( Jasmin ) Top VIP Escorts Service Dindigul 💧 7737669865 💧 by Dindigul Call G...

Market Outlook - September 27, 2010

1. Market Outlook

India Research

September 28, 2010

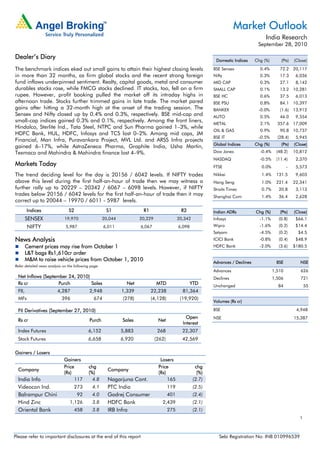

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

The benchmark indices eked out small gains to attain their highest closing levels BSE Sensex 0.4% 72.2 20,117

in more than 32 months, as firm global stocks and the recent strong foreign Nifty 0.3% 17.3 6,036

fund inflows underpinned sentiment. Realty, capital goods, metal and consumer MID CAP 0.3% 27.1 8,142

durables stocks rose, while FMCG stocks declined. IT stocks, too, fell on a firm SMALL CAP 0.1% 13.2 10,281

rupee. However, profit booking pulled the market off its intraday highs in BSE HC 0.6% 37.5 6,013

afternoon trade. Stocks further trimmed gains in late trade. The market pared BSE PSU 0.8% 84.1 10,397

gains after hitting a 32-month high at the onset of the trading session. The BANKEX -0.0% (1.6) 13,912

Sensex and Nifty closed up by 0.4% and 0.3%, respectively. BSE mid-cap and AUTO 0.5% 46.0 9,554

small-cap indices gained 0.3% and 0.1%, respectively. Among the front liners,

METAL 2.1% 357.6 17,009

Hindalco, Sterlite Ind., Tata Steel, NTPC and Sun Pharma gained 1–3%, while

OIL & GAS 0.9% 90.8 10,737

HDFC Bank, HUL, HDFC, Infosys and TCS lost 0–2%. Among mid caps, JM

BSE IT -0.5% (28.4) 5,945

Financial, Man Infra, Puravankara Project, MVL Ltd. and ARSS Infra projects

Global Indices Chg (%) (Pts) (Close)

gained 6–17%, while AstraZeneca Pharma, Graphite India, Usha Martin,

Texmaco and Mahindra & Mahindra finance lost 4–9%. Dow Jones -0.4% (48.2) 10,812

NASDAQ -0.5% (11.4) 2,370

Markets Today FTSE 0.0% - 5,573

The trend deciding level for the day is 20156 / 6042 levels. If NIFTY trades Nikkei 1.4% 131.5 9,603

above this level during the first half-an-hour of trade then we may witness a Hang Seng 1.0% 221.4 22,341

further rally up to 20229 – 20342 / 6067 – 6098 levels. However, if NIFTY Straits Times 0.7% 20.8 3,113

trades below 20156 / 6042 levels for the first half-an-hour of trade then it may Shanghai Com 1.4% 36.4 2,628

correct up to 20044 – 19970 / 6011 - 5987 levels.

Indices S2 S1 R1 R2 Indian ADRs Chg (%) (Pts) (Close)

SENSEX 19,970 20,044 20,229 20,342 Infosys -1.1% (0.8) $66.1

NIFTY 5,987 6,011 6,067 6,098 Wipro -1.6% (0.2) $14.4

Satyam -4.5% (0.2) $4.5

News Analysis ICICI Bank -0.8% (0.4) $48.9

Cement prices may rise from October 1 HDFC Bank -2.0% (3.6) $180.5

L&T bags Rs1,610cr order

M&M to raise vehicle prices from October 1, 2010 Advances / Declines BSE NSE

Refer detailed news analysis on the following page.

