What is PureMonopoly

A pure monopoly is an industry in

which there is only one supplier of a

product for which there are no close

substitutes and in which it is very

difficult or impossible for another firm

to coexist.

4.

The Monopoly MarketStructure

▶ What is a monopoly exactly?

▶ A monopoly is a market structure characterized by:

▶ A single seller

▶ A unique product

▶ Impossible entry into the market

▶ Under a monopoly, the consumer has only one

choice.

Thus, they can either buy from the producer

or not consume

▶ There are no close substitutes.

5.

A Single Seller

▶One single firm IS the industry.

▶ Local monopolies are more

commonly observed in the real-world

than national monopolies.

6.

Unique Products

▶ Whydo Monopolists have unique

products?

▶ Absence of close substitutes

7.

Impossible Entry

▶ Barriersto Entry are high

▶ Barriers to entry are attributes of a market that make it

more difficult or expensive for a new firm to open for

business than it was for the firms already present in that

market.

8.

Barriers

1. Legal restrictions:

TheU.S. Postal Service

has a monopoly position

for some of its services

because Congress has

given to it one.

2. Patents: Some firms

benefit from a special,

but important, class of

legal impediments to

entry called patents.

4. Deliberately Erected

Entry Barriers A firm may

deliberately attempt to

make entry into the

industry difficult for others.

3. Control of a Scarce

Resource or Input If a

certain commodity can be

produced only by using a

rare input, a company that

gains control of the source of

that input can establish a

monopoly position for itself.

6. Technical Superiority A

firm whose technological

expertise vastly exceeds

that of any potential

competitor can, for a period

of time, maintain a

monopoly position. For

example, IBM Corporation

for many years had little

competition in the computer

business mainly because of

its technological virtuosity.

5. Large Sunk Costs

Entry into an industry

will, obviously, be very

risky if it requires a large

investment, especially if

that investment is sunk-

meaning that it cannot be

recouped for a

considerable period of

time, if at all.

7. Economies of Scale If

mere size gives a large

firm a cost advantage

over a smaller rival, it is

likely to be impossible for

anyone to compete with

the largest firm in the

industry.

9.

SOURCES OF MONOPOLY

Economiesof Scale

The cost to distribute 4

million kilowatt hours of

electric power

5 cents a kilowatt-hour with

one seller in the market,

or . . .

10 cents a kilowatt-hour with

two sellers, or . . .

15 cents a kilowatt-hour with

four sellers.

Because of economies of scale,

one seller can meet the market

demand at a lower average cost

than two or more sellers.

10.

Price and OutputDecisions for a

Monopolist

▶ The demand curve for a monopolist differs from

the competitive firm because the monopolist is a

price maker not taker.

▶ Def: A price maker is a firm that faces a downward

sloping demand curve.

11.

More Demand andsome Marginal Revenue

▶ Demand and Marginal Revenue

▶ They are both negatively-sloped

▶ Demand

▶ Market demand is negatively-sloped. The monopolist

faces a tradeoff between price and quantity sold.

▶ To obtain a higher price, the monopolist must lower

quantity

. Or, if it wants to sell a larger quantity

, it

must lower price.

12.

MONOPOLY EQUILIBRIUM

▶ Demandand Marginal Revenue

▶ Marginal revenue is less than price

☐ The marginal revenue curve is negatively-sloped

but lies below the demand curve at each

quantity: MR<P at all Q.

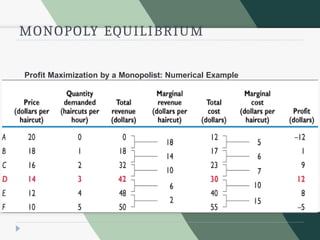

MONOPOLY EQUILIBRIUM

The diagramshows the monopolist’s

Average total cost (ATC), marginal cost

(MC), demand (D),

and marginal revenue (MR).

Profit Maximization by a Monopolist

The monopolist maximizes profits or

minimizes losses by producing the

quantity at which marginal revenue

equals marginal cost.

MONOPOLY EQUILIBRIUM

▶ Short-Runand Long-Run Equilibrium

▶ When a monopolist incurs short-run losses

▶ However, if a monopolist incurs economic

losses in the short- run, it exits the market

in the long-run. The long-run equilibrium

quantity is zero.

Price Discrimination

▶ Themonopolist may charge different prices

to consumers to maximize profits.

▶ Def: Price discrimination occurs when a seller charges

different prices for the same product that are not justified

by cost differences.

▶ Selling a good or service at a number of different prices

where the price differences do not reflect differences in cost but

instead reflect differences in consumers’ price elasticities of

demand.

▶ However, specific conditions must be met before

the seller can act in this way.

26.

