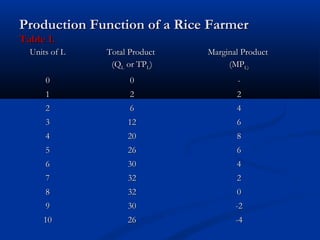

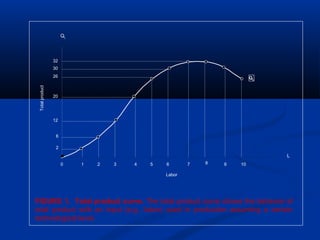

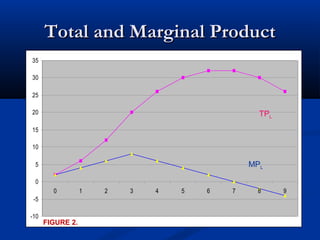

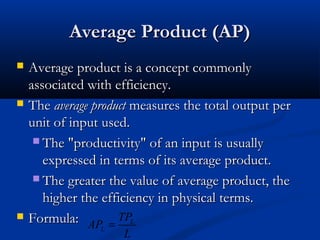

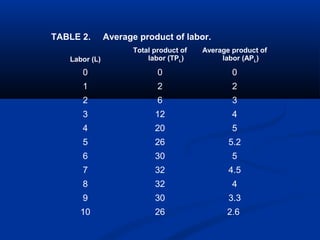

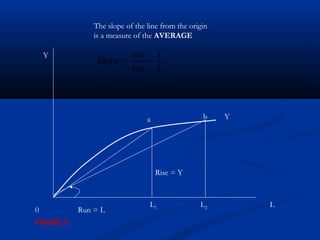

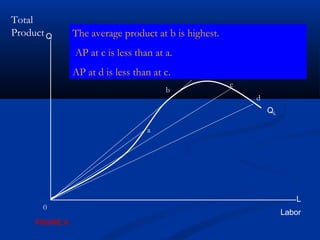

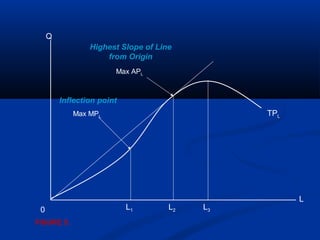

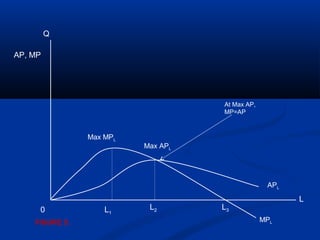

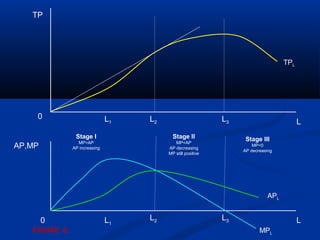

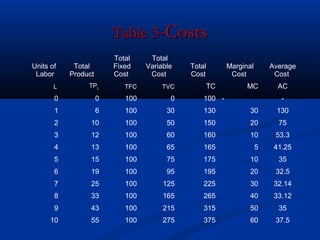

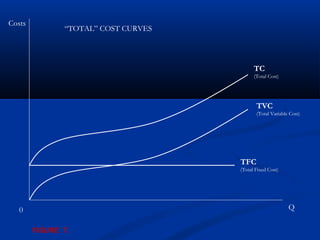

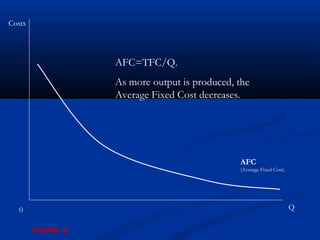

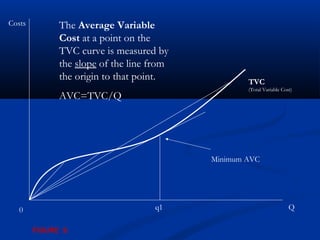

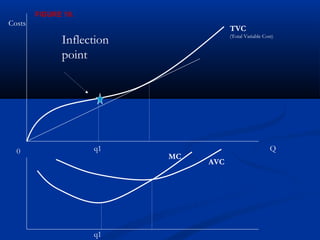

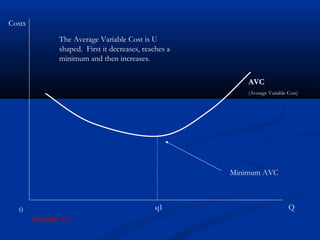

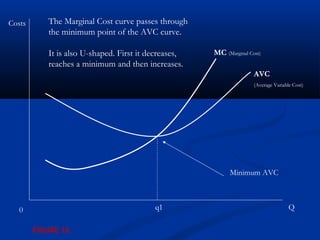

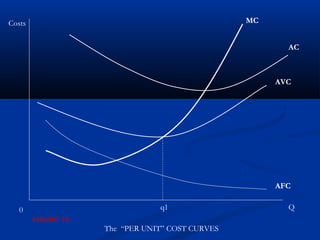

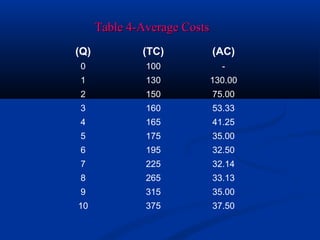

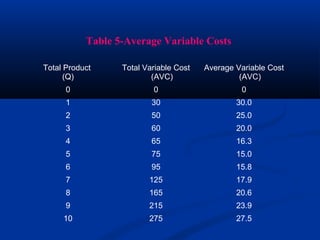

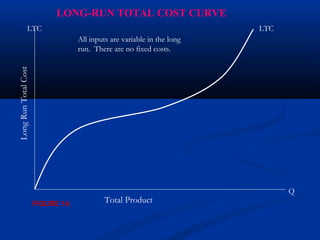

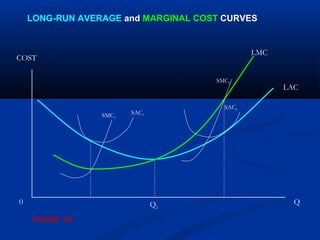

Ram Kumar Phuyal presents on production theory and costs. He discusses production functions with one and two variable inputs and the concept of returns to scale. He explains the production function and differentiates between fixed and variable inputs. Total, average, and marginal products are defined for a single variable input. There are three stages of production as marginal product first increases, then decreases and becomes negative. Short-run costs include total fixed, variable, and total costs. Average and marginal costs are also analyzed.