CALL ON ➥8923113531 🔝Call Girls Gomti Nagar Lucknow best sexual service

Market Outlook - September 23, 2010

1. Market Outlook

India Research

September 23, 2010

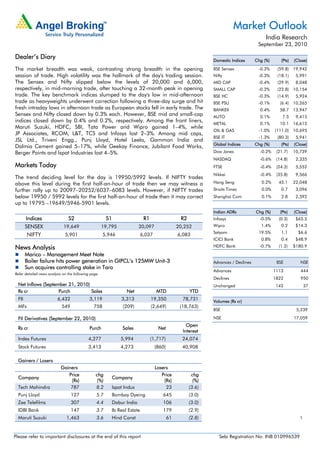

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

The market breadth was weak, contrasting strong breadth in the opening BSE Sensex -0.3% (59.8) 19,942

session of trade. High volatility was the hallmark of the day's trading session. Nifty -0.3% (18.1) 5,991

The Sensex and Nifty slipped below the levels of 20,000 and 6,000, MID CAP -0.4% (29.9) 8,048

respectively, in mid-morning trade, after touching a 32-month peak in opening SMALL CAP -0.2% (22.8) 10,154

trade. The key benchmark indices slumped to the day's low in mid-afternoon BSE HC -0.3% (14.9) 5,924

trade as heavyweights underwent correction following a three-day surge and hit BSE PSU -0.1% (6.4) 10,265

fresh intraday lows in afternoon trade as European stocks fell in early trade. The BANKEX 0.4% 58.7 13,947

Sensex and Nifty closed down by 0.3% each. However, BSE mid and small-cap AUTO 0.1% 7.5 9,415

indices closed down by 0.4% and 0.2%, respectively. Among the front liners,

METAL 0.1% 10.1 16,615

Maruti Suzuki, HDFC, SBI, Tata Power and Wipro gained 1–4%, while

OIL & GAS -1.0% (111.0) 10,695

JP Associates, RCOM, L&T, TCS and Infosys lost 2–3%. Among mid caps,

BSE IT -1.3% (80.3) 5,941

JSL Ltd., Triveni Engg., Punj Lloyd, Hotel Leela, Gammon India and

Global Indices Chg (%) (Pts) (Close)

Dalmia Cement gained 5–17%, while Geekay Finance, Jubilant Food Works,

Berger Paints and Ispat Industries lost 4–5%. Dow Jones -0.2% (21.7) 10,739

NASDAQ -0.6% (14.8) 2,335

Markets Today FTSE -0.4% (24.3) 5,552

Nikkei -0.4% (35.8) 9,566

The trend deciding level for the day is 19950/5992 levels. If NIFTY trades

above this level during the first half-an-hour of trade then we may witness a Hang Seng 0.2% 45.1 22,048

further rally up to 20097–20252/6037–6083 levels. However, if NIFTY trades Straits Times 0.0% 0.7 3,096

below 19950 / 5992 levels for the first half-an-hour of trade then it may correct Shanghai Com 0.1% 2.8 2,592

up to 19795 –19649/5946-5901 levels.

Indian ADRs Chg (%) (Pts) (Close)

Indices S2 S1 R1 R2 Infosys -0.5% (0.3) $65.5

SENSEX 19,649 19,795 20,097 20,252 Wipro 1.4% 0.2 $14.3

Satyam 19.5% 1.1 $6.6

NIFTY 5,901 5,946 6,037 6,083

ICICI Bank 0.8% 0.4 $48.9

News Analysis HDFC Bank -0.7% (1.2) $180.9

Marico – Management Meet Note

Boiler failure hits power generation in GIPCL’s 125MW Unit-3 Advances / Declines BSE NSE

Sun acquires controlling stake in Taro

Advances 1113 444

Refer detailed news analysis on the following page.

Declines 1822 950

Net Inflows (September 21, 2010) Unchanged 142 37

Rs cr Purch Sales Net MTD YTD

FII 6,432 3,119 3,313 19,350 78,731 Volumes (Rs cr)

MFs 549 758 (209) (2,649) (18,763)

BSE 5,239

FII Derivatives (September 22, 2010) NSE 17,059

Open

Rs cr Purch Sales Net

Interest

Index Futures 4,277 5,994 (1,717) 24,074

Stock Futures 3,413 4,273 (860) 40,908

Gainers / Losers

Gainers Losers

Price chg Price chg

Company Company

(Rs) (%) (Rs) (%)

Tech Mahindra 787 8.2 Ispat Indus 23 (3.6)

Punj Lloyd 127 5.7 Bombay Dyeing 645 (3.0)

Zee Telefilms 307 4.4 Dabur India 106 (3.0)

IDBI Bank 147 3.7 Ib Real Estate 179 (2.9)

Maruti Suzuki 1,463 3.6 Hind Const 61 (2.8) 1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

Marico – Management Meet Note

Core brands to post steady growth: Management is confident of driving 7–8% volume growth in

Parachute, aided by strong push of recruiter packs (5/10/20ml SKUs) and increased focus on

rural growth. Saffola is expected to sustain 14–15% volume growth, driven by strong

positioning as a good-for-heart brand.

