1. The document discusses different modes of lending used by banks to secure advances, including lien, pledge, mortgage, and hypothecation.

2. A lien allows a bank to retain possession of goods until debts are paid, while a pledge involves delivering goods to the bank.

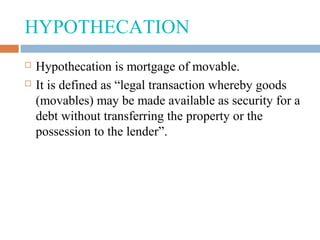

3. Mortgage transfers interest in specific immovable property, and hypothecation grants security over movable property without transferring possession.