The document describes a second-year internship focused on optimal stochastic control problems with financial applications, covering theoretical foundations, resolution methods using probabilistic and PDE approaches, and practical applications such as portfolio allocation and investment problems. It provides a detailed examination of concepts like the Bellman equation, dynamic programming principles, and relevant financial mathematics issues. The internship took place at the Lamsin research laboratory in Tunisia, highlighting its role in advancing research in financial mathematics.

![Definition

Bellman’s principle of optimality

” An optimal policy has the property that whatever the initial state and initial

decision are, the remaining decisions must constitute an optimal policy with

regard to the state resulting from the first decision”

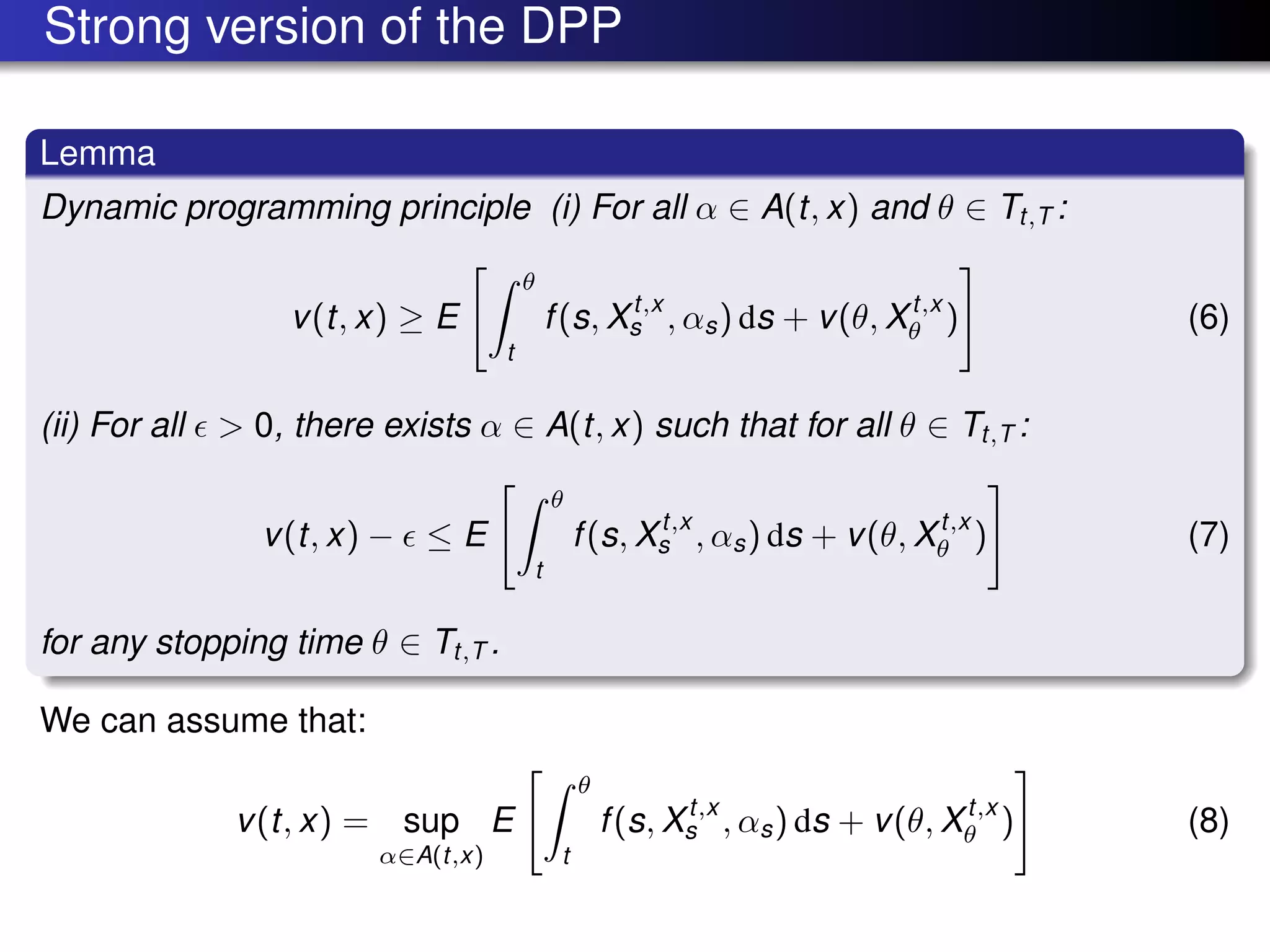

Mathematical formulation of the Bellman’s principle or Dynamic

Programming Principle (DPP)

The usual version of the DPP is written as

v(t, x) = sup

α∈A(t,x)

E

θ

t

f(s, Xt,x

s , αs) ds + v(θ, Xt,x

θ )

for any stopping time θ ∈ Tt,T (set of stopping times valued in [t, T]).](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-12-2048.jpg)

![Usual version of the DPP

(1) Finite horizon: let (t, x) ∈ [0, T] × Rn

. Then ∀ θ ∈ Tt,T

v(t, x) = sup

α∈A(t,x)

sup

θ∈Tt,T

E

θ

t

f(s, Xt,x

s , αs) ds + v(θ, Xt,x

θ ) (2)

= sup

α∈A(t,x)

inf

θ∈Tt,T

E

θ

t

f(s, Xt,x

s , αs) ds + v(θ, Xt,x

θ ) (3)

(2) Infinite horizon: let x ∈ [0, T]Rn

. Then ∀ θ ∈ Tt,T we have

v(t, x) = sup

α∈A(x)

sup

θ∈T

E

θ

0

e−βs

f(Xx

s , αs) dx + e−βs

v(Xx

θ ) (4)

= sup

α∈A(x)

inf

θ∈T

E

θ

0

e−βs

f(Xx

s , αs) dx + e−βθ

v(Xx

θ ) (5)](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-13-2048.jpg)

![Time and space descretization

Let Ω = [0, 1], ∆t = T

N , N ∈ N∗

, tk=0...N := k∆t, h step in space, tk = k∆t,

xj = jh. Ωh, Lα

, vk

j (x),bk

j ,ak,α

j approximate Ω, Lα

, b(tk , xj ), α, a(tk , xj , α)

Approximation of first

derivative:

∂v

∂x

(tk , xj ) :=

vk

j+1 − vk

j−1

2h1

(11)

∂v

∂x

(tk , xj ) :=

vk

j+1 − vk

j

h

(12)

or

∂v

∂x

(tk , xj ) :=

vk

j − vk

j−1

h

(13)

