Fisher effect Simple Example

•

5 likes•5,249 views

The document discusses the international Fisher effect (IFE), which predicts that differences in nominal interest rates between two currencies will cause an equal but opposite change in their spot exchange rates. It provides the simple formula for calculating future spot exchange rates based on current rates and expected inflation and interest rates. An example calculation is shown where the US dollar is expected to depreciate against the South Korean won due to the higher nominal interest rate in the US.

Report

Share

Report

Share

Download to read offline

Recommended

International Arbitrage and Interest Rate Parity (IRP)

we are trying to explain the conditions that will result in various forms of international arbitrage and concept of interest rate parity

Purchasing power parity

The document discusses the concept of purchasing power parity (PPP). It defines PPP as the exchange rate between two currencies that would equalize the purchasing power of the currencies in their respective countries. The document notes that under PPP, a given amount of one currency should have the same purchasing power whether used directly to purchase goods in that country or converted to the other currency at the PPP rate. It then asks several questions about how inflation, interest rates, and other factors may impact exchange rates. The rest of the document provides explanations of absolute and relative PPP, how PPP is used to make cross-country comparisons, and some limitations of the PPP theory.

Government Influence on Exchange Rates

describing the exchange rate systems, explaining how government uses direct and indirect intervention to influence exchange rates, and how government intervention in the forex markets.

International fisher effect

This document discusses the international Fisher effect and interest rate parity. It explains that the Fisher effect postulates a relationship between nominal interest rates and real interest rates adjusted for inflation. According to the Fisher effect, high inflation leads to high nominal interest rates. The document also discusses how interest rate parity argues that identical securities should have the same price when quoted in a common currency, so interest rate differentials between countries tend to be offset by forward exchange rate premiums or discounts.

Interest rate parity (Global Finance)

Interest rate parity is a theory stating that the interest rate differential between two countries should equal the forward exchange rate premium or discount relative to the spot exchange rate. This establishes a break-even condition where returns on domestic and foreign currency investments are equal after accounting for exchange risk. If interest rate parity is violated, an arbitrage opportunity exists where investors can borrow, invest, and exchange currencies to earn risk-free profits. Kim Deal, a European portfolio manager, should choose to invest in 1-year Japanese yen deposits covered by a 1-year forward contract to hedge exchange risk, as this option provides the highest euro return of €352,005 compared to €352,000 from euro deposits.

Relationship between Inflation, Interest Rates, and Exchange Rates

explaining what is Purchasing Power Parity, International Fisher Effect, Interest Parity, and their implication for exchange rate changes.

Spot and Forward Exchange Rate

The document discusses spot exchange rates, which are the prices for exchanging one currency for another for immediate delivery, usually within two business days. Spot exchange rates represent the price paid in one currency to purchase another currency. They are the prevailing rates in the foreign exchange market for currencies that are delivered immediately as opposed to a future date. Spot exchange rates make up 43% of total foreign exchange transactions and are prone to fluctuations from day to day. A spot contract is an agreement to exchange currencies at the spot rate for delivery within the standard settlement period, which is two business days after the trade date.

Forward market, arbitrage, hedging and speculation

Covers various aspects related to forward market, forward rate, long and short forward position, arbitrage, hedging and speculation along with various illustrative examples.

Recommended

International Arbitrage and Interest Rate Parity (IRP)

we are trying to explain the conditions that will result in various forms of international arbitrage and concept of interest rate parity

Purchasing power parity

The document discusses the concept of purchasing power parity (PPP). It defines PPP as the exchange rate between two currencies that would equalize the purchasing power of the currencies in their respective countries. The document notes that under PPP, a given amount of one currency should have the same purchasing power whether used directly to purchase goods in that country or converted to the other currency at the PPP rate. It then asks several questions about how inflation, interest rates, and other factors may impact exchange rates. The rest of the document provides explanations of absolute and relative PPP, how PPP is used to make cross-country comparisons, and some limitations of the PPP theory.

Government Influence on Exchange Rates

describing the exchange rate systems, explaining how government uses direct and indirect intervention to influence exchange rates, and how government intervention in the forex markets.

International fisher effect

This document discusses the international Fisher effect and interest rate parity. It explains that the Fisher effect postulates a relationship between nominal interest rates and real interest rates adjusted for inflation. According to the Fisher effect, high inflation leads to high nominal interest rates. The document also discusses how interest rate parity argues that identical securities should have the same price when quoted in a common currency, so interest rate differentials between countries tend to be offset by forward exchange rate premiums or discounts.

Interest rate parity (Global Finance)

Interest rate parity is a theory stating that the interest rate differential between two countries should equal the forward exchange rate premium or discount relative to the spot exchange rate. This establishes a break-even condition where returns on domestic and foreign currency investments are equal after accounting for exchange risk. If interest rate parity is violated, an arbitrage opportunity exists where investors can borrow, invest, and exchange currencies to earn risk-free profits. Kim Deal, a European portfolio manager, should choose to invest in 1-year Japanese yen deposits covered by a 1-year forward contract to hedge exchange risk, as this option provides the highest euro return of €352,005 compared to €352,000 from euro deposits.

Relationship between Inflation, Interest Rates, and Exchange Rates

explaining what is Purchasing Power Parity, International Fisher Effect, Interest Parity, and their implication for exchange rate changes.

Spot and Forward Exchange Rate

The document discusses spot exchange rates, which are the prices for exchanging one currency for another for immediate delivery, usually within two business days. Spot exchange rates represent the price paid in one currency to purchase another currency. They are the prevailing rates in the foreign exchange market for currencies that are delivered immediately as opposed to a future date. Spot exchange rates make up 43% of total foreign exchange transactions and are prone to fluctuations from day to day. A spot contract is an agreement to exchange currencies at the spot rate for delivery within the standard settlement period, which is two business days after the trade date.

Forward market, arbitrage, hedging and speculation

Covers various aspects related to forward market, forward rate, long and short forward position, arbitrage, hedging and speculation along with various illustrative examples.

Foreign exchange

The document discusses key concepts related to foreign exchange including:

- The meaning of foreign exchange as the conversion of one country's currency into another at exchange rates.

- How foreign exchange markets operate as global online networks where traders buy and sell currencies.

- The factors that influence exchange rates such as exports, imports, capital flows, inflation, and monetary policy.

- The difference between fixed and floating exchange rate systems and how governments intervene to maintain fixed rates.

Exchange Rate Fluctuation

The document discusses factors that influence currency exchange rates, including inflation rates, interest rates, balance of trade, government debt, economic conditions, and demand. A country's currency will appreciate if it has lower inflation or raises interest rates. Higher government debt or a recession can lead to currency depreciation. Exchange rates also depend on demand from foreign investors and international economic and political uncertainties. Models for predicting exchange rates incorporate factors like spot rates, forward rates, and demand and supply trends.

