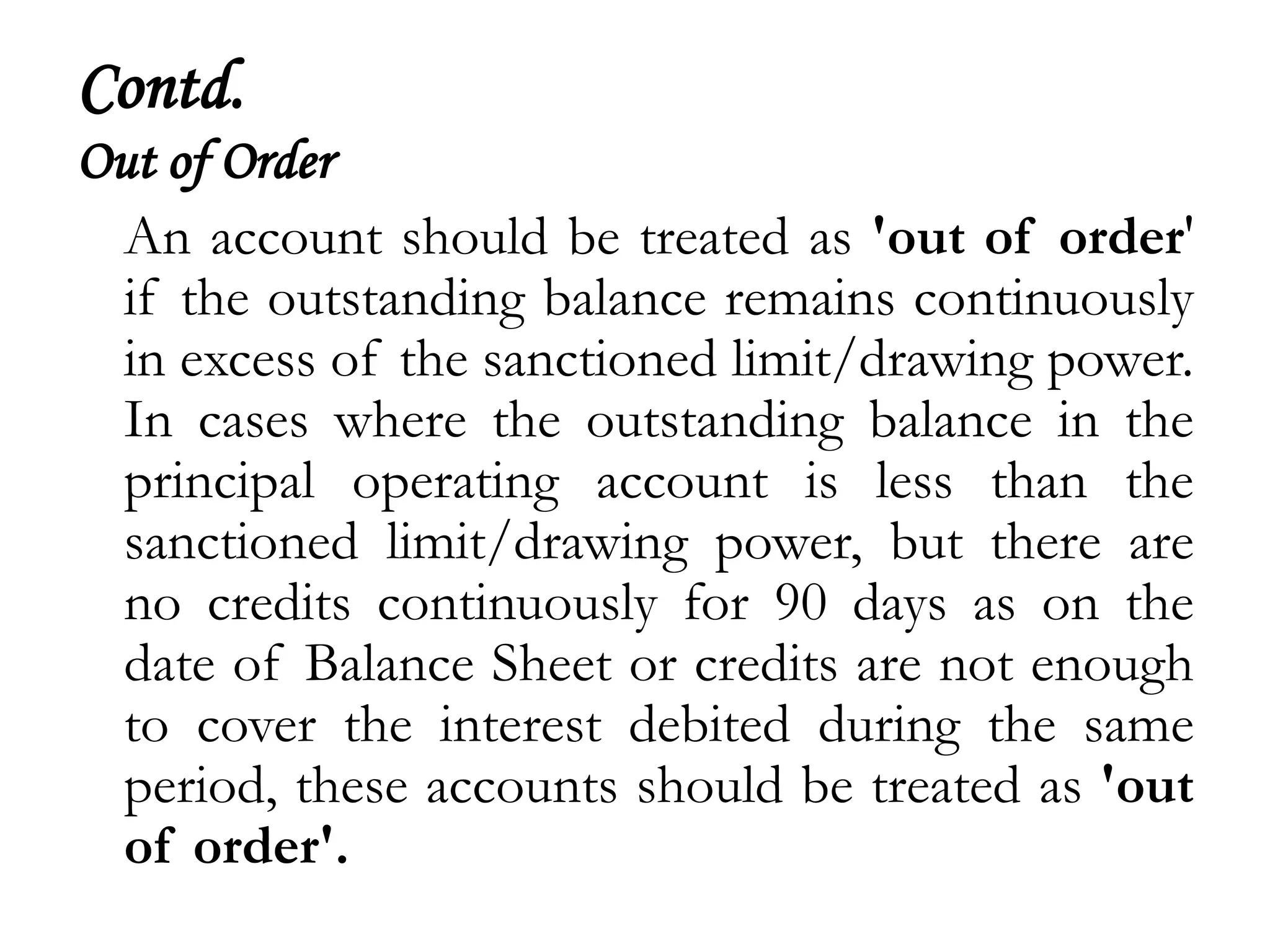

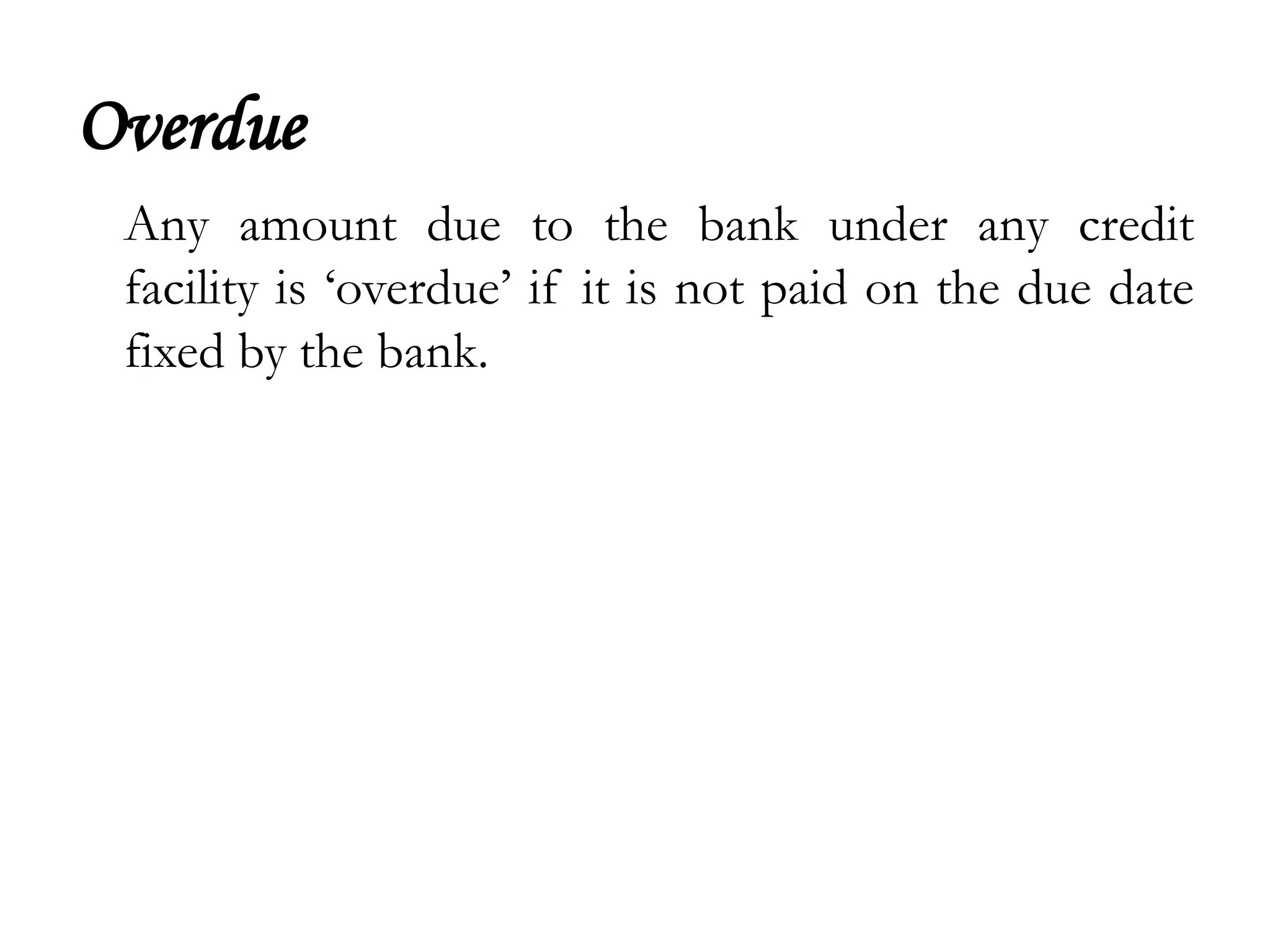

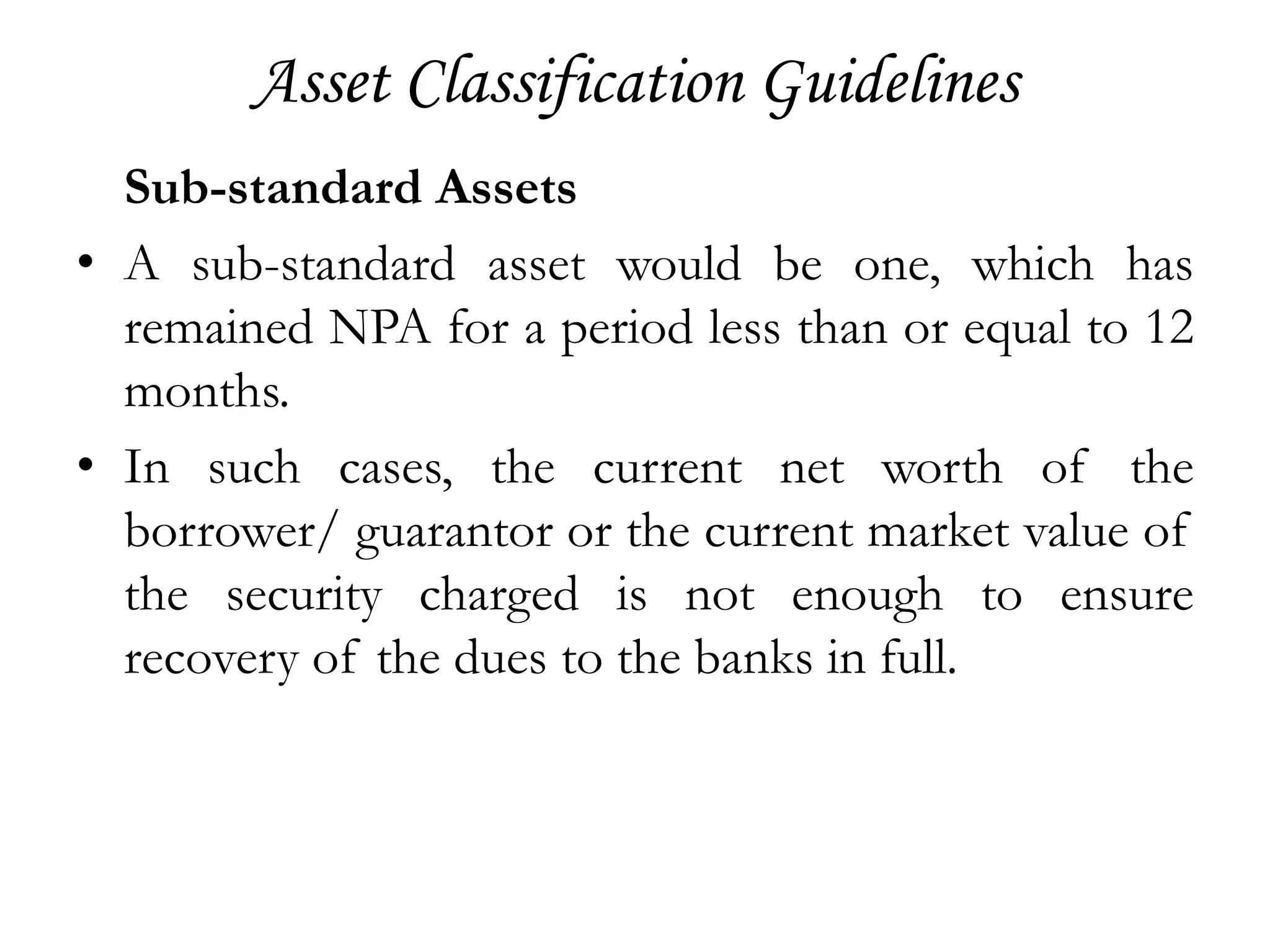

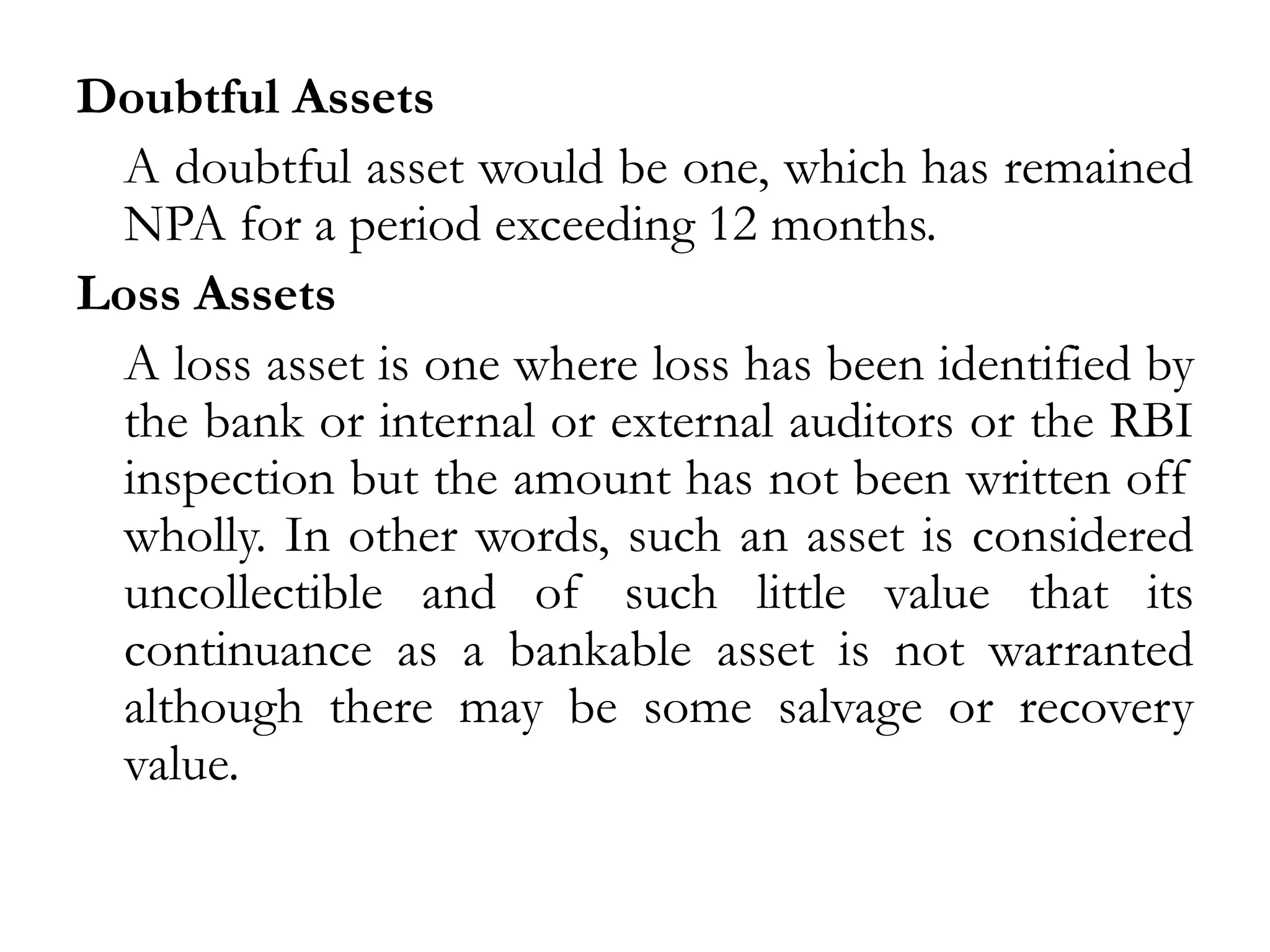