Approximation of second derivative

∂2

v

∂x2

(tk , xj ) :=

vk

j+1 − 2vk

j + vk

j−1

h2

(14)

Approximation of time derivative

∂v

∂t

(tk , xj ) :=

vk

j − vk−1

j

∆t

(15)

or

∂v

∂t

(tk , xj ) :=

vk+1

j − vk

j

∆t

(16)](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-30-2048.jpg)

![Time and space descretization

Let Ω = [0, 1], ∆t = T

N , N ∈ N∗

, tk=0...N := k∆t, h step in space, tk = k∆t,

xj = jh. Ωh, Lα

, vk

j (x),bk

j ,ak,α

j approximate Ω, Lα

, b(tk , xj ), α, a(tk , xj , α)

Approximation of first

derivative:

∂v

∂x

(tk , xj ) :=

vk

j+1 − vk

j−1

2h1

(11)

∂v

∂x

(tk , xj ) :=

vk

j+1 − vk

j

h

(12)

or

∂v

∂x

(tk , xj ) :=

vk

j − vk

j−1

h

(13)

Approximation of second derivative

∂2

v

∂x2

(tk , xj ) :=

vk

j+1 − 2vk

j + vk

j−1

h2

(14)

Approximation of time derivative

∂v

∂t

(tk , xj ) :=

vk

j − vk−1

j

∆t

(15)

or

∂v

∂t

(tk , xj ) :=

vk+1

j − vk

j

∆t

(16)](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-31-2048.jpg)

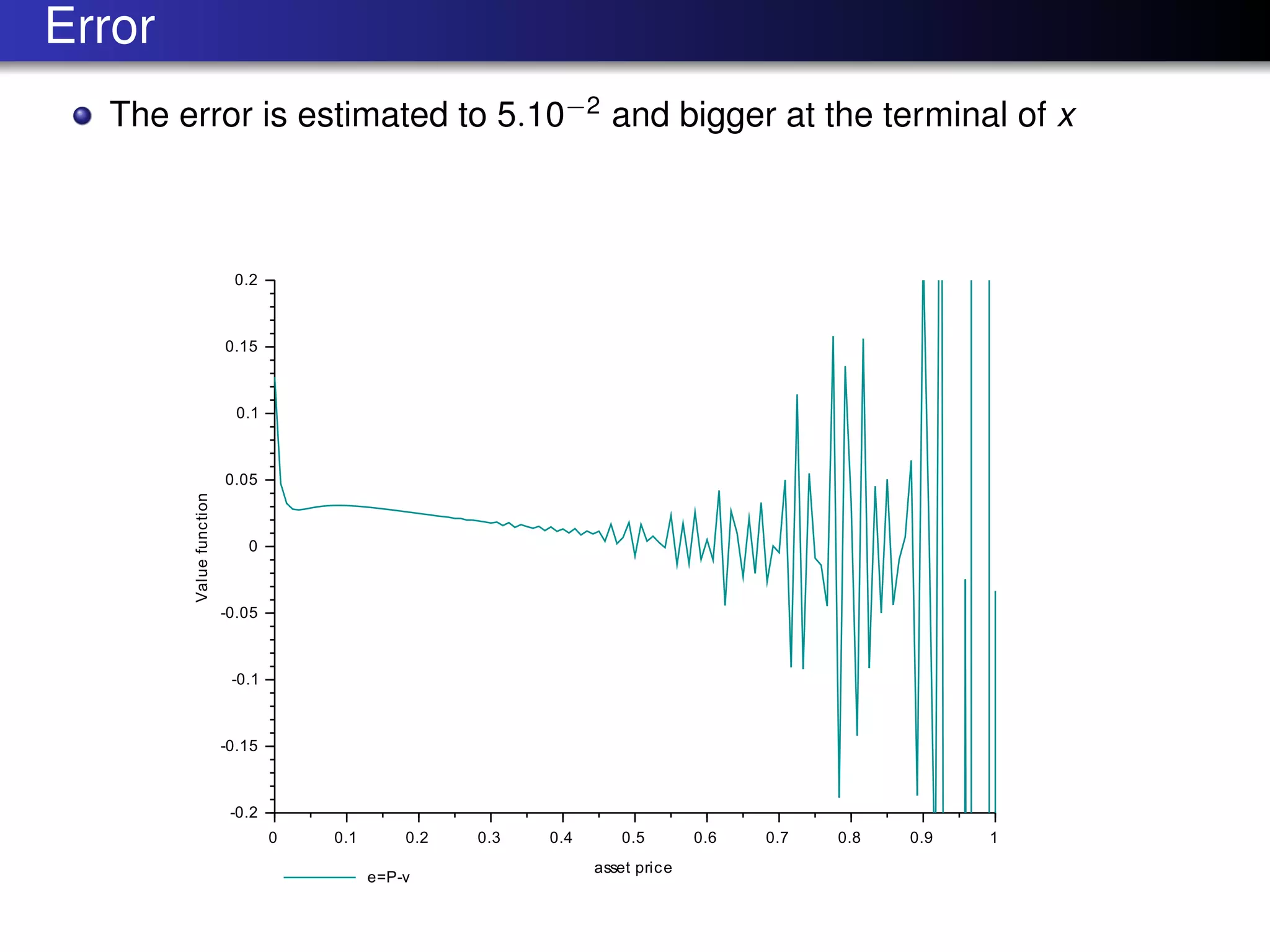

![Optimal stochastic problem theory

Resolution methods

Financial applications

Numerical results on C++ and Scilab

Probabilistic approach

Numerical/Deterministic approach with PDEs

Dirichlet boundary conditions: v = g in ∂Ω × [0, T[

Neumann boundary conditions:

∂v

∂x = g2 in Ω × [0, T[

In case f = 0 and g = xp

/p, p ∈]0, 1[

vN

j = gj =

x

p

j

p

and

vk

M −vk

M−1

h

= p

xM

vk

M = xp−1

M , k ∈ 0..N − 1, j ∈ 0..M

vk

M = vk

M−1

vk

M = 0, and vk

0 = 0

NB: In portfolio allocation problem − > Black and Scholes-Merton Problem of

stocks:

dSt = µdt + σdWt ,

dS0 = rS0dt

32 / 74](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-32-2048.jpg)