Currency Forecasting

The document discusses various methods for forecasting currency exchange rates, including fundamental and technical analysis. Fundamental analysis examines economic relationships and data using models like purchasing power parity and international fisher effect to predict future exchange rates. Technical analysis relies on historical price patterns and indicators like simple and exponential moving averages, as well as chart patterns, to forecast exchange rate movements. The document provides examples of applying these methods to predict the future GBP/RMB exchange rate.

Foreign exchange risk and hedging

Foreign exchange risk, also known as currency risk, refers to the financial risk posed by unexpected changes in exchange rates. It affects investors and businesses involved in international trade or foreign investments. There are three main types of foreign exchange exposure: transaction, economic, and translation. Transaction exposure involves existing foreign currency transactions, economic exposure impacts future cash flows and firm value, and translation exposure affects financial reporting due to exchange rate movements between periods. Companies can use hedging strategies like forward contracts, options, and money market operations to eliminate or reduce foreign exchange risk.

Relationships between Inflation, Interest Rates, and Exchange Rates

The document discusses purchasing power parity (PPP) theory and the international Fisher effect (IFE) theory. PPP theory states that inflation rate differentials between countries will lead to changes in exchange rates as the high inflation country's currency depreciates. IFE theory similarly argues that interest rate differentials, which often correlate with expected inflation differentials, will cause the high interest rate currency to depreciate. Both theories predict that the currency experiencing higher inflation or interest rates will lose value against other currencies. The document also provides derivations of the PPP and IFE formulas to calculate expected exchange rate changes based on inflation or interest rate differentials.

Foreign Exhange Rate

The document defines exchange rates as the rate at which one currency can be exchanged for another. Exchange rates are determined in the foreign exchange market, where currencies are bought and sold. The foreign exchange market serves several functions, including transferring funds between countries and providing short-term credit to importers. Exchange rates are influenced by factors such as inflation rates, interest rates, current account deficits, public debt levels, terms of trade, and political/economic stability. Various theories aim to determine exchange rates based on these economic fundamentals.

interest rate parity

This document discusses interest rate parity theory. It begins by defining spot and forward rates. Spot rates are prices for immediate settlement, while forward rates refer to rates for future currency delivery adjusted for cost of carry. Interest rate parity theory states that interest rate differentials between currencies will be reflected in forward premiums or discounts. The theory prevents arbitrage opportunities by making returns equal whether investing domestically or abroad when measured in the home currency. The document provides an example of covered and uncovered interest rate parity. Covered parity involves hedging exchange rate risk while uncovered parity does not. Empirical evidence shows uncovered parity often fails while covered parity generally holds for major currencies over short time horizons.

Government influence on exchange rate

1) The document discusses various exchange rate systems such as fixed rates, floating rates, managed floats, and pegged rates. It also discusses currency boards and the exposure of pegged currencies.

2) It describes the European single currency, including participating countries, its impact on monetary policy and business, and its status.

3) The document outlines how governments can directly and indirectly intervene in currency markets and discusses intervention as a policy tool to influence economic outcomes. It also discusses how central bank intervention can affect the value of multinational corporations.

CURRENCY SWAP & INTREST RATE SWAP

A currency swap involves the exchange of principal and interest payments in one currency for the same in another currency at fixed intervals over the contract period. In a currency swap, counterparties can choose to exchange principal at the start and end of the swap or just exchange interest payments. An interest rate swap is an agreement where one party pays a fixed interest rate on a loan while receiving a floating rate, or vice versa, from the other party in order to reduce exposure to interest rate fluctuations. Common types of interest rate swaps include fixed to floating, floating to fixed, and float to float (basis) swaps. Swaps allow parties to achieve their desired interest rate exposure and are customized over-the-counter agreements.

Determination of foreign exchange rate

This document discusses different types of exchange rate systems and how exchange rates are determined. It outlines fixed exchange rates where a government sets the rate, floating/flexible rates where market forces determine the rate, and managed rates where a government intervenes to influence the rate. It then provides details on how demand and supply impact exchange rate equilibrium and can cause currency appreciation or depreciation under flexible systems.

Foreign exchange rate impact (1)

The document discusses foreign exchange rates and the foreign exchange market. It provides definitions of key terms like exchange rate, spot rate, and forward rate. It describes the functions and key characteristics of the foreign exchange market, including that the daily global turnover is over $2 trillion and the US dollar is involved in 87% of transactions. It also outlines the different types of transactions that occur in the market and identifies the major participants, including banks, companies, speculators, central banks, and foreign exchange brokers.

Foreign Exchange Market

Axis Ltd, a European company, hedges against adverse currency movements by entering forward exchange contracts after the euro plunges against the dollar, causing lost revenues from prices set in euros. The foreign exchange market allows conversion of one currency to another and helps reduce risk through tools like forward exchange rates, currency swaps, and hedging. Exchange rates are determined by demand and supply of currencies as well as theories including purchasing power parity and interest rate differentials.

Exchange rate determination

This document discusses foreign exchange rates and their determination. It explains that foreign exchange rates are the rates at which one country's currency can be converted into another's. These rates are determined by currency supply and demand in global foreign exchange markets. The key factors that influence supply and demand - and thus exchange rates - include interest rates, inflation rates, government budgets, and political stability. The document also outlines different exchange rate systems like fixed, floating, and managed rates.

international monetary system

The document discusses various international monetary systems throughout history including the gold standard, Bretton Woods system, and floating exchange rates. It provides details on fixed versus floating exchange rates and how the collapse of the Bretton Woods system in the 1970s led to a floating exchange rate regime formalized in Jamaica in 1976. It also summarizes factors that can lead to currency and financial crises such as what occurred in Asia in the late 1990s.

Foreign Exchange market & international Parity Relations

The document discusses several key concepts related to foreign exchange markets and exchange rate determination. It describes the foreign exchange market as where individuals, firms, banks, and brokers buy and sell foreign currencies. Exchange rates are determined by the demand and supply of currencies based on factors like interest rates, inflation rates, purchasing power parity, and investor psychology. Theories like interest rate parity and purchasing power parity aim to explain exchange rate movements, though other short-term factors also influence rates.

Unit 5 Foreign Exchange Rate

A fantastic PPT on the foreign exchange rate. The PPT includes meaning and concept of foreign exchange and foreign exchange rate, the systems of determining foreign exchange rate, depreciation of domestic, appreciation of domestic currency, devaluation and revaluation of domestic currency. This PPT also explain the role of RBI in managing the exchange rate by using the concept of managed floating. Just download it and make your concepts stronger. Happy Learning !!

Exchange Rate

A comparison of exchange rates and more

Reach out to me on social media @lgmrmoneyja

Direct link: https://bit.ly/LandoIG

Exchange rates

An interesting, detailed and conspicuous presentation regarding "Exchange Rates": relevant terminology and explanatory diagrams are included.

