Downloaded 29 times

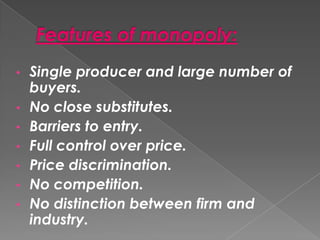

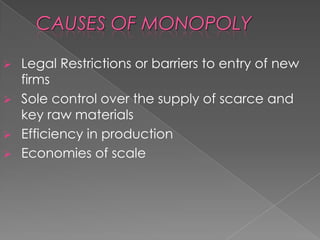

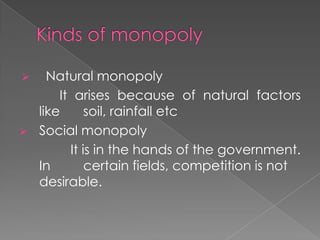

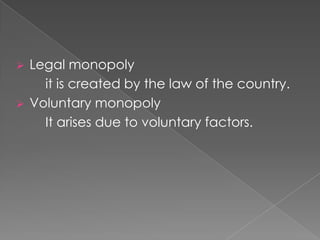

This document defines and explains the concept of monopoly. It states that a monopoly is a market situation where there is only one seller of a unique product or service, there are no close substitutes for this product or service, and there are barriers to entry that prevent other companies from entering the market. It also discusses how monopolies can control price and determine output to maximize their profits in both the short run and long run.