Conditions for PriceDiscrimination

▶ The seller must be a price maker and therefore face

a downward-sloping demand curve

▶ The seller must be able to segment the market

distinguishing between consumers willing to pay

different prices

▶ It must be impossible or too costly for customers

to engage in arbitrage

27.

How can aproducer price discriminate

▶ Discriminating among groups of

consumers

▶ Different prices for consumers with different elasticities. The market

is segmented based on some easily distinguished characteristic of

consumers—age, for example.

▶ Discriminating among units of a good

▶ The seller charges the same prices to all consumers but

offers each consumer a lower price for a larger number of

units bought—volume discounts, for example.

28.

Price Discrimination withTwo Groups of Consumers

D

(a)

LRAC, MC

0 400 Quantity per period 0 500 Quantity per period

A monopolist facing two groups of consumers with different demand elasticities may

be able to practice price discrimination to increase profit or reduce loss. With marginal

cost the same in both markets, the firm charges a higher price to the group in panel (a),

which has a less elastic demand than group in panel (b).

(b)

Dollars

per

unit

$3.00

1.00

LRAC, MC

MR Dollars

per

unit

$1.50

1.00

D’

MR’

29.

Is Price DiscriminationUnfair

▶ There is nothing evil or illegal about economic

price discrimination. It simply means charging

different prices for the same good or service

unrelated to differences in cost.

▶ Price discrimination is common in all markets

other than perfectly competitive markets.

30.

Is Price DiscriminationUnfair

▶ What are its effects:

▶ Increase seller’s profit, at least in the short run

▶ Enhance economic efficiency

▶ Conserve on scarce resources.

▶ Many buyers benefit because they are now paying a

lower price

▶ Example: Movie Theatres- senior citizen and college

students discounts

31.

How does itincrease the sellers profits

▶ Increases seller’s profits

▶ By observing different elasticities for the

consumers the following can happen

▶ Reduce the price for buyers with elastic demand

will increase TR

▶ Increase the price for buyers with inelastic

demand will increase TR

▶ When the total quantity is not changing, then

costs are not changing, but revenues are

profits are HIGHER

32.

What about efficiency

▶Enhances economic efficiency

▶ We know that under a monopoly the output is under-

produced. But price discrimination can fix this

underproduction of the good

▶ A price-discriminating monopolist is able to sell a larger

quantity than a single-price monopolist by reducing price

only on the additional units sold, not on all units sold.

▶ Because the problem with monopoly is underproduction,

increasing quantity enhances efficiency

. The sum of

producer and consumer surplus is higher in a monopoly

market with price discrimination than in a market with a

single-price monopolist.

33.

MONOPOLY AND COMPETITION

Themarket demand curve is D.

The market supply curve is S.

The competitive market

equilibrium is where quantity

demanded equals quantity

supplied.

The competitive equilibrium

quantity is QC and the

equilibrium price is PC.

Competitive Equilibrium

34.

MONOPOLY AND COMPETITION

Thecompetitive market

supply curve, S, is the

monopolist’s marginal cost

curve, MC.

The monopolist’s marginal

revenue curve is MR.

The monopolist’s equilibrium

quantity is QM where marginal

revenue equals marginal cost.

The

equilibrium price is PM , shown

by

the demand at QM.

Monopoly Equilibrium

35.

MONOPOLY AND COMPETITION

▶Competitive and Monopolistic Equilibrium

▶Monopoly quantity is lower and price is higher

▶A monopolist supplies a smaller quantity than a competitive

market would supply at a higher price.

▶The higher price allows a monopolist to earn positive long-

run economic profits.

36.

MONOPOLY AND COMPETITION

▶Economic Consequences of Monopoly

▶The absence of competition results in

• Inefficiency and deadweight

loss Redistribution of wealth

•

37.

MONOPOLY AND COMPETITION

Thecompetitive equilibrium

price, PC, brings consumers’

marginal benefit into equality

with producers’ marginal cost.

Therefore, the competitive

equilibrium quantity, QC, is

efficient. The sum of

consumer surplus and

producer surplus is

maximized.

Efficiency of Competitive

Equilibrium

38.

MONOPOLY AND COMPETITION

Marginalbenefit in the

monopoly equilibrium (equals to

the monopoly equilibrium price,

PM) exceeds marginal cost.

Therefore, the monopoly

equilibrium quantity, QM, is

inefficient because of

underproduction. Monopoly

results

in a deadweight loss.

Inefficiency of

Monopoly

MONOPOLY AND COMPETITION

Thedeadweight loss of

monopoly arises from a net loss

in both consumer and producer

surplus compared with the

competitive equilibrium.

In addition to the net loss in the

total surplus, monopoly also

redistributes some of the

remaining surplus from consumers

to the monopolist.

Monopoly Redistributes Wealth