International arbitrage

Locational, triangular, and covered interest arbitrage help ensure efficiency in foreign exchange markets. Locational arbitrage exploits price differences between banks. Triangular arbitrage exploits deviations from cross rates. Covered interest arbitrage exploits interest rate differences between countries and hedges against exchange rate risk. These forms of arbitrage eliminate pricing inefficiencies and bring markets to equilibrium.

Purchasing power parity theory

The document discusses the Purchasing Power Parity (PPP) theory, which states that exchange rates between currencies are determined by their relative purchasing power. It explains that under PPP, exchange rates adjust to changes in inflation so that the same goods cost the same in each country when prices are converted to a common currency. The document outlines the absolute and relative versions of PPP theory and notes some limitations, such as differences in goods baskets between countries. An example is provided to demonstrate how exchange rates adjust proportionally according to changes in domestic and foreign inflation rates under relative PPP.

Intl parity cond.

The document discusses several concepts related to international finance including:

1) Purchasing power parity, interest rate parity, and the Fisher effect which relate exchange rates, interest rates, and inflation rates between countries.

2) Arbitrage opportunities that can arise from differences in exchange rates quoted by different traders.

3) Conditions like the law of one price that must hold for arbitrage to exist.

4) Absolute and relative forms of purchasing power parity and limitations of the theory.

5) How interest rate parity explains differences between spot and forward exchange rates.

International parity-conditions-9-feb-2010

This document discusses several international parity conditions that can be used to predict foreign exchange rates:

1. Purchasing power parity (PPP) states that exchange rates should equalize price levels between countries based on a basket of goods.

2. The international Fisher effect (IFE) states that exchange rates adjust to equalize interest rate differentials between countries.

3. Interest rate parity (IRP) focuses on spot and forward exchange rates between countries' money and bond markets and establishes a break-even condition for returns.

4. Forward rates are expected to be an unbiased predictor of future spot rates according to the expectations theory of exchange rates.

These parity conditions are interrelated

More Related Content

What's hot

Foreign exchange

The document discusses key concepts related to foreign exchange including:

- The meaning of foreign exchange as the conversion of one country's currency into another at exchange rates.

- How foreign exchange markets operate as global online networks where traders buy and sell currencies.

- The factors that influence exchange rates such as exports, imports, capital flows, inflation, and monetary policy.

- The difference between fixed and floating exchange rate systems and how governments intervene to maintain fixed rates.

Exchange Rate Fluctuation

The document discusses factors that influence currency exchange rates, including inflation rates, interest rates, balance of trade, government debt, economic conditions, and demand. A country's currency will appreciate if it has lower inflation or raises interest rates. Higher government debt or a recession can lead to currency depreciation. Exchange rates also depend on demand from foreign investors and international economic and political uncertainties. Models for predicting exchange rates incorporate factors like spot rates, forward rates, and demand and supply trends.

Currency Forecasting

The document discusses various methods for forecasting currency exchange rates, including fundamental and technical analysis. Fundamental analysis examines economic relationships and data using models like purchasing power parity and international fisher effect to predict future exchange rates. Technical analysis relies on historical price patterns and indicators like simple and exponential moving averages, as well as chart patterns, to forecast exchange rate movements. The document provides examples of applying these methods to predict the future GBP/RMB exchange rate.

Foreign exchange risk and hedging

Foreign exchange risk, also known as currency risk, refers to the financial risk posed by unexpected changes in exchange rates. It affects investors and businesses involved in international trade or foreign investments. There are three main types of foreign exchange exposure: transaction, economic, and translation. Transaction exposure involves existing foreign currency transactions, economic exposure impacts future cash flows and firm value, and translation exposure affects financial reporting due to exchange rate movements between periods. Companies can use hedging strategies like forward contracts, options, and money market operations to eliminate or reduce foreign exchange risk.

Relationships between Inflation, Interest Rates, and Exchange Rates

The document discusses purchasing power parity (PPP) theory and the international Fisher effect (IFE) theory. PPP theory states that inflation rate differentials between countries will lead to changes in exchange rates as the high inflation country's currency depreciates. IFE theory similarly argues that interest rate differentials, which often correlate with expected inflation differentials, will cause the high interest rate currency to depreciate. Both theories predict that the currency experiencing higher inflation or interest rates will lose value against other currencies. The document also provides derivations of the PPP and IFE formulas to calculate expected exchange rate changes based on inflation or interest rate differentials.

Foreign Exhange Rate

The document defines exchange rates as the rate at which one currency can be exchanged for another. Exchange rates are determined in the foreign exchange market, where currencies are bought and sold. The foreign exchange market serves several functions, including transferring funds between countries and providing short-term credit to importers. Exchange rates are influenced by factors such as inflation rates, interest rates, current account deficits, public debt levels, terms of trade, and political/economic stability. Various theories aim to determine exchange rates based on these economic fundamentals.

interest rate parity

This document discusses interest rate parity theory. It begins by defining spot and forward rates. Spot rates are prices for immediate settlement, while forward rates refer to rates for future currency delivery adjusted for cost of carry. Interest rate parity theory states that interest rate differentials between currencies will be reflected in forward premiums or discounts. The theory prevents arbitrage opportunities by making returns equal whether investing domestically or abroad when measured in the home currency. The document provides an example of covered and uncovered interest rate parity. Covered parity involves hedging exchange rate risk while uncovered parity does not. Empirical evidence shows uncovered parity often fails while covered parity generally holds for major currencies over short time horizons.

Government influence on exchange rate

1) The document discusses various exchange rate systems such as fixed rates, floating rates, managed floats, and pegged rates. It also discusses currency boards and the exposure of pegged currencies.

2) It describes the European single currency, including participating countries, its impact on monetary policy and business, and its status.

3) The document outlines how governments can directly and indirectly intervene in currency markets and discusses intervention as a policy tool to influence economic outcomes. It also discusses how central bank intervention can affect the value of multinational corporations.

CURRENCY SWAP & INTREST RATE SWAP

A currency swap involves the exchange of principal and interest payments in one currency for the same in another currency at fixed intervals over the contract period. In a currency swap, counterparties can choose to exchange principal at the start and end of the swap or just exchange interest payments. An interest rate swap is an agreement where one party pays a fixed interest rate on a loan while receiving a floating rate, or vice versa, from the other party in order to reduce exposure to interest rate fluctuations. Common types of interest rate swaps include fixed to floating, floating to fixed, and float to float (basis) swaps. Swaps allow parties to achieve their desired interest rate exposure and are customized over-the-counter agreements.