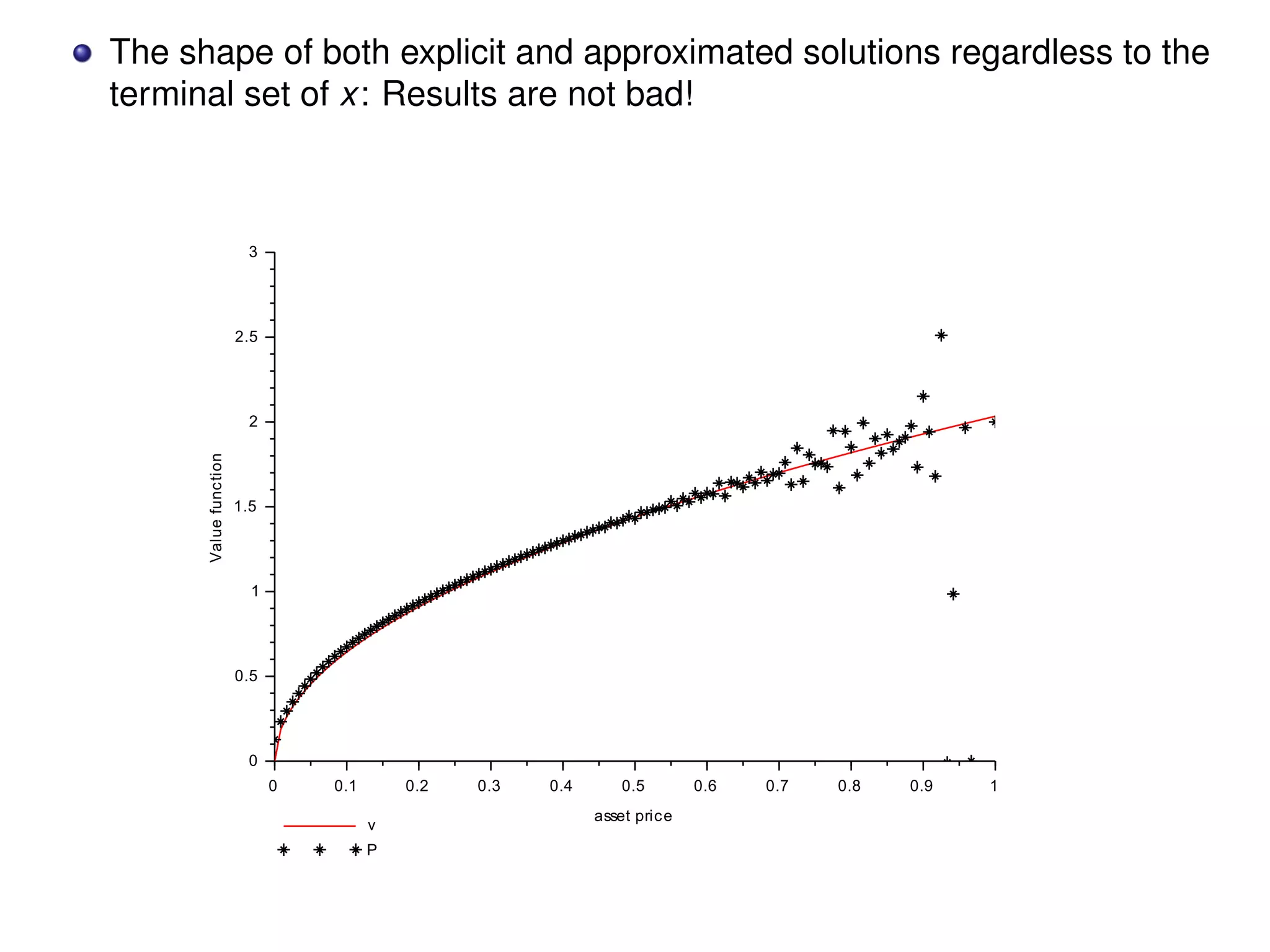

![Applications 1: Merton portfolio allocation problem in

finite horizon

An agent invests at any time t a proportion αt of his wealth X in a stock of

price S and 1 − αt in a bond of price S0

with interest rate r.

The dynamics of the controlled wealth process is:

dXt =

Xt αt

St

dSt +

Xt (1 − αt )

S0

t

dS0

t

”Utility maximization problem at a finite horizon T ”:

v(t, x) = sup

α∈A

E U Xt,x

T , ∀ (t, x) ∈ [0, T] × (0, ∞) .

HJB eqaution for Merton’s problem

vt + rxvx + sup

a∈A

a (µ − r) xvx +

1

2

x2

a2

σ2

vxx = 0 (17)

v(T, x) = U(x) (18)](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-35-2048.jpg)

