1. .

Market Outlook

India Research

August 13, 2010

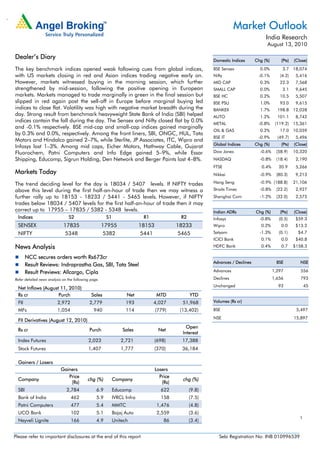

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

The key benchmark indices opened weak following cues from global indices, BSE Sensex 0.0% 3.7 18,074

with US markets closing in red and Asian indices trading negative early on. Nifty -0.1% (4.2) 5,416

However, markets witnessed buying in the morning session, which further MID CAP 0.3% 22.3 7,568

strengthened by mid-session, following the positive opening in European SMALL CAP 0.0% 3.1 9,645

markets. Markets managed to trade marginally in green in the final session but BSE HC 0.2% 10.5 5,507

slipped in red again post the sell-off in Europe before marginal buying led BSE PSU 1.0% 93.0 9,615

indices to close flat. Volatility was high with negative market breadth during the BANKEX 1.7% 198.8 12,028

day. Strong result from benchmark heavyweight State Bank of India (SBI) helped AUTO 1.2% 101.1 8,742

indices contain the fall during the day. The Sensex and Nifty closed flat by 0.0%

METAL -0.8% (119.2) 15,361

and -0.1% respectively. BSE mid-cap and small-cap indices gained marginally

OIL & GAS 0.2% 17.0 10,059

by 0.3% and 0.0%, respectively. Among the front liners, SBI, ONGC, HUL, Tata

BSE IT -0.9% (49.7) 5,496

Motors and Hindalco gained 2–7%, while Sterlite, JP Associates, ITC, Wipro and

Global Indices Chg (%) (Pts) (Close)

Infosys lost 1–3%. Among mid caps, Eicher Motors, Hathway Cable, Gujarat

Fluorochem, Patni Computers and Info Edge gained 5–9%, while Essar Dow Jones -0.6% (58.9) 10,320

Shipping, Educomp, Sigrun Holding, Den Network and Berger Paints lost 4–8%. NASDAQ -0.8% (18.4) 2,190

FTSE 0.4% 20.9 5,266

Markets Today Nikkei -0.9% (80.3) 9,213

The trend deciding level for the day is 18034 / 5407 levels. If NIFTY trades Hang Seng -0.9% (188.8) 21,106

above this level during the first half-an-hour of trade then we may witness a Straits Times -0.8% (22.2) 2,927

further rally up to 18153 - 18233 / 5441 - 5465 levels. However, if NIFTY Shanghai Com -1.2% (32.0) 2,575

trades below 18034 / 5407 levels for the first half-an-hour of trade then it may

correct up to 17955 – 17835 / 5382 - 5348 levels. Indian ADRs Chg (%) (Pts) (Close)

Indices S2 S1 R1 R2 Infosys -0.8% (0.5) $59.3

SENSEX 17835 17955 18153 18233 Wipro 0.2% 0.0 $13.2

NIFTY 5348 5382 5441 5465 Satyam -1.3% (0.1) $4.7

ICICI Bank 0.1% 0.0 $40.8

News Analysis HDFC Bank 0.4% 0.7 $158.3

NCC secures orders worth Rs673cr

Advances / Declines BSE NSE

Result Reviews: Indraprastha Gas, SBI, Tata Steel

Result Previews: Allcargo, Cipla Advances 1,297 556

Refer detailed news analysis on the following page. Declines 1,656 793

Unchanged 93 45

Net Inflows (August 11, 2010)

Rs cr Purch Sales Net MTD YTD

FII 2,972 2,779 193 4,027 51,968 Volumes (Rs cr)

MFs 1,054 940 114 (779) (13,402) BSE 5,497

NSE 15,897

FII Derivatives (August 12, 2010)