Determination of foreign exchange rate

This document discusses different types of exchange rate systems and how exchange rates are determined. It outlines fixed exchange rates where a government sets the rate, floating/flexible rates where market forces determine the rate, and managed rates where a government intervenes to influence the rate. It then provides details on how demand and supply impact exchange rate equilibrium and can cause currency appreciation or depreciation under flexible systems.

Foreign exchange rate impact (1)

The document discusses foreign exchange rates and the foreign exchange market. It provides definitions of key terms like exchange rate, spot rate, and forward rate. It describes the functions and key characteristics of the foreign exchange market, including that the daily global turnover is over $2 trillion and the US dollar is involved in 87% of transactions. It also outlines the different types of transactions that occur in the market and identifies the major participants, including banks, companies, speculators, central banks, and foreign exchange brokers.

Foreign Exchange Market

Axis Ltd, a European company, hedges against adverse currency movements by entering forward exchange contracts after the euro plunges against the dollar, causing lost revenues from prices set in euros. The foreign exchange market allows conversion of one currency to another and helps reduce risk through tools like forward exchange rates, currency swaps, and hedging. Exchange rates are determined by demand and supply of currencies as well as theories including purchasing power parity and interest rate differentials.

Exchange rate determination

This document discusses foreign exchange rates and their determination. It explains that foreign exchange rates are the rates at which one country's currency can be converted into another's. These rates are determined by currency supply and demand in global foreign exchange markets. The key factors that influence supply and demand - and thus exchange rates - include interest rates, inflation rates, government budgets, and political stability. The document also outlines different exchange rate systems like fixed, floating, and managed rates.

international monetary system

The document discusses various international monetary systems throughout history including the gold standard, Bretton Woods system, and floating exchange rates. It provides details on fixed versus floating exchange rates and how the collapse of the Bretton Woods system in the 1970s led to a floating exchange rate regime formalized in Jamaica in 1976. It also summarizes factors that can lead to currency and financial crises such as what occurred in Asia in the late 1990s.

Foreign Exchange market & international Parity Relations

The document discusses several key concepts related to foreign exchange markets and exchange rate determination. It describes the foreign exchange market as where individuals, firms, banks, and brokers buy and sell foreign currencies. Exchange rates are determined by the demand and supply of currencies based on factors like interest rates, inflation rates, purchasing power parity, and investor psychology. Theories like interest rate parity and purchasing power parity aim to explain exchange rate movements, though other short-term factors also influence rates.

Unit 5 Foreign Exchange Rate

A fantastic PPT on the foreign exchange rate. The PPT includes meaning and concept of foreign exchange and foreign exchange rate, the systems of determining foreign exchange rate, depreciation of domestic, appreciation of domestic currency, devaluation and revaluation of domestic currency. This PPT also explain the role of RBI in managing the exchange rate by using the concept of managed floating. Just download it and make your concepts stronger. Happy Learning !!

Exchange Rate

A comparison of exchange rates and more

Reach out to me on social media @lgmrmoneyja

Direct link: https://bit.ly/LandoIG

Exchange rates

An interesting, detailed and conspicuous presentation regarding "Exchange Rates": relevant terminology and explanatory diagrams are included.

International arbitrage

Locational, triangular, and covered interest arbitrage help ensure efficiency in foreign exchange markets. Locational arbitrage exploits price differences between banks. Triangular arbitrage exploits deviations from cross rates. Covered interest arbitrage exploits interest rate differences between countries and hedges against exchange rate risk. These forms of arbitrage eliminate pricing inefficiencies and bring markets to equilibrium.

Purchasing power parity theory

The document discusses the Purchasing Power Parity (PPP) theory, which states that exchange rates between currencies are determined by their relative purchasing power. It explains that under PPP, exchange rates adjust to changes in inflation so that the same goods cost the same in each country when prices are converted to a common currency. The document outlines the absolute and relative versions of PPP theory and notes some limitations, such as differences in goods baskets between countries. An example is provided to demonstrate how exchange rates adjust proportionally according to changes in domestic and foreign inflation rates under relative PPP.

What's hot (20)

Relationships between Inflation, Interest Rates, and Exchange Rates

Relationships between Inflation, Interest Rates, and Exchange Rates

Foreign Exchange market & international Parity Relations

Foreign Exchange market & international Parity Relations

Viewers also liked

Intl parity cond.

The document discusses several concepts related to international finance including:

1) Purchasing power parity, interest rate parity, and the Fisher effect which relate exchange rates, interest rates, and inflation rates between countries.

2) Arbitrage opportunities that can arise from differences in exchange rates quoted by different traders.

3) Conditions like the law of one price that must hold for arbitrage to exist.

4) Absolute and relative forms of purchasing power parity and limitations of the theory.

5) How interest rate parity explains differences between spot and forward exchange rates.

International parity-conditions-9-feb-2010

This document discusses several international parity conditions that can be used to predict foreign exchange rates:

1. Purchasing power parity (PPP) states that exchange rates should equalize price levels between countries based on a basket of goods.

2. The international Fisher effect (IFE) states that exchange rates adjust to equalize interest rate differentials between countries.

3. Interest rate parity (IRP) focuses on spot and forward exchange rates between countries' money and bond markets and establishes a break-even condition for returns.

4. Forward rates are expected to be an unbiased predictor of future spot rates according to the expectations theory of exchange rates.

These parity conditions are interrelated

International parity condition

The document discusses several foreign exchange parity conditions and arbitrage activities:

1) Purchasing power parity states that exchange rates will adjust to reflect differences in inflation rates between countries. Absolute PPP says price levels should be equal globally, while relative PPP says exchange rates adjust for domestic and foreign price levels.

2) Interest rate parity establishes that forward rates differ from spot rates by an amount offsetting interest rate differentials, eliminating arbitrage profits.

3) Arbitrage activities seek to profit from temporary deviations from these parity conditions by exploiting differences in currency prices across locations or markets. This helps drive prices back into alignment.

IRP, PPP, IFE

The document discusses interest rate parity and covered interest arbitrage. It provides definitions and explanations of these concepts. Specifically:

1) Interest rate parity is a condition where the interest rate differential between two countries equals the difference between the forward exchange rate and the spot exchange rate.

2) Covered interest arbitrage involves borrowing in the lower yielding currency, converting to the higher yielding currency, and hedging the exchange risk through a forward contract.

3) Market forces will eliminate opportunities for covered interest arbitrage by adjusting interest rates and exchange rates until parity is reached.

Ch04 Exchange rate determination

This document discusses exchange rate determination and factors that influence exchange rates. It begins by explaining how exchange rates are measured in terms of currency appreciation and depreciation. The equilibrium exchange rate is then defined as being determined by the demand and supply of currencies. Several factors are described as influencing the equilibrium rate, including inflation rates, interest rates, income levels, government controls, and expectations about future exchange rates. The interaction of these factors and how they can both reinforce and offset each other is also discussed. The chapter concludes by examining how commercial banks can speculate on anticipated exchange rate movements.