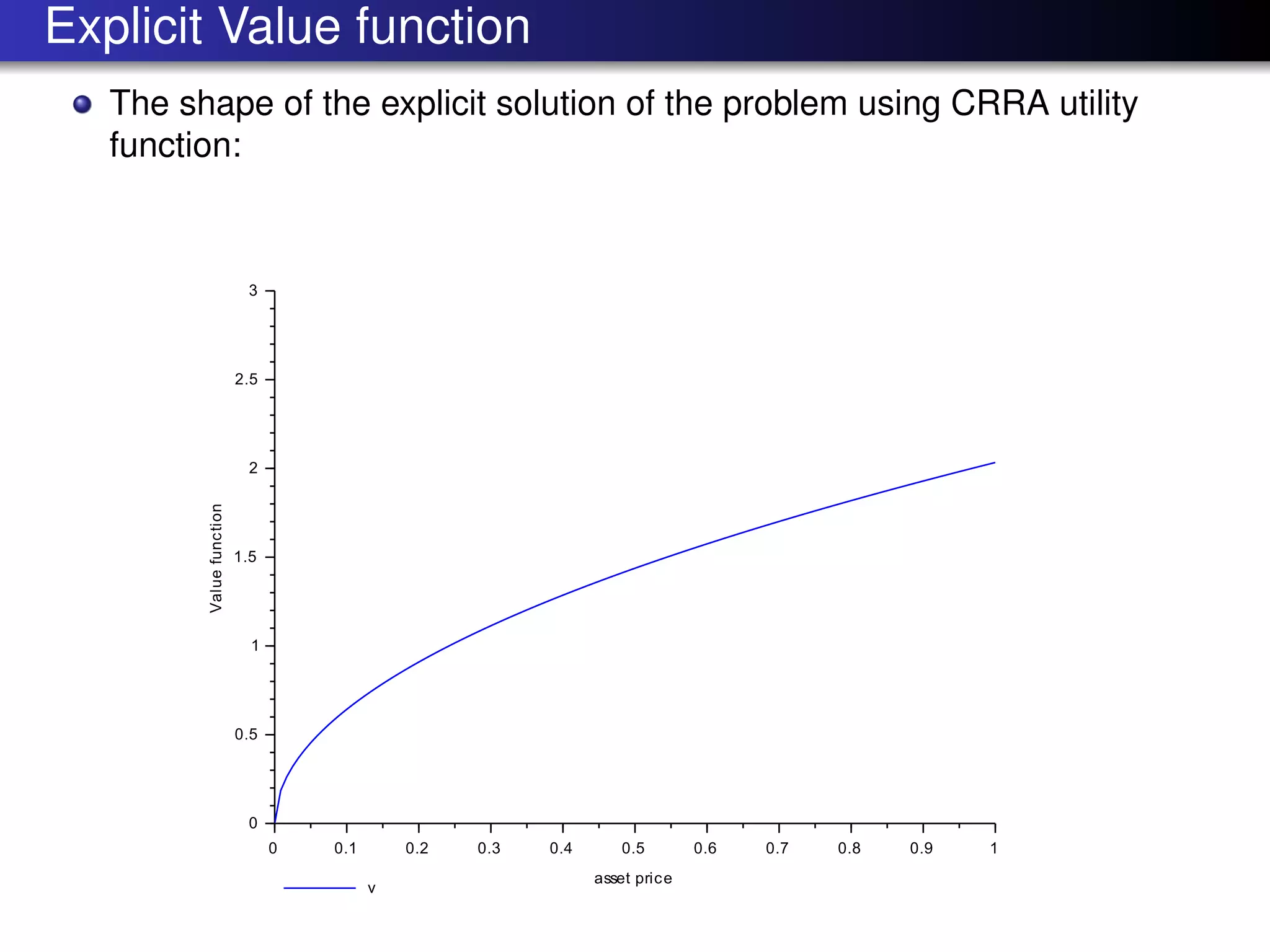

![Utility function

U is C1

, strictly increasing and concave on (0, ∞), and satisies the Inada

conditions:

U (0) = ∞ U (∞) = 0 :

Convex conjugate of U:

ˆU(y) := sup

x>0

[U(x) − xy]

We use the CRRA utility function:

U(x) =

xp

p

, p 1, p 0

Relative Risk Aversion RRA: −xU”

(x)/U (x) = 1 − p.

→ if the person experiences an increase in wealth, he/she will choose to

increase (or keep unchanged, or decrease) the fraction of the portfolio

held in the risky asset if relative risk aversion is decreasing (or constant, or

increasing).](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-36-2048.jpg)

![Investment/consumption problem on infinite horizon

The SDE governing the wealth process

dXt = Xt (αt µ + (1 − αt )r − ct )dt + Xt αt αt dWt ,

The goal is to maximize over strategies (α, c) the expected utility from

intertemporal consumption up to a random time horizon τ:

v(x) = sup

(α,c)∈A×C

E

τ

0

e−βt

u(ct Xx

t ) dt .

τ is independent of F∞, denote by F(t) = P[τ ≤ t] = P[τ ≤ t|F∞] the

distribution function of τ.

Assume an exponential distribution for the random time horizon:

1 − F(t) = exp−λt

for some positive constant λ.

Infinite horizon problem:

v(x) = sup

(α,c)∈A×C

E

∞

0

e−(β+λ)t

u(ct Xx

t ) dt](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-38-2048.jpg)

![The HJB equation associated is

ˆβv(x) − sup

a∈A,c≥0

[La,c

v(x) + u(cx)] = 0, x ≥ 0, (19)

where La,c

v(x) = x(aµ + (1 − a)r − c)v + 1

2 x2

a2

σ2

v

Explicit solution

The discount factor β shall satisfy: β > ρ − λ

v(x) = Ku(x) solves the HJB equation where

K =

1 − p

β + λ − ρ

1−p

and ρ =

(µ − r)2

2σ2

p

1 − p

+ rp

The optimal controls are constant given by (ˆa, ˆc)

ˆa = arg max

a∈A

[a(µ − r) + r −

1

2

a2

(1 − p)σ2

]

ˆc =

1

x

(v (x))

1

p−1 .](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-39-2048.jpg)

![The HJB equation associated is

ˆβv(x) − sup

a∈A,c≥0

[La,c

v(x) + u(cx)] = 0, x ≥ 0, (19)

where La,c

v(x) = x(aµ + (1 − a)r − c)v + 1

2 x2

a2

σ2

v

Explicit solution

The discount factor β shall satisfy: β > ρ − λ

v(x) = Ku(x) solves the HJB equation where

K =

1 − p

β + λ − ρ

1−p

and ρ =

(µ − r)2

2σ2

p

1 − p

+ rp

The optimal controls are constant given by (ˆa, ˆc)

ˆa = arg max

a∈A

[a(µ − r) + r −

1

2

a2

(1 − p)σ2

]

ˆc =

1

x

(v (x))

1

p−1 .](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-40-2048.jpg)

![The HJB equation associated is

ˆβv(x) − sup

a∈A,c≥0

[La,c

v(x) + u(cx)] = 0, x ≥ 0, (19)

where La,c

v(x) = x(aµ + (1 − a)r − c)v + 1

2 x2

a2

σ2

v

Explicit solution

The discount factor β shall satisfy: β > ρ − λ

v(x) = Ku(x) solves the HJB equation where

K =

1 − p

β + λ − ρ

1−p

and ρ =

(µ − r)2

2σ2

p

1 − p

+ rp

The optimal controls are constant given by (ˆa, ˆc)

ˆa = arg max

a∈A

[a(µ − r) + r −

1

2

a2

(1 − p)σ2

]

ˆc =

1

x

(v (x))

1

p−1 .](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-41-2048.jpg)

![The HJB equation associated is

ˆβv(x) − sup

a∈A,c≥0

[La,c

v(x) + u(cx)] = 0, x ≥ 0, (19)

where La,c

v(x) = x(aµ + (1 − a)r − c)v + 1

2 x2

a2

σ2

v

Explicit solution

The discount factor β shall satisfy: β > ρ − λ

v(x) = Ku(x) solves the HJB equation where

K =

1 − p

β + λ − ρ

1−p

and ρ =

(µ − r)2

2σ2

p

1 − p

+ rp

The optimal controls are constant given by (ˆa, ˆc)

ˆa = arg max

a∈A

[a(µ − r) + r −

1

2

a2

(1 − p)σ2

]

ˆc =

1

x

(v (x))

1

p−1 .](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-42-2048.jpg)