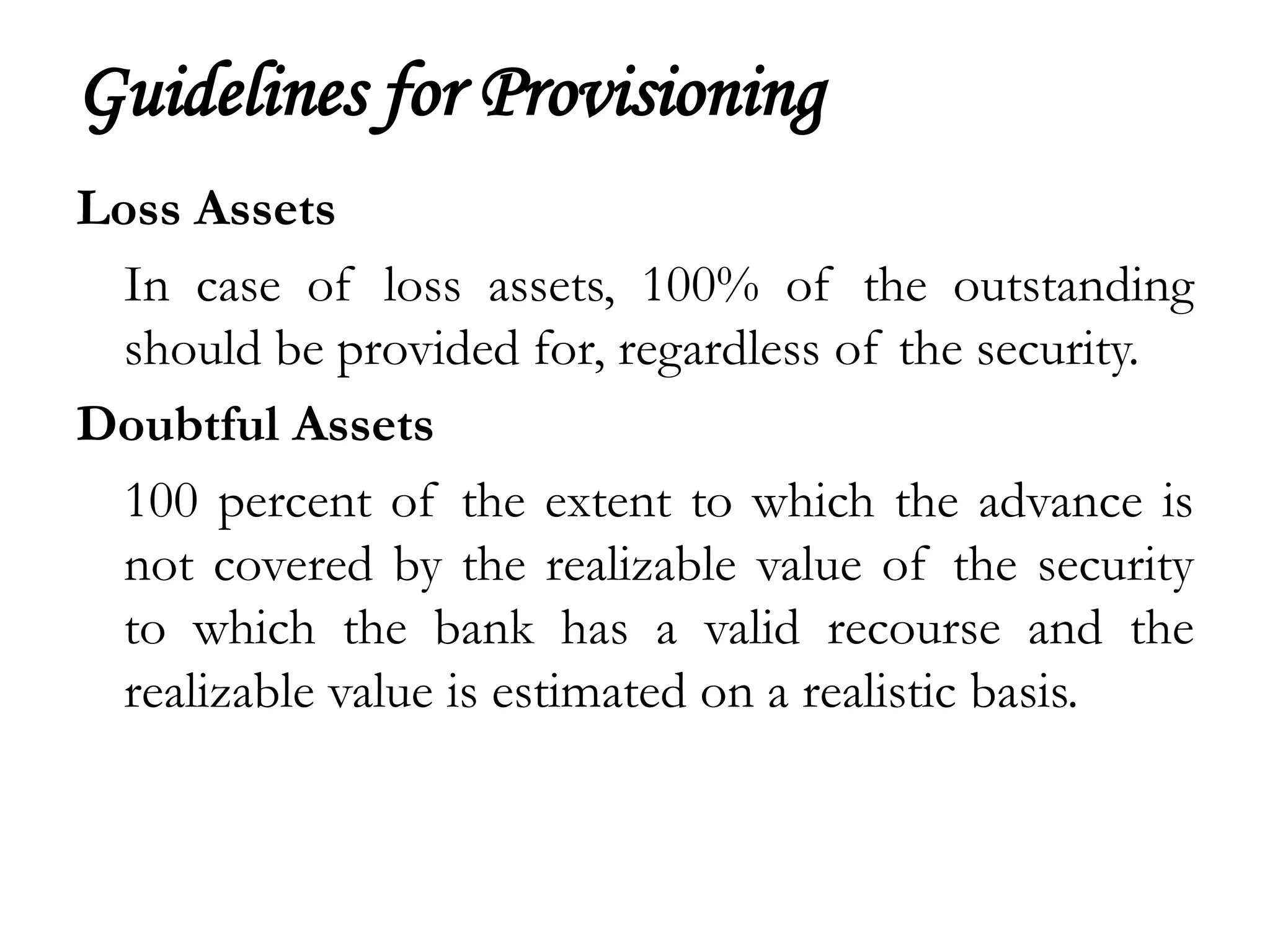

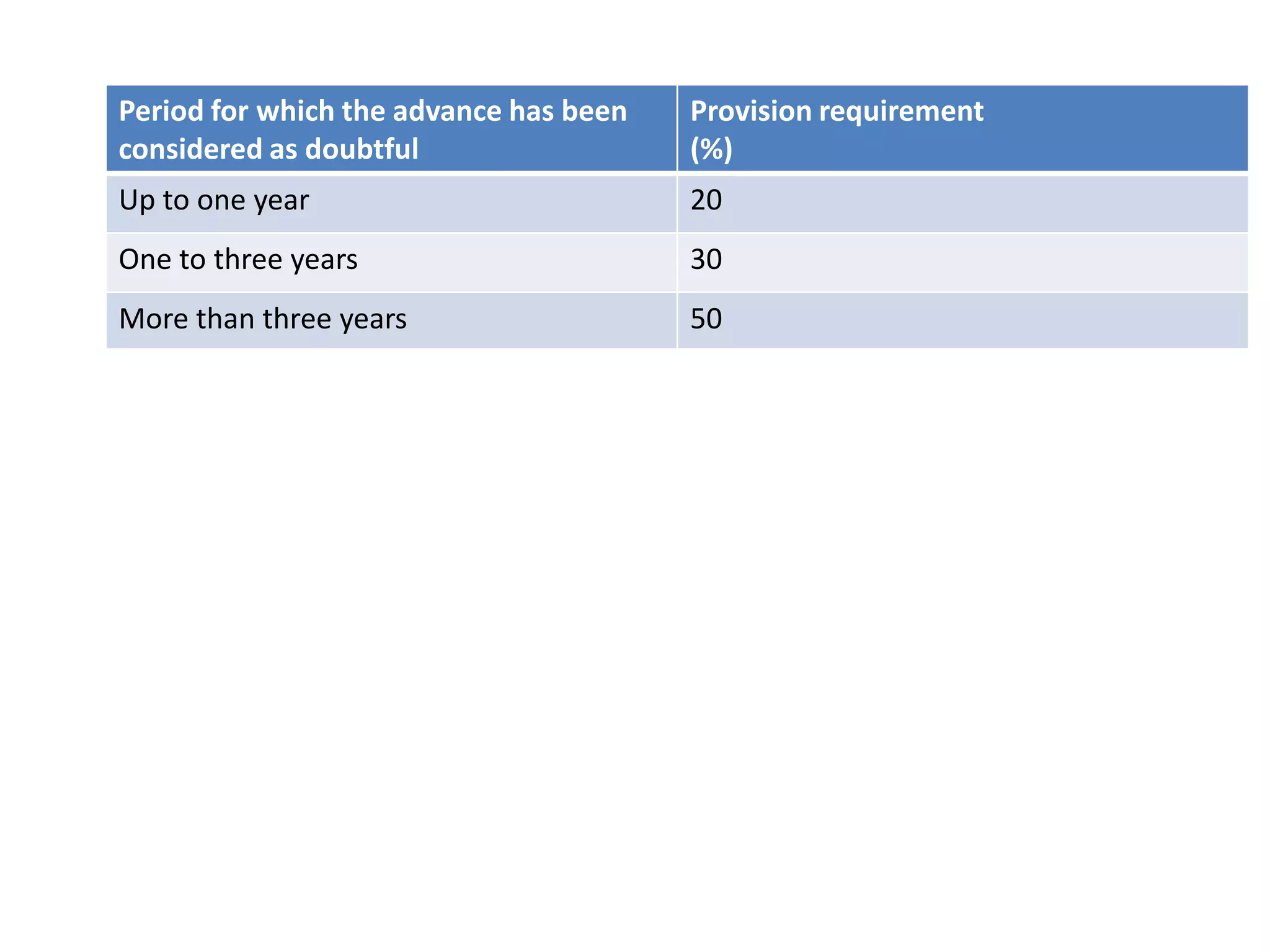

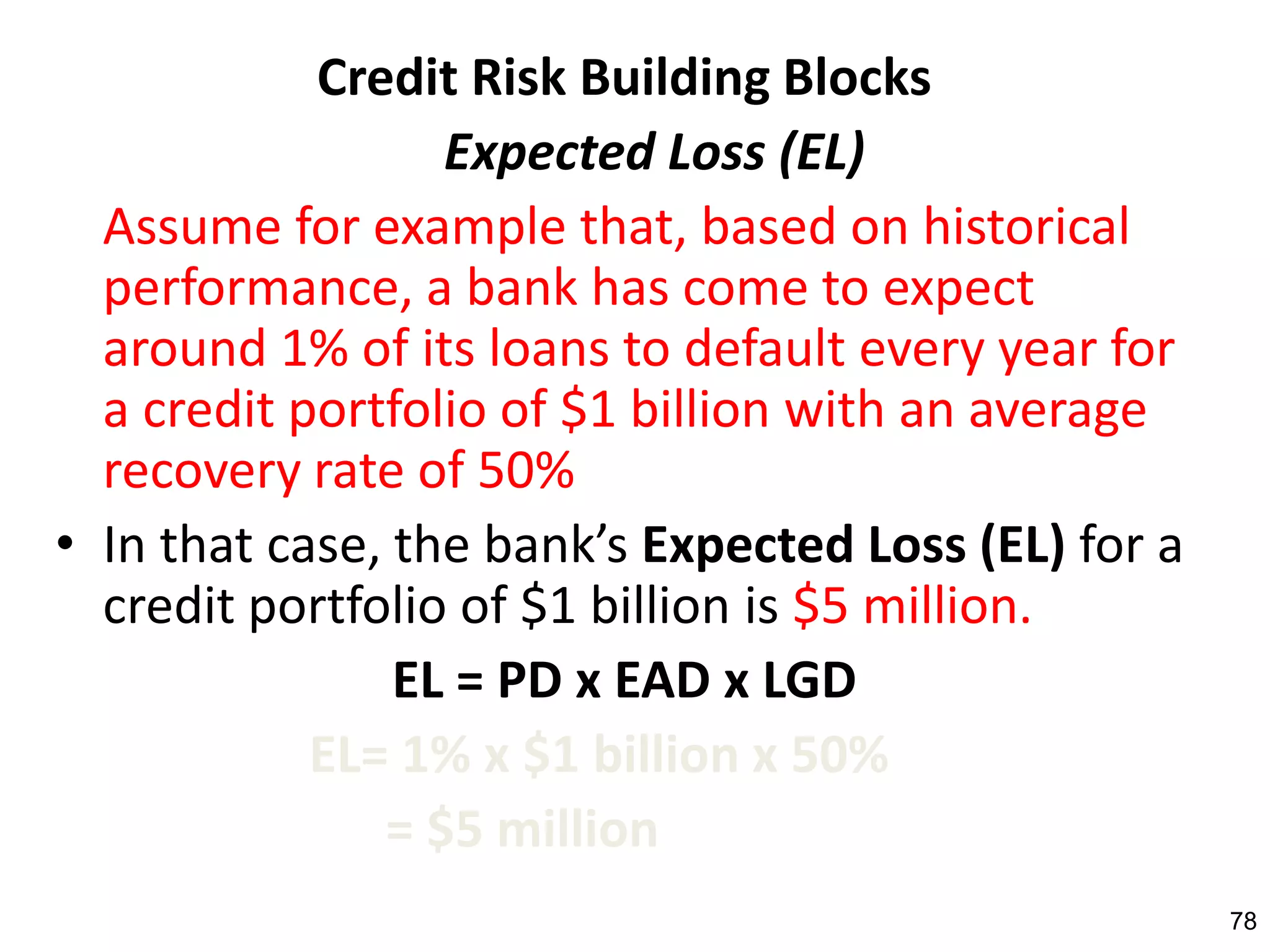

The document discusses guidelines related to management and classification of non-performing assets (NPAs) for banks. It defines what constitutes an NPA and provides classifications such as sub-standard, doubtful, and loss assets. It specifies timelines for classifying assets under each category and provisioning requirements ranging from 10-100% depending on the classification. The document also discusses income recognition policies for NPAs and outlines the broad components that should be included in an NPA management policy for banks.

![E banking by sanjeev kumar chaswal [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/e-bankingbysanjeevkumarchaswalcompatibilitymode-130122093515-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)