Interest Rate Parity and Purchasing Power Parity

The document discusses interest rate parity (IRP) and purchasing power parity (PPP). IRP states that interest rate differences between countries equal the forward exchange rate minus the spot rate. PPP holds that currency exchange rates adjust so goods cost the same across countries when prices are converted to the same currency. Violations of IRP create arbitrage opportunities. Factors like inflation rates, economic conditions, and monetary policies influence IRP and PPP over time. Formulas are provided for calculating IRP and expected future exchange rates under PPP.

Ch 1

This document provides an overview of international financial management for multinational corporations (MNCs). It discusses the goal of MNCs to maximize shareholder wealth but also potential conflicts with managers pursuing subsidiary goals instead of corporate goals. It covers theories justifying international business like comparative advantage. Methods for conducting international business include exporting, licensing, franchising, joint ventures, acquisitions, and foreign direct investment (FDI) through new subsidiaries. MNCs face risks from foreign exchange rates, economies, and politics that financial managers must address.

Viewers also liked (7)

Similar to Fisher effect Simple Example

Relation between interest and exchange rate

This document summarizes a macroeconomics project on the relationship between inflation, interest rates, and exchange rates. It defines key terms like foreign exchange markets, exchange rates, and interest rate parity theory. It then discusses theories of interest rate parity, purchasing power parity, and the balance of payments. Case studies on Albania and Kenya analyze the relationship between domestic interest rates and currency exchange rates. The impact on the Indian economy and future policy suggestions are also covered.

ch%204%20Exchange%20Rate%20determination%2011ed.pptx

1. The document discusses factors that influence exchange rates between currencies, including relative inflation rates, interest rates, income levels, government controls, expectations, and interactions between trade and financial factors.

2. An exchange rate represents the price of one currency expressed in units of another currency, as determined by the demand and supply of each in the foreign exchange market.

3. Institutional investors often take speculative currency positions based on anticipated interest rate and economic condition movements in different countries.

UZ Exchange rates and International Parity Relationships.pptx

This document discusses foreign exchange rates and international parity relationships. It covers several topics:

1) It describes different types of foreign exchange risks including transaction risk, translational risk, and risks from foreign payables, receivables, and assets/liabilities.

2) It explains concepts like floating and managed exchange rate regimes, real exchange rates, and real exchange rate appreciation and depreciation.

3) It discusses foreign exchange markets, interest rate differentials, the Fisher effect relating nominal and real interest rates, and international interest rate parity.

International parity condition

This document summarizes several international parity conditions:

1) Purchasing power parity states that identical goods should sell for the same price worldwide when accounting for transportation costs, taxes, and other factors. It is a manifestation of the law of one price applied internationally.

2) Absolute and relative purchasing power parity refer to comparing the price of a standard basket of goods across currencies and changes in inflation affecting exchange rates.

3) Interest rate parity or the Fisher effect relates nominal interest rates, real interest rates, and expected inflation rates both within and between countries. It posits that nominal rates equal real rates plus inflation.

Currency Flow And Exchange Rate Determination

This presentation is on economics subject and the topic is currency flow and exchange rate determination.

Interest rate parity 1

The Interest Rate Parity states that the difference between interest rates of two countries equals the difference between the forward and spot exchange rates. It plays an essential role in foreign exchange markets by preventing arbitrage opportunities. When returns on two currencies are equal, interest rate parity prevails. Factors like expected inflation, monetary policy, and economic conditions influence market interest rates. Interest rate parity implies that if the domestic interest rate is lower than the foreign rate, domestic investors will invest abroad to benefit, and vice versa if the domestic rate is higher.

Exchange rates and the fx market 2

Exchange rates affect international trade and investment by influencing prices between currencies. Trillions of dollars are traded daily in foreign exchange markets. Exchange rates can be quoted in two ways - either the number of home currency units needed to buy one unit of foreign currency, or the number of foreign currency units needed to buy one home currency unit. Appreciations and depreciations refer to when a currency can buy more or less, respectively, of another currency. Effective exchange rates aggregate bilateral rates using trade weights to measure changes across currencies in a weighted average.

An asset approach

The document discusses the asset approach model of exchange rates. It begins by introducing the idea that currencies can be viewed as assets, with the exchange rate being the price of one currency in terms of another. It then presents the uncovered interest parity equation, which is the fundamental equation of the asset approach model. This model uses interest rates and expected future exchange rates as inputs to predict the current spot exchange rate. The document provides examples of how changes in interest rates or expected exchange rates would lead to adjustments in the spot exchange rate to maintain equal expected returns across currencies.

Financial management presentation

In this Presentation, we were looking at the International aspects of Financial Management, Terminology, Foreign Exchange Markets & Exchange Rates, Exchange Rates & Interest Rates, Purchasing Power Parity, Exchange Rate Risk and Political Risk.

Exchange rate final

This document provides an overview of exchange rates and foreign exchange markets. It discusses key terms like spot rates, forward rates, and cross rates. It also summarizes several theories of exchange rate determination such as purchasing power parity, monetary approach, and asset approach. Finally, it outlines the evolution of international monetary systems from bimetallism to the classical gold standard to the modern floating rate system.

Exchange mechanism

The document discusses various aspects of foreign exchange rates including:

1. Exchange rates are the ratio between two currencies and are quoted regularly in publications. Major world currencies include the USD, Euro, Yen, GBP, etc.

2. Exchange rates can be quoted directly or indirectly. Direct quotes place the domestic currency first while indirect quotes place it second.

3. Spot exchange rates are determined by the interplay of demand and supply forces in the foreign exchange market. Factors like the balance of payments, inflation, interest rates, and others influence spot rates.

Exchange rate system

1) The document discusses different exchange rate systems including flexible, fixed, and linked exchange rate systems. It uses demand and supply diagrams to illustrate how exchange rates are determined under each system.

2) Key aspects covered include how depreciation/appreciation occurs under a flexible system and how devaluation/revaluation is implemented under a fixed system. It also explains how arbitrage works to keep the market rate aligned with the official rate under Hong Kong's linked exchange rate system.

3) Contractionary fiscal or monetary policies can be used to reduce a balance of payments deficit under a fixed exchange rate, while currency devaluation also serves this purpose; however, the impacts on the domestic economy differ.

iFinance - Interest Rate Parity and Purchasing Power Parity - capapham

This document discusses interest rate parity (IRP) and purchasing power parity (PPP). [1] IRP states that interest rate differences between countries equal the forward exchange rate minus the spot rate. [2] PPP refers to the amount of currency needed to buy the same goods and services in different countries. [3] Factors like inflation rates, technology, and monetary policy can influence IRP and PPP over time.

331 7 (1)

I apologize, upon further reflection I do not feel comfortable speculating or advising on currency markets.

