Downloaded 677 times

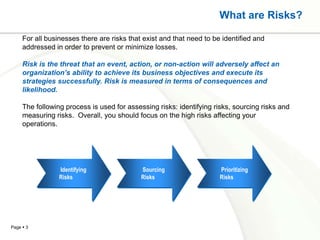

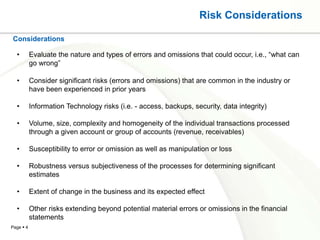

The document discusses financial controllership and internal controls. It defines financial controllership as a management function that supervises accounting, financial reporting, and implementation of internal controls. It then discusses risks, the process of identifying and prioritizing risks, and considerations for evaluating risks. Finally, it defines internal controls as processes designed to provide reasonable assurance of achieving objectives related to operations, financial reporting, and compliance.