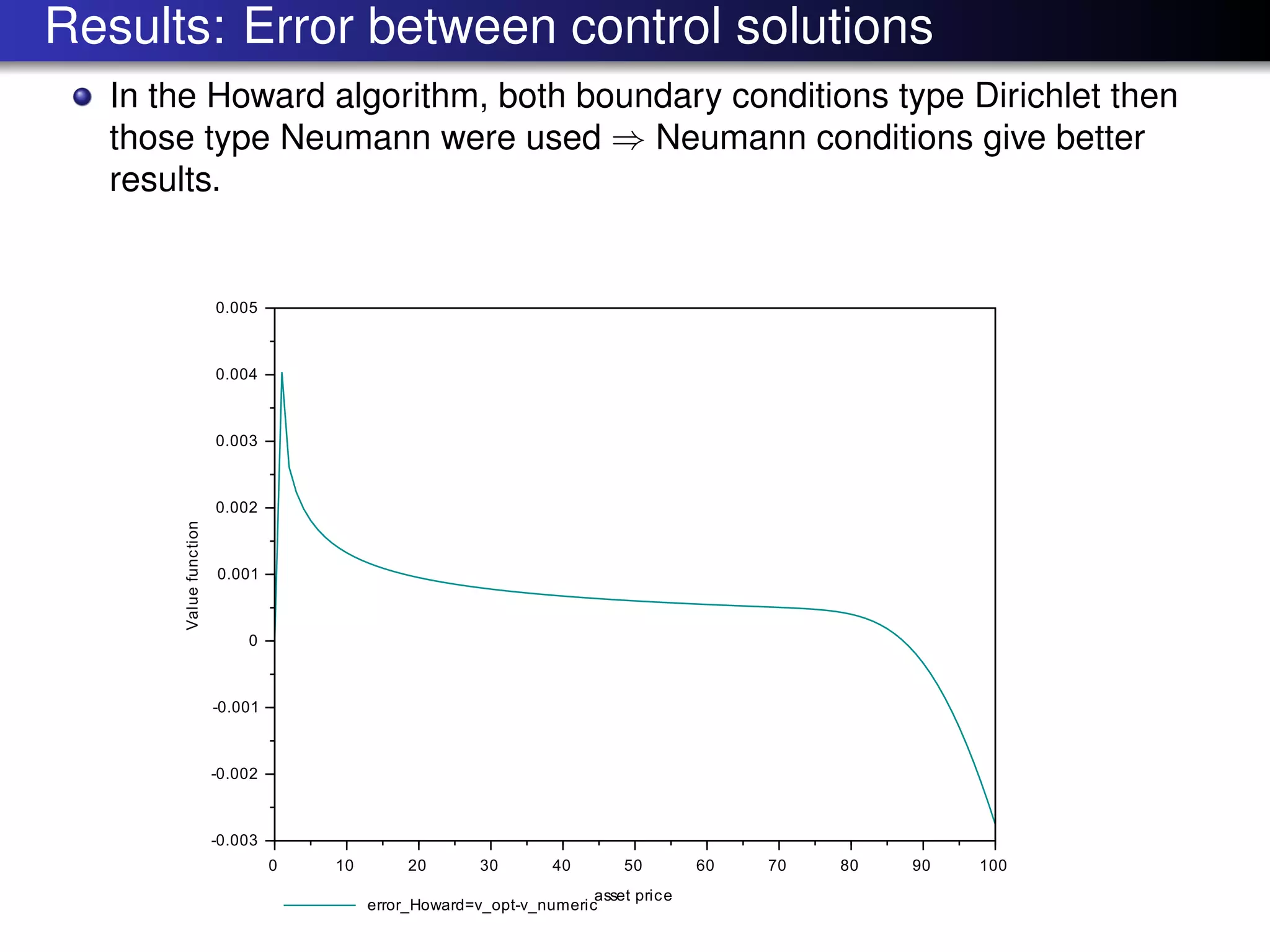

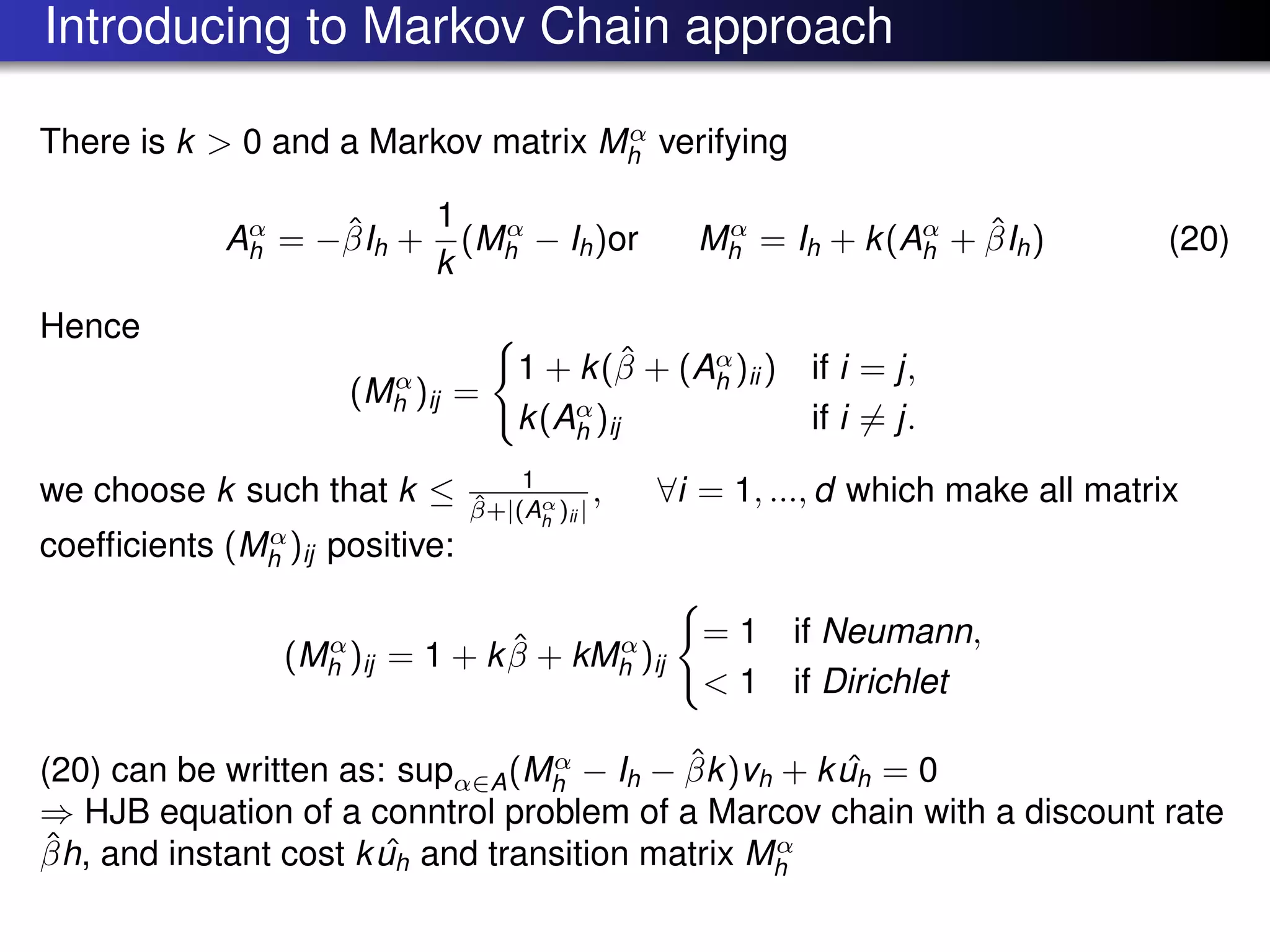

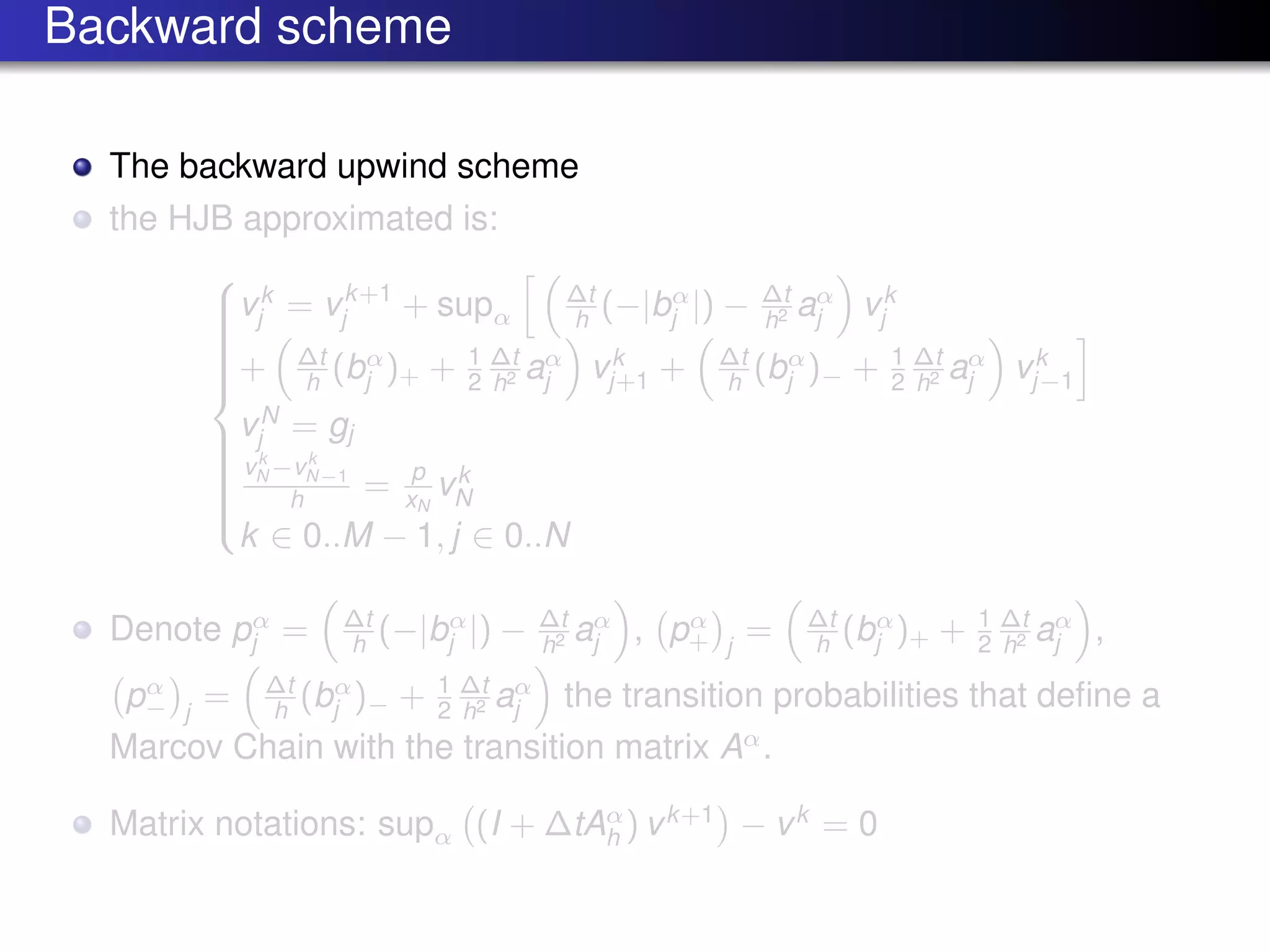

![Why Markov Chain approach?

solving the descritized system requires some conditions on the matrix A

of the differential operator Lα

Case where A is not defined positive, we can obtain a descretization

system such satisfy the ” Discrete Maximum principle ”

Under specific condition on the space step of discretization h we get a

convergent Markov Chain. [page 89 A. SULEM, J-P. PHILIPPE, M´ethode

num´erique en contr ole stochastique]

The convergence of the scheme can be found and explained using

standard arguments provided by D. Kushner [Numerical Methods for

Stochastic Control Problems in Continuous Time.

NB Depending on the sign of the drift b of Xt , we use the right-hand-side

scheme upwind when b is positive and the left-hand-side upwind

scheme when b is negative to obtain a sort of transition probabilities

(∈ [0, 1] )](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-43-2048.jpg)