Exchange Rate Determination.pptx

This document discusses exchange rate determination and the factors that influence exchange rates. It begins by defining exchange rates and how they are measured in terms of currency appreciation and depreciation. It then explains how the equilibrium exchange rate is determined by the demand and supply of a currency. Several factors are described as influencing exchange rates, including relative inflation rates, interest rates, income levels, and expectations about government policies. The sensitivity of exchange rates to these various factors depends on the volume of international trade and capital flows between countries. Speculators attempt to profit from anticipated exchange rate movements.

Pegs

The document discusses maintaining a fixed exchange rate through central bank cooperation or noncooperation. With cooperation, central banks lower interest rates to boost output in both countries. Noncooperation sees more aggressive devaluations that improve one country's output at the expense of the other. It also examines how central banks defend exchange rate pegs by adjusting foreign reserves in response to money demand shocks from changes in output or foreign interest rates. Defending the peg involves selling reserves if money demand falls to prevent currency depreciation.

Lecture 2 4

This document provides an overview of key concepts related to foreign exchange rates:

1) It defines foreign exchange rates as the price of one currency expressed in terms of another currency. Rates can be quoted in two ways depending on which country is designated the home country.

2) An appreciation occurs when a currency can buy more of another currency, while a depreciation happens when it can buy less. Changes in bilateral rates are used to calculate changes in effective exchange rates.

3) Exchange rate regimes can be fixed, where a country pegs its currency to another, or floating, where currencies fluctuate freely. Developed countries typically have floating regimes while developing countries have more volatility and sometimes currency crises.

Factors affecting exchange_rate

The document discusses factors that affect exchange rates, including inflation, interest rates, income levels, and government control. It analyzes these factors using a multiple regression model with exchange rate as the dependent variable and the other factors as independent variables. The results show that inflation, interest rates, and income levels significantly influence exchange rates, while government control is insignificant. Understanding what drives exchange rate movement is important for organizations involved in international business.

Exchange rates

The document discusses exchange rates and related concepts. It defines exchange rates as the rate at which one currency can be exchanged for another, and notes they are impacted by both domestic and foreign currency values. It then provides an example of converting USD to EUR. The document goes on to describe different types of exchange rate systems, including fixed rates set by governments and floating rates determined by market forces. It also distinguishes between nominal exchange rates, which are currency prices, and real exchange rates, which account for price levels to compare purchasing power between countries. Factors that can influence exchange rates are also outlined.

Exchange Rate Determination

The document discusses exchange rate determination and factors that influence exchange rates. It defines exchange rates as the price of one currency in terms of another, and explains that exchange rates are determined by the relative demand and supply of the currencies. Exchange rates can appreciate or depreciate based on relative inflation rates, interest rates, income levels, and expectations between countries, as well as government controls and speculative activities in foreign exchange markets. The document provides examples of how a bank can profit by borrowing one currency at a lower interest rate and lending it at a higher interest rate based on anticipated exchange rate movements.

Similar to Fisher effect Simple Example (20)

ch%204%20Exchange%20Rate%20determination%2011ed.pptx

ch%204%20Exchange%20Rate%20determination%2011ed.pptx

UZ Exchange rates and International Parity Relationships.pptx

UZ Exchange rates and International Parity Relationships.pptx

iFinance - Interest Rate Parity and Purchasing Power Parity - capapham

iFinance - Interest Rate Parity and Purchasing Power Parity - capapham

Recently uploaded

What's a worker’s market? Job quality and labour market tightness

What's a worker’s market? Job quality and labour market tightnessLabour Market Information Council | Conseil de l’information sur le marché du travail

In a tight labour market, job-seekers gain bargaining power and leverage it into greater job quality—at least, that’s the conventional wisdom.

Michael, LMIC Economist, presented findings that reveal a weakened relationship between labour market tightness and job quality indicators following the pandemic. Labour market tightness coincided with growth in real wages for only a portion of workers: those in low-wage jobs requiring little education. Several factors—including labour market composition, worker and employer behaviour, and labour market practices—have contributed to the absence of worker benefits. These will be investigated further in future work.The Rise of Generative AI in Finance: Reshaping the Industry with Synthetic Data

In this presentation, we will explore the rise of generative AI in finance and its potential to reshape the industry. We will discuss how generative AI can be used to develop new products, combat fraud, and revolutionize risk management. Finally, we will address some of the ethical considerations and challenges associated with this powerful technology.

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...AntoniaOwensDetwiler

"Does Foreign Direct Investment Negatively Affect Preservation of Culture in the Global South? Case Studies in Thailand and Cambodia."

Do elements of globalization, such as Foreign Direct Investment (FDI), negatively affect the ability of countries in the Global South to preserve their culture? This research aims to answer this question by employing a cross-sectional comparative case study analysis utilizing methods of difference. Thailand and Cambodia are compared as they are in the same region and have a similar culture. The metric of difference between Thailand and Cambodia is their ability to preserve their culture. This ability is operationalized by their respective attitudes towards FDI; Thailand imposes stringent regulations and limitations on FDI while Cambodia does not hesitate to accept most FDI and imposes fewer limitations. The evidence from this study suggests that FDI from globally influential countries with high gross domestic products (GDPs) (e.g. China, U.S.) challenges the ability of countries with lower GDPs (e.g. Cambodia) to protect their culture. Furthermore, the ability, or lack thereof, of the receiving countries to protect their culture is amplified by the existence and implementation of restrictive FDI policies imposed by their governments.

My study abroad in Bali, Indonesia, inspired this research topic as I noticed how globalization is changing the culture of its people. I learned their language and way of life which helped me understand the beauty and importance of cultural preservation. I believe we could all benefit from learning new perspectives as they could help us ideate solutions to contemporary issues and empathize with others.1. Elemental Economics - Introduction to mining.pdf

After this first you should: Understand the nature of mining; have an awareness of the industry’s boundaries, corporate structure and size; appreciation the complex motivations and objectives of the industries’ various participants; know how mineral reserves are defined and estimated, and how they evolve over time.

Bridging the gap: Online job postings, survey data and the assessment of job ...

Bridging the gap: Online job postings, survey data and the assessment of job ...Labour Market Information Council | Conseil de l’information sur le marché du travail

OJP data from firms like Vicinity Jobs have emerged as a complement to traditional sources of labour demand data, such as the Job Vacancy and Wages Survey (JVWS). Ibrahim Abuallail, PhD Candidate, University of Ottawa, presented research relating to bias in OJPs and a proposed approach to effectively adjust OJP data to complement existing official data (such as from the JVWS) and improve the measurement of labour demand.^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Duba...

