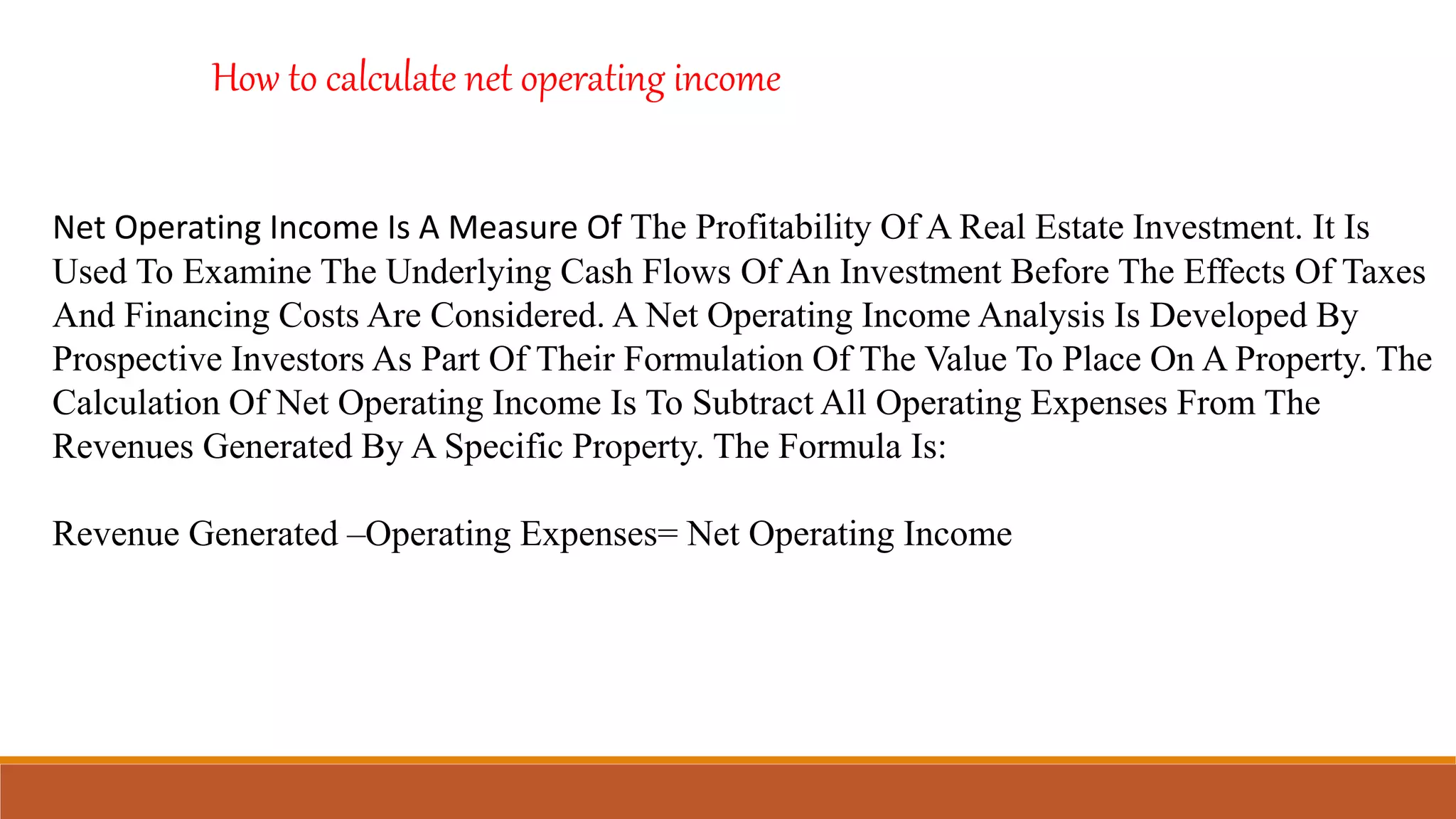

The Net Operating Income approach is a capital structure theory that suggests the total value of a firm is independent of the firm's capital structure or use of financial leverage. According to this approach, the market value of a firm depends only on the firm's operating income and business risk, not on financial leverage. While financial leverage can impact distributions to debt holders and equity holders, it cannot impact the firm's operating income or total value. The Net Operating Income is a measure of real estate profitability calculated by subtracting operating expenses from revenues to examine underlying cash flows before taxes and financing costs.