Copra and rice bran oil rise, 3–5% price hikes taken: On a yoy basis YTD, copra prices have

risen by almost 12–15%. However, in 2QFY2011, copra prices witnessed a steep rise of

20–25% and rice bran oil was up almost 10% yoy. Hence, Marico initiated another price hike of

~5% (from Rs40 to Rs42) in the 200ml SKU in August and Rs3/litre hike (~3% hike) in Saffola

Gold/Saffola Active.

International business on strong footing, we peg 22% CAGR over FY2010–12E: Management is

confident of sustaining 20–25% growth across geographies, driven by better distribution reach

and new product launches. Moreover, current OPMs at ~12% in the international business are

likely to improve to ~14% over 2–3 years, aided by supply chain re-engineering and price

increases.

Kaya domestic under consolidation, 4–6 clinics to be opened in the Middle East: Focus on Kaya

has now shifted to improve consumer experience and pushing product revenue higher. In

2QFY2011, Marico opened one more clinic in the Middle East and Bangladesh respectively,

taking the total tally to 101 clinics. In FY2011, Marico plans to open no new clinics in India and

around 4–6 clinics in the Middle East. During 3QFY2011, management plans to introduce

Derma-Rx products in India and Middle East.

No major capex, tax guidance of 19–20% maintained: Capex for FY2011E includes

Rs15cr–20cr maintenance capex, Rs25cr additional capex for Baddi plant and Rs4cr–6cr for

Kaya clinics. Management has maintained its tax guidance of 19–20% due to rising

contribution from tax-saving plants (Baddi and Ponta Sahib) and international operations (low

tax rate).

Outlook and valuation: We have marginally tweaked our estimates upwards to account for: 1)

recent price hikes, 2) stronger growth in international business and 3) better margins, aided by

price hikes and improving profitability in the international business. At the CMP of Rs131, the

stock is trading at 22.4x FY2012E earnings, which is justified given the 22% earnings CAGR

over FY2010–12E. Hence, we upgrade the stock from Neutral to Accumulate with a Target

Price of Rs135 (Rs124) based on a P/E multiple of 23x FY2012E earnings.

September 23, 2010 2

3. Market Outlook | India Research

Boiler failure hits power generation in GIPCL’s 125MW Unit-3

Gujarat Industries Power Company (GIPCL) has informed the BSE that there was a failure

in the boiler of 125MW Unit-3 on September 17, 2010, at its Surat Lignite Power Plant.

This has damaged the Economizer Hopper and some parts of Back-pass of the Boiler

accidentally and has resulted in stoppage of power generation from the unit, which was

commissioned and synchronised recently in April 2010. The costs of repair will be borne

by the EPC Contractor as the unit is yet to be taken over by the company. The company

expects restoration work to be completed in about 30 days. As we had factored in only six

months of operation for Unit-3 in FY2011, this development does not affect our revenue

estimates. We expect the company’s top line and bottom line to log in CAGRs of 32.5%

and 28.3% over FY2010–12E, respectively. We expect RoE to improve from 8.8% in

FY2010E to 12.4% in FY2012E, following commissioning of new plants. At the CMP of

Rs116, the stock is trading at 1.2x P/BV and EV/MW of Rs3.5cr on FY2012E estimates,

which we believe is attractive compared to its peers. We maintain a Buy rating on the stock

with a Target Price of Rs135.

Sun acquires controlling stake in Taro

Sun Pharma (Sun) has announced that it has completed the acquisition of controlling stake

in Taro Pharma (Taro) post the closure of the tender offer. As a result, the company’s stake

in Taro would increase to 48.7% (c 36.6%) with voting rights of 65.8% (c 24%). Further,

directors of Sun and Taro have settled all outstanding litigation among themselves. The

acquisition of Levitt’s family stake would result into an outflow of US $37.2mn for Sun,

taking the total investment in Taro to US $165mn (including warrant conversions). We view

this development as positive as Sun would now get access to Taro’s dermatology product

portfolio in the US and new geographies, viz. Israel and Canada. For 1HCY2010, Taro

recorded net sales of US $187mn, with OPM of 19.7%. However, pending clarity on the

financials of Taro (audited financials for CY2008 and CY2009 have not been filed), we

have valued Sun’s stake in Taro at Rs85 per share (1x Mcap/Sales). The stock is currently

trading at 26.9x FY2011E and 22.7x FY2012E earnings; we maintain our Neutral rating

on Sun at these levels.

September 23, 2010 3

4. Market Outlook | India Research

Economic and Political News

EPFO asks private PF trusts to pay 9.5% interest

Farm output rise to ease food inflation, says Ahluwalia

Gold rises to record high after Fed rates nod

Corporate News

IOC unveils plan to double petrochemical revenue to Rs15,000cr

Nestle to invest Rs1,230cr in new plant, R&D centre

ONGC ventures into shale gas exploration

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

September 23, 2010 4

5. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel: (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

September 23, 2010 5