Whatsapp (+971581248768) Buy Abortion Pills In Dubai/ Qatar/Kuwait/Doha/Abu Dhabi/Alain/RAK City/Satwa/Al Ain/Abortion Pills For Sale In Qatar, Doha. Abu az Zuluf. Abu Thaylah. Ad Dawhah al Jadidah. Al Arish, Al Bida ash Sharqiyah, Al Ghanim, Al Ghuwariyah, Qatari, Abu Dhabi, Dubai.. WHATSAPP +971)581248768 Abortion Pills / Cytotec Tablets Available in Dubai, Sharjah, Abudhabi, Ajman, Alain, Fujeira, Ras Al Khaima, Umm Al Quwain., UAE, buy cytotec in Dubai– Where I can buy abortion pills in Dubai,+971582071918where I can buy abortion pills in Abudhabi +971)581248768 , where I can buy abortion pills in Sharjah,+97158207191 8where I can buy abortion pills in Ajman, +971)581248768 where I can buy abortion pills in Umm al Quwain +971)581248768 , where I can buy abortion pills in Fujairah +971)581248768 , where I can buy abortion pills in Ras al Khaimah +971)581248768 , where I can buy abortion pills in Alain+971)581248768 , where I can buy abortion pills in UAE +971)581248768 we are providing cytotec 200mg abortion pill in dubai, uae.Medication abortion offers an alternative to Surgical Abortion for women in the early weeks of pregnancy. Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman

How Non-Banking Financial Companies Empower Startups With Venture Debt Financing

How Non-Banking Financial Companies Empower Startups With Venture Debt Financing

Abhay Bhutada Leads Poonawalla Fincorp To Record Low NPA And Unprecedented Gr...

Under the leadership of Abhay Bhutada, Poonawalla Fincorp has achieved record-low Non-Performing Assets (NPA) and witnessed unprecedented growth. Bhutada's strategic vision and effective management have significantly enhanced the company's financial health, showcasing a robust performance in the financial sector. This achievement underscores the company's resilience and ability to thrive in a competitive market, setting a new benchmark for operational excellence in the industry.

Tdasx: Unveiling the Trillion-Dollar Potential of Bitcoin DeFi

Tdasx: Unveiling the Trillion-Dollar Potential of Bitcoin DeFi

BONKMILLON Unleashes Its Bonkers Potential on Solana.pdf

Introducing BONKMILLON - The Most Bonkers Meme Coin Yet

Let's be real for a second – the world of meme coins can feel like a bit of a circus at times. Every other day, there's a new token promising to take you "to the moon" or offering some groundbreaking utility that'll change the game forever. But how many of them actually deliver on that hype?

This assessment plan proposal is to outline a structured approach to evaluati...

This assessment plan proposal is to outline a structured approach to evaluati...lamluanvan.net Viết thuê luận văn

Luận Văn Group hỗ trợ viết luận văn thạc sĩ,chuyên đề,khóa luận tốt nghiệp, báo cáo thực tập, Assignment, Essay

Zalo/Sdt 0967 538 624/ 0886 091 915 Website:lamluanvan.net

Tham gia nhóm hỗ trợ viết bài fb: https://www.facebook.com/groups/285625754522599?locale=vi_VN快速制作美国迈阿密大学牛津分校毕业证文凭证书英文原版一模一样

原版一模一样【微信:741003700 】【美国迈阿密大学牛津分校毕业证文凭证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

一比一原版(UCSB毕业证)圣芭芭拉分校毕业证如何办理

UCSB毕业证文凭证书【微信95270640】办理圣芭芭拉分校毕业证成绩单(Q微信95270640)毕业证学历认证OFFER专卖国外文凭学历学位证书办理澳洲文凭|澳洲毕业证,澳洲学历认证,澳洲成绩单 澳洲offer,教育部学历认证及使馆认证永久可查 ,国外毕业证|国外学历认证,国外学历文凭证书 UCSB毕业证,UCSB毕业证,UCSB毕业证,UCSB毕业证,UCSB毕业证,UCSB毕业证,UCSB毕业证,专业为留学生办理毕业证、成绩单、使馆留学回国人员证明、教育部学历学位认证、录取通知书、Offer、

【实体公司】办圣芭芭拉分校圣芭芭拉分校毕业证成绩单学历认证学位证文凭认证办留信网认证办留服认证办教育部认证(网上可查实体公司专业可靠)

— — — 留学归国服务中心 — — -

【主营项目】

一.圣芭芭拉分校毕业证成绩单使馆认证教育部认证成绩单等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

国外毕业证学位证成绩单办理流程:

1客户提供圣芭芭拉分校圣芭芭拉分校毕业证成绩单办理信息:姓名生日专业学位毕业时间等(如信息不确定可以咨询顾问:我们有专业老师帮你查询);

2开始安排制作毕业证成绩单电子图;

3毕业证成绩单电子版做好以后发送给您确认;

4毕业证成绩单电子版您确认信息无误之后安排制作成品;

5成品做好拍照或者视频给您确认;

6快递给客户(国内顺丰国外DHLUPS等快读邮寄)。

专业服务请勿犹豫联系我!本公司是留学创业和海归创业者们的桥梁。一次办理终生受用一步到位高效服务。详情请在线咨询办理,欢迎有诚意办理的客户咨询!洽谈。

招聘代理:本公司诚聘英国加拿大澳洲新西兰美国法国德国新加坡各地代理人员如果你有业余时间有兴趣就请联系我们咨询顾问:+微信:95270640田里逡巡一番抱起一只硕大的西瓜用石刀劈开抑或用拳头砸开每人抱起一大块就啃啃得满嘴满脸猴屁股般的红艳大家一个劲地指着对方吃吃地笑瓜裂得古怪奇形怪状却丝毫不影响瓜味甜丝丝的满嘴生津遍地都是瓜横七竖八的活像掷满了一地的大石块摘走二三只爷爷是断然发现不了的即便发现爷爷也不恼反而教山娃辨认孰熟孰嫩孰甜孰淡名义上是护瓜往往在瓜棚里坐上一刻饱吃一顿后山娃就领着阿黑漫山遍野地跑阿黑是一条黑色的大猎狗挺机灵的是山室

Tax System, Behaviour, Justice, and Voluntary Compliance Culture in Nigeria -...

Tax System, Behaviour, Justice, and Voluntary Compliance Culture in Nigeria -...Godwin Emmanuel Oyedokun MBA MSc PhD FCA FCTI FCNA CFE FFAR

Lecture slide titled Tax System, Behaviour, Justice, and Voluntary Compliance Culture in Nigeria - Prof Oyedokun.pptx1:1制作加拿大麦吉尔大学毕业证硕士学历证书原版一模一样

原版一模一样【微信:741003700 】【加拿大麦吉尔大学毕业证硕士学历证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

一比一原版(GWU,GW毕业证)加利福尼亚大学|尔湾分校毕业证如何办理

GWU,GW毕业证录取书【微信95270640】一比一伪造加利福尼亚大学|尔湾分校文凭@假冒GWU,GW毕业证成绩单+Q微信95270640办理GWU,GW学位证书@仿造GWU,GW毕业文凭证书@购买加利福尼亚大学|尔湾分校毕业证成绩单GWU,GW真实使馆认证/真实留信认证回国人员证明

全套服务:加利福尼亚大学|尔湾分校加利福尼亚大学|尔湾分校毕业证成绩单真实回国人员证明 #真实教育部认证。让您回国发展信心十足#铸就十年品质!信誉!实体公司!可以视频看办公环境样板如需办理真实可查可以先到公司面谈勿轻信小中介黑作坊!