Open

Rs cr Purch Sales Net

Interest

Index Futures 2,023 2,721 (698) 17,388

Stock Futures 1,407 1,777 (370) 36,184

Gainers / Losers

Gainers Losers

Price Price

Company chg (%) Company chg (%)

(Rs) (Rs)

SBI 2,784 6.9 Educomp 622 (9.8)

Bank of India 462 5.9 IVRCL Infra 158 (7.5)

Patni Computers 477 5.4 MMTC 1,476 (4.8)

UCO Bank 102 5.1 Bajaj Auto 2,559 (3.6)

1

Neyveli Lignite 166 4.9 Unitech 86 (3.4)

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

NCC secures orders worth Rs673cr

Nagarjuna Construction Company (NCC) has secured six new orders worth Rs673cr from

different clients. These orders are spread across verticals of building, oil/gas and urban

infrastructure. Secured orders are expected to be executed within 8–30 months. With these

new orders, the outstanding order book now stands at ~Rs16,700cr (3.5x FY2010

revenue). At the CMP of Rs161, the stock trades at 16.4x FY2012E P/E and 1.6x FY2012E

P/B. We maintain a Buy rating on NCC with a Target Price of Rs201.

Result Review – 1QFY2011

Indraprastha Gas

Indraprastha Gas (IGL) reported its 1QFY2011 results, which were above our expectations

on the top-line front, but were marginally below expectations on the bottom-line front. The

top line registered growth of 43.5% yoy to Rs336cr (Rs234cr), against our expectation of

Rs318cr. During the quarter, CNG volumes increased 17.8% yoy to 142mnkg

(120.5mnkg), above our expectation of 137mnkg. PNG volumes increased 102.9% yoy to

35.5mmscm (17.5mmscm), above our expectation of 28mmscm. Total volumes came in at

221.5mmscm (175.4mmscm), above our expectation of 207.5mmscm. However, the dent

came in on account of higher-than-expected raw-material cost, which stood at Rs166.7cr,

against our expectation of Rs148.2cr. This resulted in OPM coming in at 32%, which was

below our expectation of 34.3%. Depreciation cost also came in above our expectation at

Rs23.1cr. The bottom line increased 18.4% to Rs57.1cr (Rs48.3cr), against our expectation

of Rs60.3cr. We maintain a Neutral view on the stock.

State Bank of India

For 1QFY2011, State Bank of India (SBI) reported net profit growth of 25.1% on a yoy

basis and 56.1% on a sequential basis to Rs2,914cr, above our estimates, on account of

better-than-estimated NII coupled with lower operating expenses. Robust operating

performance and stable asset quality were the key highlights of the result.

NII grew by healthy 45.4% on a yoy basis and by 8.7% on a sequential basis to Rs7,304cr.

Non-interest income stood at Rs3,690cr, up by 3.4% yoy but down by 18.2% sequentially.

Operating costs decreased 1.2% yoy and 19.5% on a sequential basis. The cost-to-income

ratio stood at 44.2%, much lower than its eight-quarter average of 49.6%. Gross NPAs

were up by 6.6% sequentially to Rs20,825cr, while net NPAs were up by 1.9% sequentially

to Rs11,074cr. The bank’s gross NPA ratio was stable at 3.14% compared to 3.05% as of

4QFY2010. While net NPA ratio improved marginally to 1.70% (from 1.72% in

4QFY2010). The provision coverage ratio excluding technical write-offs was at 46.8%

compared to 44.4% in 4QFY2010. The bank’s CAR stood at 13.5% as compared to 13.4%

in 4QFY2010.

Deposits grew by 6.8% yoy to Rs8,15,297cr, driven by CASA growth of 28.9% and retail

term deposit growth of 10.2%, despite shedding of high-cost bulk deposits by 51.4%. The

CASA ratio improved to 47.5% as of 1QFY2011 from 38.5% as of 1QFY2010. Net

advances registered growth of 20.4% yoy to Rs6,53,220cr, underpinned by strong growth

of 34.7% yoy in large corporate advances and growth of 29.8% yoy in the home loans

segment.