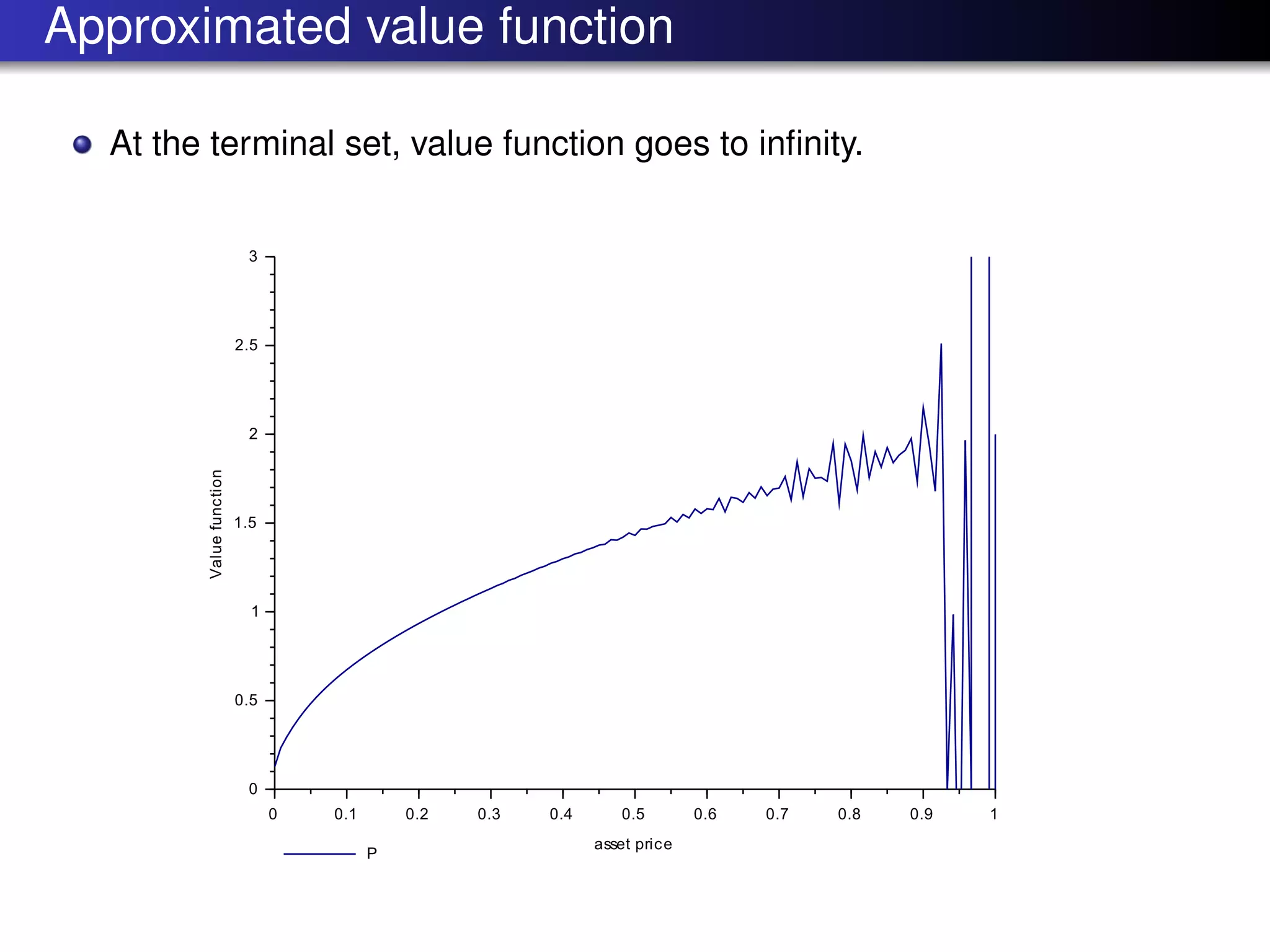

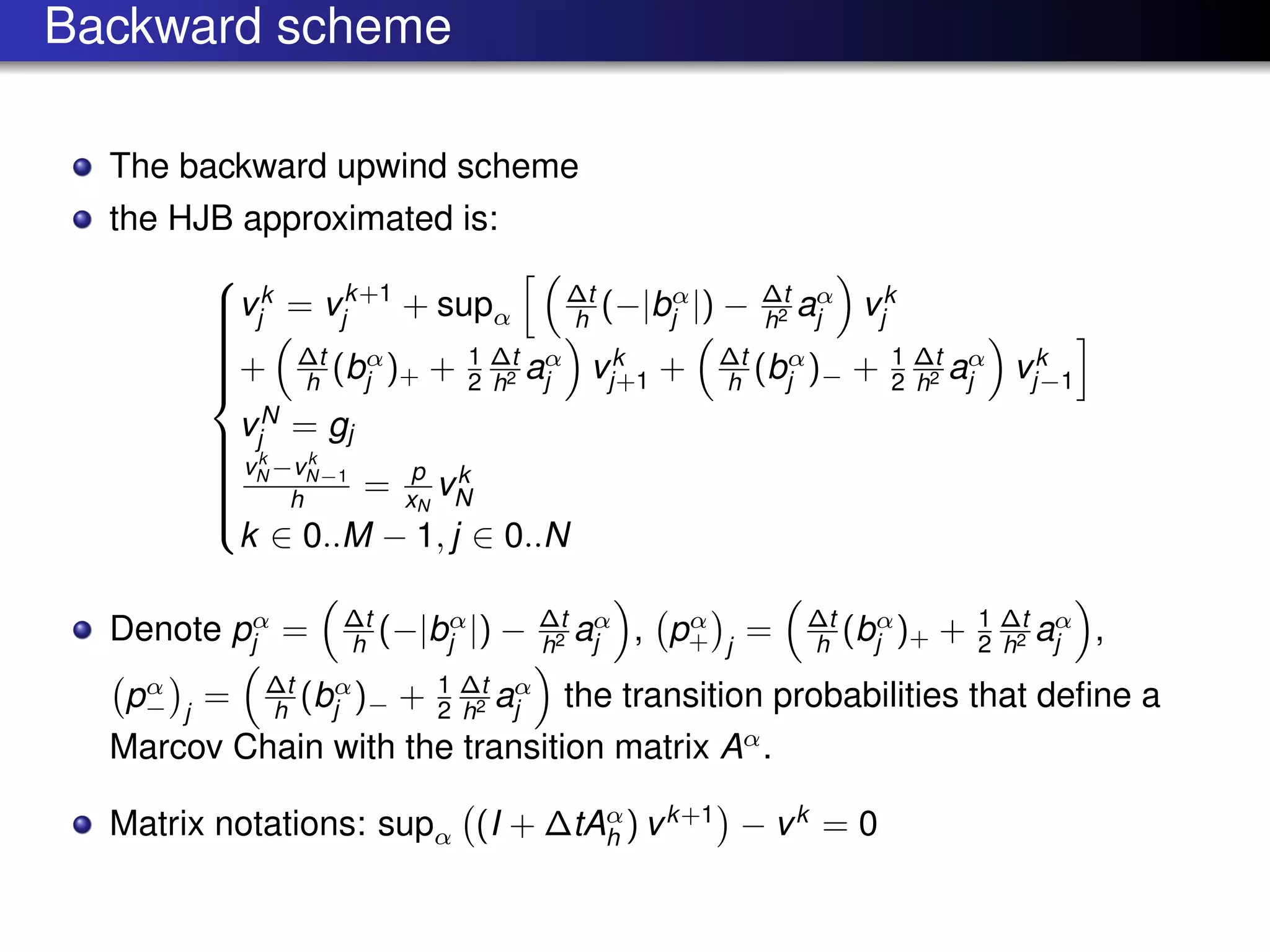

![Approximated scheme

Approximated scheme: two different scheme were used.

