VIP Call Girls LB Nagar ( Hyderabad ) Phone 8250192130 | ₹5k To 25k With Room...

India Market Edges Lower on Profit-taking

1. Market Outlook

India Research

October 18, 2010

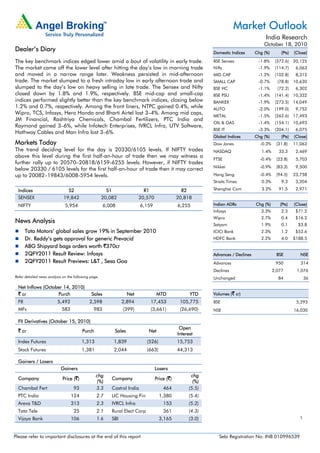

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

The key benchmark indices edged lower amid a bout of volatility in early trade. BSE Sensex -1.8% (372.6) 20,125

The market came off the lower level after hitting the day’s low in morning trade Nifty -1.9% (114.7) 6,063

and moved in a narrow range later. Weakness persisted in mid-afternoon MID CAP -1.2% (102.8) 8,312

trade. The market slumped to a fresh intraday low in early afternoon trade and SMALL CAP -0.7% (78.8) 10,630

slumped to the day’s low on heavy selling in late trade. The Sensex and Nifty BSE HC -1.1% (72.2) 6,302

closed down by 1.8% and 1.9%, respectively. BSE mid-cap and small-cap BSE PSU -1.4% (141.4) 10,332

indices performed slightly better than the key benchmark indices, closing below BANKEX -1.9% (273.5) 14,049

1.2% and 0.7%, respectively. Among the front liners, NTPC gained 0.4%, while AUTO -2.0% (199.0) 9,752

Wipro, TCS, Infosys, Hero Honda and Bharti Airtel lost 3–4%. Among mid caps,

METAL -1.5% (262.6) 17,493

JM Financial, Rashtriya Chemicals, Chambal Fertilizers, PTC India and

OIL & GAS -1.4% (154.1) 10,693

Raymond gained 3–6%, while Infotech Enterprises, IVRCL Infra, UTV Software,

BSE IT -3.3% (204.1) 6,075

Hathway Cables and Man Infra lost 3–6%.

Global Indices Chg (%) (Pts) (Close)

Markets Today Dow Jones -0.3% (31.8) 11,063

The trend deciding level for the day is 20330/6105 levels. If NIFTY trades NASDAQ 1.4% 33.3 2,469

above this level during the first half-an-hour of trade then we may witness a

FTSE -0.4% (23.8) 5,703

further rally up to 20570–20818/6159-6255 levels. However, if NIFTY trades

Nikkei -0.9% (83.3) 9,500

below 20330 / 6105 levels for the first half-an-hour of trade then it may correct

up to 20082–19843/6008-5954 levels. Hang Seng -0.4% (94.5) 23,758

Straits Times 0.3% 9.3 3,204

Indices S2 S1 R1 R2 Shanghai Com 3.2% 91.5 2,971

SENSEX 19,842 20,082 20,570 20,818

NIFTY 5,954 6,008 6,159 6,255 Indian ADRs Chg (%) (Pts) (Close)

Infosys 3.3% 2.3 $71.2

Wipro 2.7% 0.4 $16.2

News Analysis

Satyam 1.9% 0.1 $3.8

Tata Motors’ global sales grow 19% in September 2010 ICICI Bank 2.3% 1.2 $52.6

Dr. Reddy’s gets approval for generic Prevacid HDFC Bank 2.2% 4.0 $188.5

ABG Shipyard bags orders worth `370cr

2QFY2011 Result Review: Infosys Advances / Declines BSE NSE

2QFY2011 Result Previews: L&T , Sesa Goa Advances 950 314

Declines 2,077 1,076

Refer detailed news analysis on the following page. Unchanged 84 36

Net Inflows (October 14, 2010)

` cr Purch Sales Net MTD YTD Volumes (` cr)

FII 5,492 2,598 2,894 17,453 105,775 BSE 5,293

MFs 583 983 (399) (3,661) (26,690) NSE 16,030

FII Derivatives (October 15, 2010)

Open

` cr Purch Sales Net

Interest

Index Futures 1,313 1,839 (526) 15,753

Stock Futures 1,381 2,044 (663) 44,313

Gainers / Losers

Gainers Losers

chg chg

Company Price (`) Company Price (`)

(%) (%)

Chambal Fert 93 3.3 Castrol India 464 (5.5)

PTC India 124 2.7 LIC Housing Fin 1,380 (5.4)

Areva T&D 313 2.3 IVRCL Infra 153 (5.2)

Tata Tele 25 2.1 Rural Elect Corp 361 (4.3)

Vijaya Bank 106 1.6 SBI 3,165 (3.0) 1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

Tata Motors’ global sales grow 19% in September 2010

Tata Motors reported its global sales numbers for September 2010, which increased by

19% yoy to 86,996 units. Growth was led by strong growth in commercial and passenger

vehicle sales.

During the month, sales of commercial vehicles grew 18% yoy to 40,961 units and sales of

passenger vehicles grew by 21% yoy to 46,035 units in September 2010. Sales of luxury

brands Jaguar and Land Rover (JLR) maintained a strong traction, posting 16% yoy growth

to 19,528 units. Jaguar sales stood at 4,861 units, up 10% yoy; while Land Rover sales

grew by 19% yoy to 14,667 units. JLR continues to see robust demand in the UK, the US,

China and Russia. Moreover, with global sales witnessing strong growth, Tata Motors now

plans to retain all the three JLR plants in the UK against its earlier plan to consolidate its

operations in the region and shut one of its plants.