We may revisit our earnings estimates and target price post our interaction with the bank’s

management. SBI (excluding value of insurance and capital market subsidiaries) is trading

at 1.7x FY2012E ABV v/s its five-year range of 1.3–2.0x. We believe this provides sufficient

margin of safety and attractive upside, especially in light of its dominant position and

reach, strong growth and superior earnings quality. Presently, we maintain an Accumulate

rating on the stock with a Target Price of Rs3,021.

August 13, 2010 2

3. Market Outlook | India Research

Tata Steel

Tata Steel’s standalone 1QFY2011 net revenue grew by 16.5% yoy to Rs6,471cr but was

down 13.3% qoq. During the quarter, production was lower on a sequential basis due to

maintenance shutdown and power failure at its plants. While sales volume was flat yoy, it

declined 17.7% qoq to 1.4mn tonnes. Average realisation increased by 22% yoy and 4.9%

qoq to US $1,009/tonne. EBITDA margin expanded by 1,357bp to 43.8% on account of

cost reduction initiatives and higher realisations. Consequently, EBITDA grew by 68.8% yoy

to Rs2,836cr. Interest expense declined by 4.2% yoy to Rs328cr, while other income

increased by 19.3% yoy to Rs129cr. As a result, net profit came in at Rs1,579cr, registering

growth 100% yoy.

On a consolidated basis, Tata Steel’s net revenue increased by 16.8% yoy, down 1.1%

qoq, to Rs27,195cr. In Europe, deliveries increased to 3.7mn tonnes as compared to

3.3mn tonnes in 1QFY2010, but they were down sequentially from 3.9mn tonnes in

4QFY2010. EBITDA/tonne for European operations increased to US $79 in 1QFY2011 as

compared to a loss of US $117 in 1QFY2010. Consolidated EBITDA stood at Rs4,433cr as

compared to a loss of Rs30cr in 1QFY2010 and net profit stood at Rs1,825cr as

compared to a loss of 2,209cr in 1QFY2010. We maintain our Buy rating on the stock

with a Target Price of Rs697.

Result Previews – 1QFY2011

Allcargo Global Logistics – 2QCY2010

Allcargo Global Logistics (AGL) is scheduled to announce its 2QCY2010 results. We expect

AGL to report healthy top-line growth of 12.4% to Rs588cr, led by strong performance of

the MTO and CFS segments on the back of revival in EXIM business. The company’s OPM

is expected to be marginally lower yoy by ~143bp to 10.5% on account of higher freight

charges and appreciation of euro impacting operating profits from ECU line business.

Consequently, we expect AGL’s net profit to fall 22.1% yoy to Rs36.3cr. At Rs167, the stock

is trading at 11.7x its CY2011E earnings of Rs14.3. We maintain a Neutral rating on the

stock.

Cipla

Cipla is slated to announce its 1QFY2011 results. The company is expected to post modest

sales growth of 6.6% to Rs1,412cr, mainly driven by the domestic formulation segment.

The company's OPM (excluding technical know-how fees) is expected to contract by 336bp

to 18.6% on account of lower gross margins and higher employee expenses. Further, net

profit is estimated to fell by 7.0% to Rs225cr because of lower OPM. We recommend

Accumulate on the stock with a Target Price of Rs360.

August 13, 2010 3

4. Market Outlook | India Research

Economic and Political News

June IIP below estimates at 7.1%

Mobile number portability to be rolled out from October 31

April-July Indirect Tax collections up 46.2%

Corporate News

Ssangyong picks M&M as preferred bidder

Maran's offer to buy 20% additional stake in SpiceJet deferred

Vedanta in talks to buy stake in Cairn India

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

Ackruti City Results

Adani Enterprises Results

Cipla Results

Deccan Chronicle Results

Dhanalakshmi Bank Results

Finolex Ind Results

McNally Bharat Engg. Results

MSK Projects Results

Nitin Fire Results

Patel Engg Results

Pipavav Shipyard Results

Rajesh Exports Results

Reliance Comm Results

Saregama India Results

Shiv Vani Oil Results

Suzlon Energy Results

Tanla Solutions Results

Trigyn Tech Results

Wockhardt Results

August 13, 2010 4

5. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has not

independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation or

warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours

to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that

prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

August 13, 2010 5