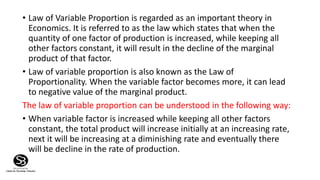

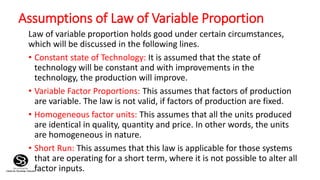

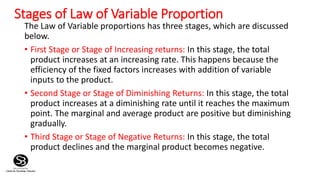

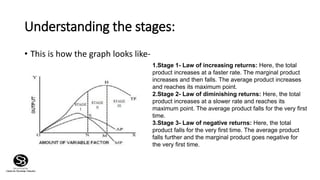

The law of variable proportion dictates that increasing one factor of production, while keeping others constant, will initially raise and then eventually decrease marginal product. This law applies under certain assumptions, including constant technology and variable factor proportions, and consists of three stages: increasing returns, diminishing returns, and negative returns. Ultimately, producers achieve equilibrium when marginal cost equals marginal revenue, indicating the optimal level of output.