Advances 1,510 626

Net Inflows (September 24, 2010) Declines 1,506 721

Rs cr Purch Sales Net MTD YTD Unchanged 84 55

FII, 4,287 2,948 1,339 22,238 81,364

MFs 396 674 (278) (4,128) (19,920)

Volumes (Rs cr)

FII Derivatives (September 27, 2010) BSE 4,948

Open NSE 15,387

Rs cr Purch Sales Net

Interest

Index Futures 6,152 5,883 268 22,307

Stock Futures 6,658 6,920 (262) 42,569

Gainers / Losers

Gainers Losers

Price chg Price chg

Company Company

(Rs) (%) (Rs) (%)

India Info 117 4.8 Nagarjuna Cont. 165 (2.7)

Videocon Ind. 273 4.1 PTC India 119 (2.5)

Balrampur Chini 92 4.0 Godrej Consumer 401 (2.4)

Hind Zinc 1,126 3.8 HDFC Bank 2,439 (2.1)

Oriental Bank 458 3.8 IRB Infra 275 (2.1)

1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

Cement prices may rise from October 1

Media reports suggest that cement manufacturers are set to hike prices by around Rs20

per 50kg bag from October 1 in Gujarat, while a similar hike is being contemplated for

Maharashtra, including the key market of Mumbai, to cash in on the spurt in demand

following the monsoons. Companies including UltraTech Cement, Ambuja Cements,

Sanghi Industries, Gujarat Siddhi Cement, Saurashtra Cement, Binani Cement, JK Lakshmi

Cement and Jaiprakash Associates will raise the prices of the commodity.

Cement prices had cracked to around Rs150 in August from its peak of Rs225 in mid-May,

owing to sluggish construction activity in the monsoons and scarcity of sand and, with the

proposed hike, prices of the commodity will be around Rs180 per 50kg bag in

Ahmedabad. In Mumbai, the hike is being considered and may be implemented in a

different way by withdrawing a discount of at least Rs10 per bag that is being offered to

dealers, said a city-based large cement stockist. The southern region, which witnessed two

rounds of price hike in September, despite low demand and over capacity is also set to

witness another round of price hike. In Hyderabad, prices may be hiked by Rs30 per bag,

pushing cement prices to around Rs240; while Chennai prices may be hiked by as much

as Rs40. Stockists and dealers in the central and northern regions have not been intimated

about any hike in these regions yet. However, cement companies may announce some

hikes in these regions depending on the response to the hikes in southern and western

India.

We maintain Buy on India Cements with a Target Price of Rs139, Madras Cements with a

Target Price of Rs139 and JK Lakshmi Cement with a Target Price of Rs92, due to their

attractive valuations. We recommend Accumulate on Ultratech with a Target Price of

Rs1,087.

L&T bags Rs1,610cr order

Larsen & Toubro (L&T) has bagged an order worth Rs1,610cr from Visa Steel and Power

Company for executing Balance of Plant (BOP) package for a 2x600MW power plant,

coming up at Raigarh-Chhattisgarh. The expected period of execution is between 29–32

months. This order from VISA Power Ltd. follows a recent order for Rs6,500cr received last

month from Jaiprakash Power Ventures Ltd., a Jaiprakash Group Power Company for a

3x660MW supercritical Boiler–Steam Turbine Generator Package Karchana power project.

L&T is one of the few companies to bag consistent orders in recent times, especially from

the power segment. This is very much reflected in the sharp run up in the stock price as

well. At Rs2,026, stock is trading at P/E of 29.5x and P/BV of 4.9x to its FY2012E on

standalone basis. We believe most of the positives are factored in and, hence, maintain

our Neutral rating on the stock. However, since we believe the near-term catalysts are in

place for the stock, we recommend investors to remain equal weight despite rich

valuations.

September 28, 2010 2

3. Market Outlook | India Research

M&M to raise vehicle prices from October 1, 2010

M&M plans to raise prices of its passenger and commercial vehicle products, effective from

October 1, 2010. The price increase would be in the range of Rs3,000 to Rs8,000,

depending on the model. The increase in prices comes on expected lines, as the company

intends to protect its margins in the wake of increased cost due to introduction of new

emission norms (Bharat Stage III), effective from October 2010, and the recent hike in raw-

material prices. Because of the recent positive movement in the stock price, we recommend

Accumulate on the stock with an SOTP Target Price of Rs771.

Economic and Political News

Govt. neutralises tax impact of 1st year of DTC regime

Govt. imposes anti-dumping duty on chemical from China

Steel prices may go up by Rs1,500 a tonne next month

Industry ad budget up 30–40% in 2010–11

Foreigners to fund up to 30% of Indian roads

Corporate News

PFC to issue infra bonds of Rs1,000cr by December-end

IndusInd Bank raises US $253mn through QIP

IDFC launches first tax-free infra bonds to raise Rs3,400cr

IRB Infra to raise Rs750cr debt for Karrnataka road project

AstraZeneca’s plan to delist rejected

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

September 28, 2010 3

4. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel: (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

September 28, 2010 4