We expect Tata Motors to post healthy volume growth going ahead. We continue to

maintain our Accumulate rating on the stock with an SOTP Target Price of `1,214.

We value the core business at `490, implying 6.5x FY2012E EV/EBITDA and P/E of 13x

FY2012E EPS. Our embedded value of the subsidiaries and investments in Tata Motors'

books (including JLR) works out to `724/share.

Dr. Reddy’s gets approval for generic Prevacid

Dr. Reddy’s (DRL) has received US FDA approval for generic Prevacid (Lansoprazole)

delayed-release capsules (15mg and 30mg). The company plans to launch the drug

shortly in the US market. The approval is positive for the company as the product would be

a limited competition opportunity for the company (Teva, Mylan, Sandoz and other generic

players) for the next 12–15 months. We expect the product to contribute an NPV of `25 per

share. We remain Neutral on the stock at these levels.

ABG Shipyard bags orders worth `370cr

ABG Shipyard Ltd. (ABG) has bagged orders worth approximately US $82.5mn (`370cr)

from Halul Offshore Services Company (HOSC) of Qatar (US $65mn) and Manravi Spa

(Manravi) of Italy (US $17.5mn). As per the order, ABG will construct a 91-metre

twin-screw diving support vessel for HOSC and a 63.8-metre twin-screw 82T bollard pull

anchor handling tug supply vessel (AHTSV) for Marnavi.

With these two orders, ABG’s total unexecuted order book stands at more than `8,000cr

(~5.0x FY2010 sales) and is executable by FY2014E. Moreover, in 1HFY2011, the

company delivered four AHTSVs to different clients and three interceptor boats to the

Indian coast guard in 1HFY2011.

Further, ABG has completed the acquisition of Western India Shipyard (WISL) by acquiring

an incremental 40.6% stake in the company from ICICI Bank in off-market deals, taking its

stake to 60.3%. The deal is a part of the Scheme of Arrangement & Compromise between

WISL and its secured lenders, approved by the Bombay High Court in January 2010. WISL,

which has been making losses since its inception in 1996, had posted profit of about `66cr

for the first time in 4QFY2010 and profit of `5.8cr in 1QFY2011.

At the CMP, ABG is trading at 8.1x FY2012E earnings, 7.9x FY2012E EV/EBITDA and 1.4x

FY2012E P/BV. We maintain our Neutral rating on the stock.

October 18, 2010 2

3. Market Outlook | India Research

Result Review – 2QFY2011

Infosys

During 2QFY2011, Infosys reported revenue of `6,947cr, up12.1% qoq, on the back of

strong volume growth, higher revenue productivity with better business mix and favourable

cross-currency movement. EBITDA margins improved by 165bp qoq to 33.3% on the back

of better utilisation and favourable currency movement negating the effect of higher

onshore effort. We expect Infosys’ revenue, EBITDA and PAT to witness CAGRs of

21.8%,17.0% and 13.8% over FY2010-12E, respectively. At the CMP of `3,076, the stock

is trading at 21.7x FY2012E EPS, close to its intrinsic value and at par with its historical P/E

multiple of 22x. Hence, we maintain our Neutral rating on the stock.

Result Previews – 2QFY2011

L&T

Larsen & Toubro (L&T) is expected to announce its 2QFY2011 results. We expect L&T to

post modest top-line growth of 11.5% to `8,829cr on the back of good monsoons. On the

operating margin front, performance is expected to be better with a 135bp yoy increase to

11.4%, which is expected due to higher contribution from the MIP and E&E segments.

Net profit is expected to register 13.5% yoy growth to `637cr. The stock has seen a sharp

run-up in the recent times, and its premium over peers, which have underperformed, has

enhanced, thereby resulting in limited upside from current levels. Therefore, in light of the

rich valuations that the stock is trading at, we maintain our Neutral view.

Sesa Goa

Sesa Goa is slated to announce its 2QFY2011 results. We expect the company’s top line to

grow by 90.1% yoy to `1,024cr on account of higher realisations (up 67% yoy). Sales

volume for the quarter stood at 2mn tonnes as compared to 1.6mn tonnes in 2QFY2010.

On the operating front, EBITDA margin is expected at 52.1% as compared to 28.3% in

2QFY2010. Hence, the bottom line is expected to grow by 193.8% yoy to `489cr.

We maintain a Neutral rating on the stock.

October 18, 2010 3

4. Market Outlook | India Research

Economic and Political News

PM to raise visa issue, outsourcing with Obama

34 blocks put up for auctions under Nelp-IX

Ministry of Environment and Forest panel on Posco to submit report on Oct. 18

Corporate News

JLR to invest in UK, keep all three auto plants

SBI to raise `1,000cr via Tier-II bonds

NTPC yet to acquire land for two proposed super thermal power projects

Moser Baer to set up US $11.5mn organic LED facility

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

Bajaj Finserv Results

Camlin Results

Essar Oil Results

HDFC Results

Indiabulls Securities Results

ING Vysya Bank Results

L&T Results

NIIT Technologies Results

Parsvnath Developers Stock split

Sesa Goa Results

Supreme Industries Stock split

Zydus Wellness Results

October 18, 2010 4

5. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

October 18, 2010 5