Downloaded 1,642 times

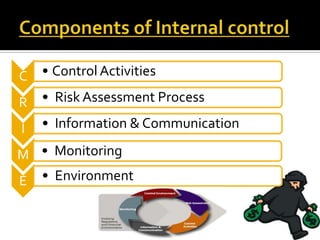

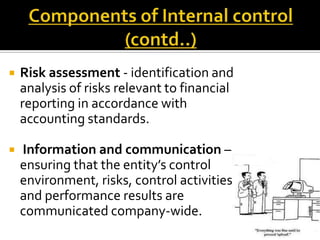

The document discusses internal controls in auditing, including the objectives, components, and case studies related to internal controls. It describes the control environment, risk assessment, control activities, information and communication, and monitoring as the main components of internal controls. The document also differentiates between substantive tests and tests of controls in auditing.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)