The forward upwind scheme

the HJB approximated is:

vk−1

j = supα 1 − ∆t

h |bk,α

j | − ∆t

h2 ak,α

j vk

j +

∆t

h (bk,α

j )+ + 1

2

∆t

h2 ak,α

j vk

j+1 + ∆t

h (bk,α

j )− + 1

2

∆t

h2 ak,α

j vk

j−1

vN

j = gj

Denote

pα

j = p(xj , xj |α), pα

+ j

= p(xj , xj+1|α), pα

− j

= p(xj , xj−1|α)

the transition probabilities that define the transition matrix Aα

.

Matrix notations: vk−1

= supα (I − ∆tAα

) vk

Explicit solution is given in [1]:](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-45-2048.jpg)

![Approximated scheme

Approximated scheme: two different scheme were used.

The forward upwind scheme

the HJB approximated is:

vk−1

j = supα 1 − ∆t

h |bk,α

j | − ∆t

h2 ak,α

j vk

j +

∆t

h (bk,α

j )+ + 1

2

∆t

h2 ak,α

j vk

j+1 + ∆t

h (bk,α

j )− + 1

2

∆t

h2 ak,α

j vk

j−1

vN

j = gj

Denote

pα

j = p(xj , xj |α), pα

+ j

= p(xj , xj+1|α), pα

− j

= p(xj , xj−1|α)

the transition probabilities that define the transition matrix Aα

.

Matrix notations: vk−1

= supα (I − ∆tAα

) vk

Explicit solution is given in [1]:](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-46-2048.jpg)

![Algorithm C++

Algorithm of the forward scheme

Initialization: ∀j in 0, ..., M, vN

j =

√

xj

Repeat for all k from N − 1 to 0 do

vk

0 = 0

calculate vk

j ∈ h := v(tk , xj ) = supαi

w(tk , xj , αi )

Repeat for all j in 1, ..., M − 1,

for each αi in [ˆα − , ˆα + ] do

calculate (bαi

j )+ and (bαi

j )−

solve

vk

j = supαi

1 − ∆t

h |bαi

j | − ∆t

h2 aαi

j vk+1

j +

∆t

h (bαi

j )+ + 1

2

∆t

h2 aαi

j vk+1

j+1 + ∆t

h (bαi

j )− + 1

2

∆t

h2 aαi

j vk+1

j−1

vN

j = vN−1

j](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-47-2048.jpg)

![Algorithm C++

Algorithm of the forward scheme

Initialization: ∀j in 0, ..., M, vN

j =

√

xj

Repeat for all k from N − 1 to 0 do

vk

0 = 0

calculate vk

j ∈ h := v(tk , xj ) = supαi

w(tk , xj , αi )

Repeat for all j in 1, ..., M − 1,

for each αi in [ˆα − , ˆα + ] do

calculate (bαi

j )+ and (bαi

j )−

solve

vk

j = supαi

1 − ∆t

h |bαi

j | − ∆t

h2 aαi

j vk+1

j +

∆t

h (bαi

j )+ + 1

2

∆t

h2 aαi

j vk+1

j+1 + ∆t

h (bαi

j )− + 1

2

∆t

h2 aαi

j vk+1

j−1

vN

j = vN−1

j](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-48-2048.jpg)

![Algorithm in Scilab

Algorithm of the Howard

sets up the Howard algorithm[3] [7] that allows us to solve

minα∈A (B (α) x − b). B (α) is defined as B(α)ij = B(αi )ij = (I + δtA(αi ))ij

1. Initialize α0

in A.

2. Iterate for k ≥ 0 :

(i) find xk

∈ N

solution of B(α)xk

= b.

(ii) αk+1

:= argminα∈An B(α)xk

− b .

3. k=k+1

Note that at each iteration, we have to find the control value of α](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-56-2048.jpg)

![Algorithm in Scilab

Algorithm of the Howard

sets up the Howard algorithm[3] [7] that allows us to solve

minα∈A (B (α) x − b). B (α) is defined as B(α)ij = B(αi )ij = (I + δtA(αi ))ij

1. Initialize α0

in A.

2. Iterate for k ≥ 0 :

(i) find xk

∈ N

solution of B(α)xk

= b.

(ii) αk+1

:= argminα∈An B(α)xk

− b .

3. k=k+1

Note that at each iteration, we have to find the control value of α](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-57-2048.jpg)

![Algorithm in Scilab

Algorithm of the Howard

sets up the Howard algorithm[3] [7] that allows us to solve

minα∈A (B (α) x − b). B (α) is defined as B(α)ij = B(αi )ij = (I + δtA(αi ))ij

1. Initialize α0

in A.

2. Iterate for k ≥ 0 :

(i) find xk

∈ N

solution of B(α)xk

= b.

(ii) αk+1

:= argminα∈An B(α)xk

− b .

3. k=k+1

Note that at each iteration, we have to find the control value of α](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-58-2048.jpg)

![Algorithm in Scilab

Algorithm of the Howard

sets up the Howard algorithm[3] [7] that allows us to solve

minα∈A (B (α) x − b). B (α) is defined as B(α)ij = B(αi )ij = (I + δtA(αi ))ij

1. Initialize α0

in A.

2. Iterate for k ≥ 0 :

(i) find xk

∈ N

solution of B(α)xk

= b.

(ii) αk+1

:= argminα∈An B(α)xk

− b .

3. k=k+1

Note that at each iteration, we have to find the control value of α](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-59-2048.jpg)

![Algorithm in Scilab

Algorithm of the Howard

sets up the Howard algorithm[3] [7] that allows us to solve

minα∈A (B (α) x − b). B (α) is defined as B(α)ij = B(αi )ij = (I + δtA(αi ))ij

1. Initialize α0

in A.

2. Iterate for k ≥ 0 :

(i) find xk

∈ N

solution of B(α)xk

= b.

(ii) αk+1

:= argminα∈An B(α)xk

− b .

3. k=k+1

Note that at each iteration, we have to find the control value of α](https://image.slidesharecdn.com/presentation-161117120736/75/Presentation-on-stochastic-control-problem-with-financial-applications-Merton-portfolio-problem-60-2048.jpg)