Downloaded 25 times

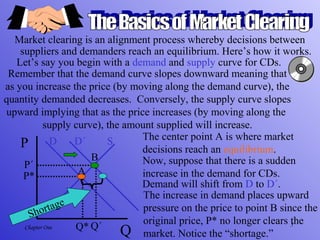

This document provides an acknowledgements section for the author Mannig J. Simidian and an introduction to the topics that will be covered in the macroeconomics textbook and course. It thanks various individuals who influenced the author and provided guidance. It also outlines some of the key macroeconomic concepts that will be discussed, including real GDP, inflation, unemployment, models, endogenous and exogenous variables, market clearing, and the relationship between microeconomics and macroeconomics.