Downloaded 336 times

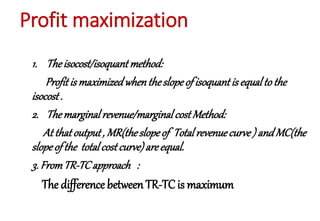

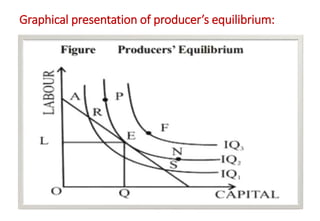

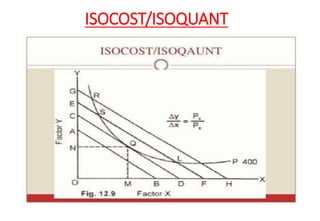

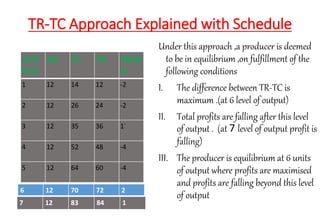

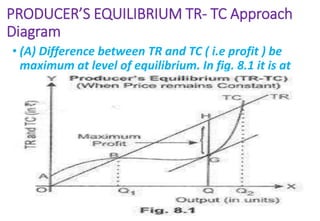

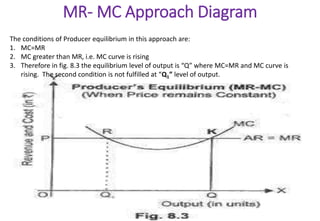

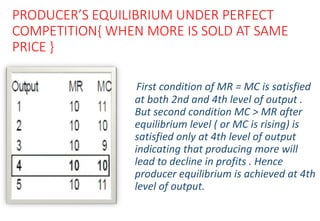

A producer seeks to maximize profits by producing at the level of output where marginal revenue equals marginal cost. This occurs at the producer's equilibrium. There are three main approaches to determining the producer's equilibrium: (1) where the isoquant is tangent to the isocost line, (2) where marginal revenue equals marginal cost, and (3) where the difference between total revenue and total cost is maximized. The equilibrium level of output is where profits are maximized and will fall if output increases beyond this level. Producer equilibrium can occur when price is constant, as in perfect competition, or when price decreases with increased output, as in imperfect competition.