Download as PPS, PPTX

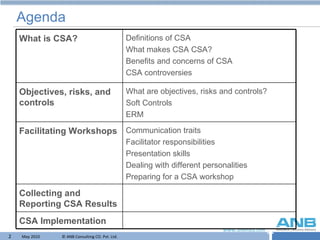

The document provides an overview of control self-assessment (CSA). It discusses what CSA is, its goals and benefits, how it is implemented through workshops, and how the results are reported. CSA involves employees assessing risks, controls and weaknesses within their process. Workshops are facilitated to have open discussions, develop recommendations and action plans. The results are anonymously reported to management to address issues.