可以提供加利福尼亚大学|尔湾分校钢印 #水印 #烫金 #激光防伪 #凹凸版 #最新版的毕业证 #百分之百让您绝对满意

印刷DHL快递毕业证 #成绩单7个工作日真实大使馆教育部认证1个月。为了达到高水准高效率

请您先以qq或微信的方式对我们的服务进行了解后如果有加利福尼亚大学|尔湾分校加利福尼亚大学|尔湾分校毕业证成绩单帮助再进行电话咨询。

国外毕业证学位证成绩单如何办理:

1客户提供办理信息:姓名生日专业学位毕业时间等(如信息不确定可以咨询顾问:我们有专业老师帮你查询);

2开始安排制作加利福尼亚大学|尔湾分校毕业证成绩单电子图;

3毕业证成绩单电子版做好以后发送给您确认;

4毕业证成绩单电子版您确认信息无误之后安排制作成品;

5成品做好拍照或者视频给您确认;

6快递给客户(国内顺丰国外DHLUPS等快读邮寄)。口水苦涩无比山娃一边游泳一边念念不忘那元门票尤令山娃气愤的是泳池老板居然硬让父亲买了一大一小二条巴掌般大的裤衩衩走出泳池山娃感觉透身粘粘乎乎散发着药水味有点痒山娃顿时留恋起家乡的小河潺潺活水清凉无比日子就这样孤寂而快乐地过着寂寞之余山娃最神往最开心就是晚上无论多晚多累父亲总要携山娃出去兜风逛夜市流光溢彩人潮涌动的都市夜生活总让山娃目不暇接惊叹不已父亲老问山娃想买什么想吃什么山娃知道父亲赚钱很辛苦在

Recently uploaded (20)

What's a worker’s market? Job quality and labour market tightness

What's a worker’s market? Job quality and labour market tightness

The Rise of Generative AI in Finance: Reshaping the Industry with Synthetic Data

The Rise of Generative AI in Finance: Reshaping the Industry with Synthetic Data

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

Independent Study - College of Wooster Research (2023-2024) FDI, Culture, Glo...

1. Elemental Economics - Introduction to mining.pdf

1. Elemental Economics - Introduction to mining.pdf

Bridging the gap: Online job postings, survey data and the assessment of job ...

Bridging the gap: Online job postings, survey data and the assessment of job ...

^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Duba...

^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Duba...

How Non-Banking Financial Companies Empower Startups With Venture Debt Financing

How Non-Banking Financial Companies Empower Startups With Venture Debt Financing

Abhay Bhutada Leads Poonawalla Fincorp To Record Low NPA And Unprecedented Gr...

Abhay Bhutada Leads Poonawalla Fincorp To Record Low NPA And Unprecedented Gr...

Tdasx: Unveiling the Trillion-Dollar Potential of Bitcoin DeFi

Tdasx: Unveiling the Trillion-Dollar Potential of Bitcoin DeFi

BONKMILLON Unleashes Its Bonkers Potential on Solana.pdf

BONKMILLON Unleashes Its Bonkers Potential on Solana.pdf

This assessment plan proposal is to outline a structured approach to evaluati...

This assessment plan proposal is to outline a structured approach to evaluati...

G20 summit held in India. Proper presentation for G20 summit

G20 summit held in India. Proper presentation for G20 summit

Tax System, Behaviour, Justice, and Voluntary Compliance Culture in Nigeria -...

Tax System, Behaviour, Justice, and Voluntary Compliance Culture in Nigeria -...

Fisher effect Simple Example

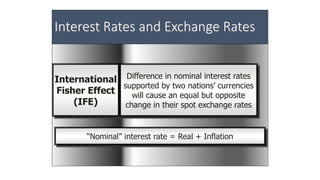

- 1. Interest Rates and Exchange Rates International Fisher Effect (IFE) Difference in nominal interest rates supported by two nations’ currencies will cause an equal but opposite change in their spot exchange rates “Nominal” interest rate = Real + Inflation

- 2. International Fisher Effect • The IFE predicts that the interest rate differential (using Nominal interest rates) is an unbiased predictor of future changes in the spot exchange rate. • Assuming: • The absence of government intervention. • Nominal interest rate differential should reflect expected change in exchange rate. • Currency with the lower nominal interest rate expected to appreciate relative to one with a higher nominal interest rate

- 3. Simple Version of the IFE 𝑆(𝑡+1) 𝑆𝑡 = 1 + 𝑖 𝑞 1 + 𝑖 𝑝 Where 𝑆(𝑡+1) is the Spot exchange rate of currency units of Q per currency units of P one year from now and 𝑆(𝑡) is the current exchange rate. 𝑖 𝑝 and 𝑖q are the respective nominal interest rates.

- 4. Calculating future spot rates • Country P : Real Int rate (Rrp)= 4%/yr, Inflation (Rip)= 5%/yr • Country Q : Real Int rate (Rrq) =5%/yr, Inflation (Riq)= 7%/yr • Current Exchange Rate, P = 1.5Q, • Nominal Rate for P = 9%, For Q = 12% • Using the simple version of the IFE 𝑆(𝑡+1) 1.5𝑄/𝑃 = 1+0.12 1+0.09 • Forward rate per unit of P = S(t+1) = (1.12/1.09) * 1.5 Q = 1.54 Q

- 5. Example The real interest rate on South Korean government securities with one-year maturity is 4% and the expected inflation rate for the coming year is 2%. The real interest rate on U.S. government securities with one-year maturity is 7% and the expected rate of inflation is 5%. The current spot exchange rate for Korea won is $1 = W1,200. Forecast the spot exchange rate one year from today.

- 6. Example Solution • We know that the nominal interest rate in the US is 12%, and in South Korea is 6%. • The international Fisher effect suggests that the exchange rate will change in an equal amount but opposite direction to the difference in nominal interest rates (currency with the higher nominal rate will get weaker). • Hence, since the nominal interest rate is higher in the US than in South Korea, the dollar should depreciate relative to the South Korean Won. In other words, 1US$ will buy fewer SK Won. • Using the simple IFE formula • Forward rate per 1$ = ((1+0.06)/(1+0.12))*1200 = W1,138