This document provides an overview of brand accounting including:

- The meaning and elements of brands as well as home-grown brands.

- The identification of brands as strategic assets and the objectives/purposes of brand accounting such as real economic value and future profitability.

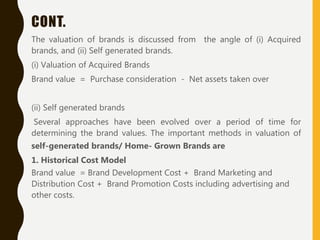

- The valuation approaches for acquired and self-generated brands which include historical cost, replacement cost, market price, and income approaches. Factors affecting valuation and difficulties in brand accounting are also discussed.

- Numerical examples are provided to illustrate the calculation of brand value using different approaches such as replacement cost and income approach.